The Leviticus 25 Plan will generate annual budget surpluses of $37.303 billion during each of the first five years of activation (2027-2031), versus the CBO-projected $1.982 trillion average annual deficits, representing a positive budget gain of $2.019 trillion annually for the period.

Budget surpluses would be negotiable for partial transfer back to the Federal Reserve to effect ongoing reductions of the Citizens Credit Facility balance sheet. More importantly, $37.303 billion annual budget surpluses would provide a dynamic counterbalance to the inevitable demands on the Fed to purchase T-Bills and T-Bonds in support of Treasury Auctions throughout 2027-2031.

Overview, Primary Assumptions, Economic Scoring

The Leviticus 25 Plan activation period is slated for the 5-year period beginning in 2027 and ending in 2031.

- The Leviticus 25 Plan – Each participating U.S. citizen will receive a $60,000 deposit into a Family Account (FA) and a $35,000 deposit into a Medical Savings Account (MSA).

All U.S. citizens residing in the United States are eligible to participate, contingent upon meeting qualification standards and agreement to specified recapture provisions.

Participants (other than ‘custody account’ applicants) must prove stable credit history, stable job history, no recent drug/felony convictions.

These general recapture provisions include:

- Waiving all federal income tax refunds for a period of 5 years.

- Waiving benefits from economic security programs, select benefits from means-tested welfare programs, SSI, and SSDI for a period of 5 years.

- Enrollees in the Medicare, VA Healthcare system, Federal Employees Health Benefits

(FEHB), and TRICARE will be subject to a $7,000 deductible for primary care and outpatient

services annually for a period of 5 years. (See full plan for more details)

Primary scoring assumptions:

The Plan assumes an 80% participation rate by U.S. citizens. Wealthier Americans would choose not to participate, due to the comparative benefit of income tax refund amounts. Many individuals of lower socio-economic sector would also choose not to participate, due to the comparatively high benefits profiles that they would not wish to give up.

The Plan assumes that participating families would use significant funds to pay down / eliminate debt, and that these longer-term, lower debt service obligations would enhance the financial security of participating families for several decades beyond the opening activation period. Federal, state, and local government entities would benefit from longer-term tax revenue growth and reduced citizen dependence on government-based entitlement program benefits.

The Plan assumes that dynamic new efficiencies would emerge in the healthcare system – with more families managing/directing healthcare expenditures through their MSAs.

The Plan assumes that apart from the recapture provisions, there would also be significant tax revenue growth for federal, state and local government entities from free-market economic revitalization, more people working and paying taxes, and from the elimination of various income tax deductions (e.g. mortgage / HELOC interest expense).

The Plan assumes that there would not be a massive full-scale move back into the means-tested welfare programs, income security programs, SSI, and SSDI at the end of the initial 5-year activation period.

The benefits of a free-market economy and newfound economic liberty for American families would provide positive economic inertia throughout years 5-10, and for several decades beyond.

Recapture provisions would provide substantial federal budget surpluses for each year of the initial 5-year period. Economic growth over the following 10-15 years would generate sufficient recapture funding and tax revenue growth to offset the entire initial Federal Reserve balance sheet expansion.

Significant inertia from The Plan would also provide on-going, market-based growth benefits over succeeding years that far exceed any prospect for healthy economic growth that may be expected under America’s current big-government, central-planning approach.

Dynamic economic benefits would flow from:

- Family level massive debt elimination, financial security gains.

- Timely, sweeping reversal of big government “central planning” control.

- Productivity gains from reversal of work disincentives currently embedded in social programs.

- Economic growth, improved productivity, job creation, free market dynamics.

- Stabilization of bank capitalization, housing market.

- Strengthen / stabilize long-term value of U.S. Dollar.

- Minimizing the role of government in managing, directing, controlling the affairs of citizens.

- Federal Budget Deficit Projections – Congressional Budget Office

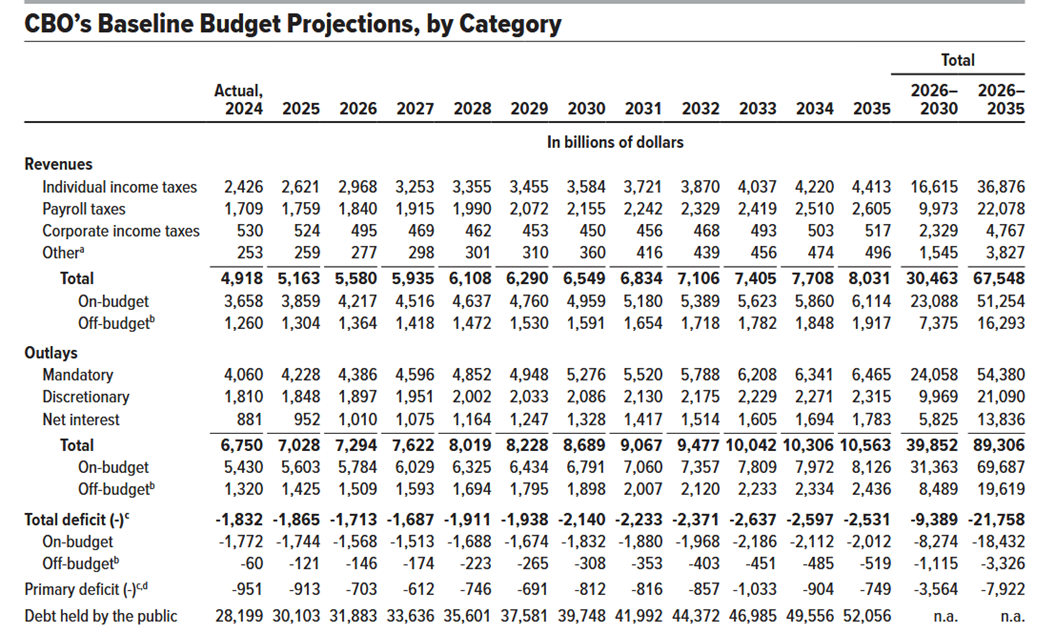

The Budget and Economic Outlook: 2025-2035 projects budget deficits ranging from $1.713 trillion 2026 to $2.140 trillion in 2030, and on up to $2.531 trillion by 2035. Actual deficits for the out years are likely to be higher than CBO projections, based upon history (“actual” versus “projected”).

Congressional Budget Office (CBO) Deficit Projections 2025-2035

CBO deficit projections for target period (2027-2031)

2024: $1.832 trillion (actual) vs $1.915 trillion (projected)

2025: $1.865 trillion

2026: $1.713 trillion

2027: $1.687 trillion

2028: $1.911 trillion

2029: $1.938 trillion

2030: $2.140 trillion

2031: $2.233 trillion

Total deficits projected 2027-2031: $9.909 trillion

Average annual budget deficits 2027-2031: $1.982 trillion

Source: CBO 10-Year Budget Projections (2025-2035): https://www.cbo.gov/system/files/2025-01/60870-Outlook-2025.pdf