Authored by Lance Roberts via RealInvestmentAdvice.com,

Jan 28, 2022 – Excerpts:

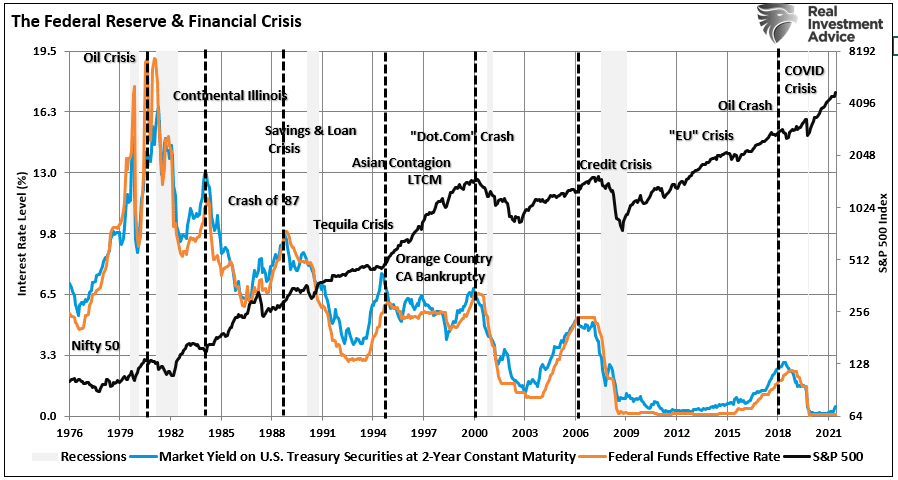

After more than 12-years of the most unprecedented monetary policy program in U.S. history, the Fed realizes there are significant risks in the financial system. The behavioral biases of individuals remain the most serious risk facing the Fed.

{kind=link}

With the Fed now reversing monetary accommodation, the question is how long before something breaks.

In the short term, the economy and the markets (due to the current momentum) can DEFY the laws of financial gravity as interest rates rise. However, as interest rates increase, they act as a “brake” on economic activity. Such is because higher rates NEGATIVELY impact a highly levered economy:

- Rates increases debt servicing requirements reducing future productive investment.

- Housing slows. People buy payments, not houses.

- Higher borrowing costs lead to lower profit margins.

- The massive derivatives and credit markets get negatively impacted.

- Variable rate interest payments on credit cards and home equity lines of credit increase, reducing consumption.

- Rising defaults on debt service will negatively impact banks which are still not as well capitalized as most believe.

- Many corporate share buyback plans and dividend payments are done through the use of cheap debt.

- Corporate capital expenditures are dependent on low borrowing costs.

- The deficit/GDP ratio will soar as borrowing costs rise sharply.

The debt problem exposes the Fed’s risk and why they continue to look for excuses NOT to hike rates. (Like “full employment” even though jobless claims are at record lows.) However, given economic stability was not achieved in the last decade, it is doubtful the withdrawal of monetary accommodation will be “risk-free.”

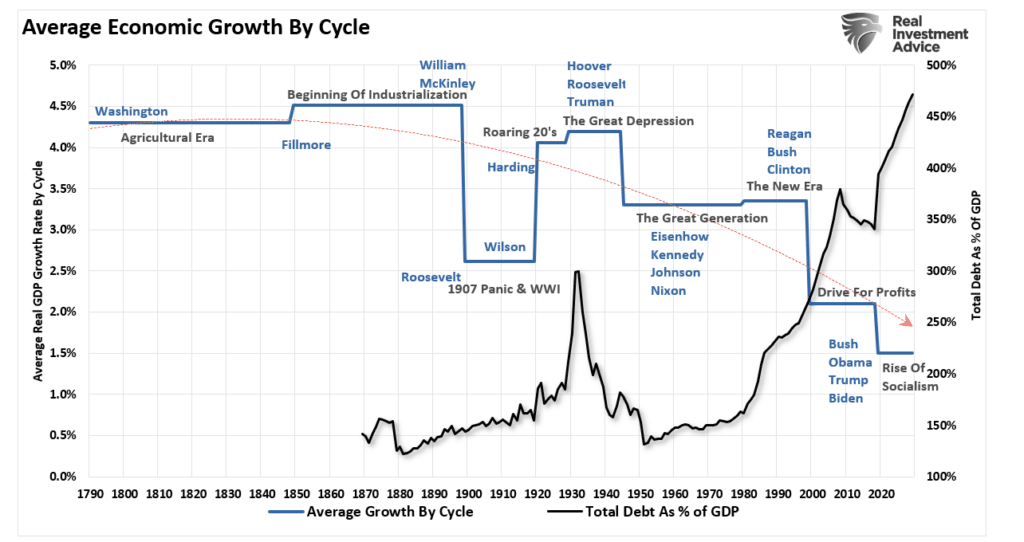

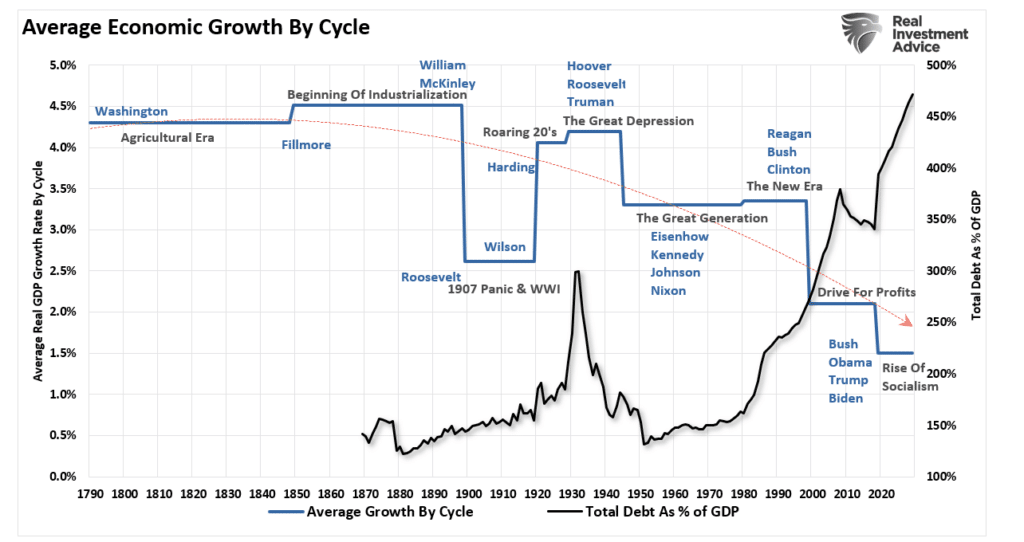

The evidence is quite clear that surging debt and deficits inhibit organic growth, and the massive debt levels are sensitive to increases in interest rates.

{kind=link}

With exceptionally high market valuations, Fed rate hikes historically led to events that devastated investors. Those events created the Fed’s repetitive cycle of monetary policy.

- Monetary policy drags forward future consumption leaving a void in the future.

- Since monetary policy does not create self-sustaining economic growth, ever-larger amounts of liquidity are needed to maintain the same level of activity.

- The filling of the “gap” between fundamentals and reality leads to economic contraction.

- Job losses rise, wealth effect diminishes, and real wealth reduces.

- The middle class shrinks further.

- Central banks act to provide more liquidity to offset recessionary drag and restart economic growth by dragging forward future consumption.

- Wash, Rinse, Repeat.

Conclusion

“Financial markets’ sensitivity to monetary policy has never been higher. The Fed’s balance sheet doubled since the end of the last financial crisis and is now 40% of gross domestic product. By buying massive amounts of bonds, the Fed lowered rates and used asset prices, like stocks, as the primary tool for monetary policy. That’s through the so-called wealth effect, or the tendency for consumers (two-thirds of GDP) to spend more as their assets grow.” – Joe LaVorgna

Therein lies the problem…. If the Fed tightens, the existing debt pile becomes more expensive to service, and stocks fall, hampering consumer confidence and economic growth.

On the other hand, if the Fed doesn’t tighten, debt across households, companies, and the government will continue to grow, making it more challenging for the Fed to act in the future

___________________________________

Exactly. The Fed cannot raise rates, in any meaningful way, with the U.S. economy surrounded by mountains of debt. According to the NY Fed, Household Debt climbed over the $15 trillion mark in Q3 2021. Corporate debt in 2020 rose to $11 trillion, according to Federal Reserve data.

The National Debt just hit $30 trillion. State and Local debt stands at $3.2 trillion.

The solution: America needs a dynamic new ‘debt elimination plan.’

There is just such a plan – loaded up and ready to launch. It will eliminate massive amounts of ‘ground level’ debt in America, usher in a long-term economic growth cycle, strengthen free market dynamics, and restore economic liberty.

It will generate $583 billion Federal budget surpluses during each of its first five years of activation – and pay for itself over a 10-15 year period.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2022 (3941 downloads)