Overview – “Consumer expenditures on interest payments represent a significant portion of household budgets, exceeding $1.1 trillion last quarter. These payments, covering non-mortgage debt like credit cards and auto loans, have risen significantly due to higher interest rates aimed at combating inflation, according to data from the U.S. Bureau of Economic Analysis (BEA).”

………………………………………….

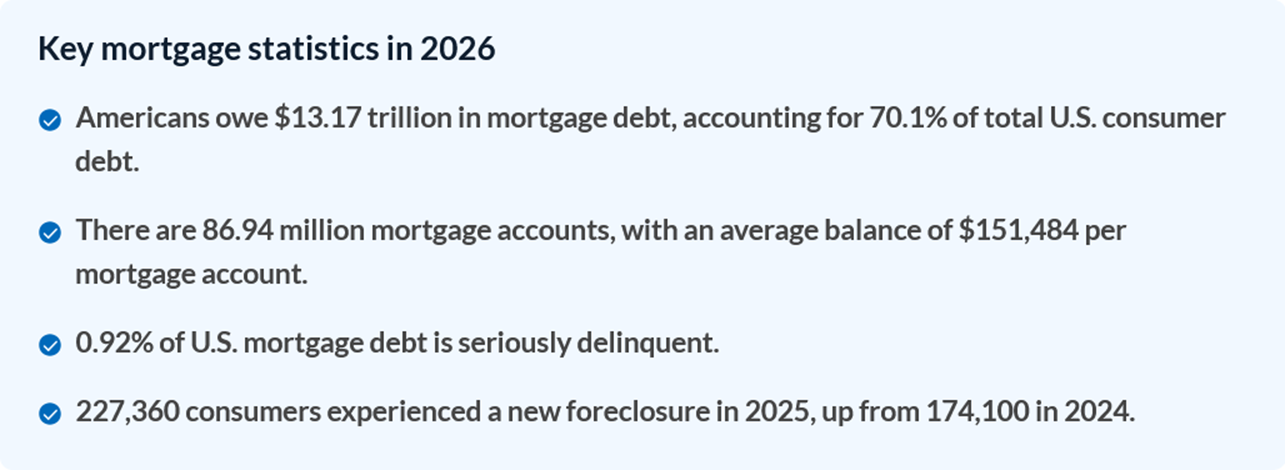

US Mortgage Statistics 2026: Debt, Delinquency and Foreclosure Data

Written by Maggie Davis | Edited by Dan Shepard | Updated Mar 25, 2026

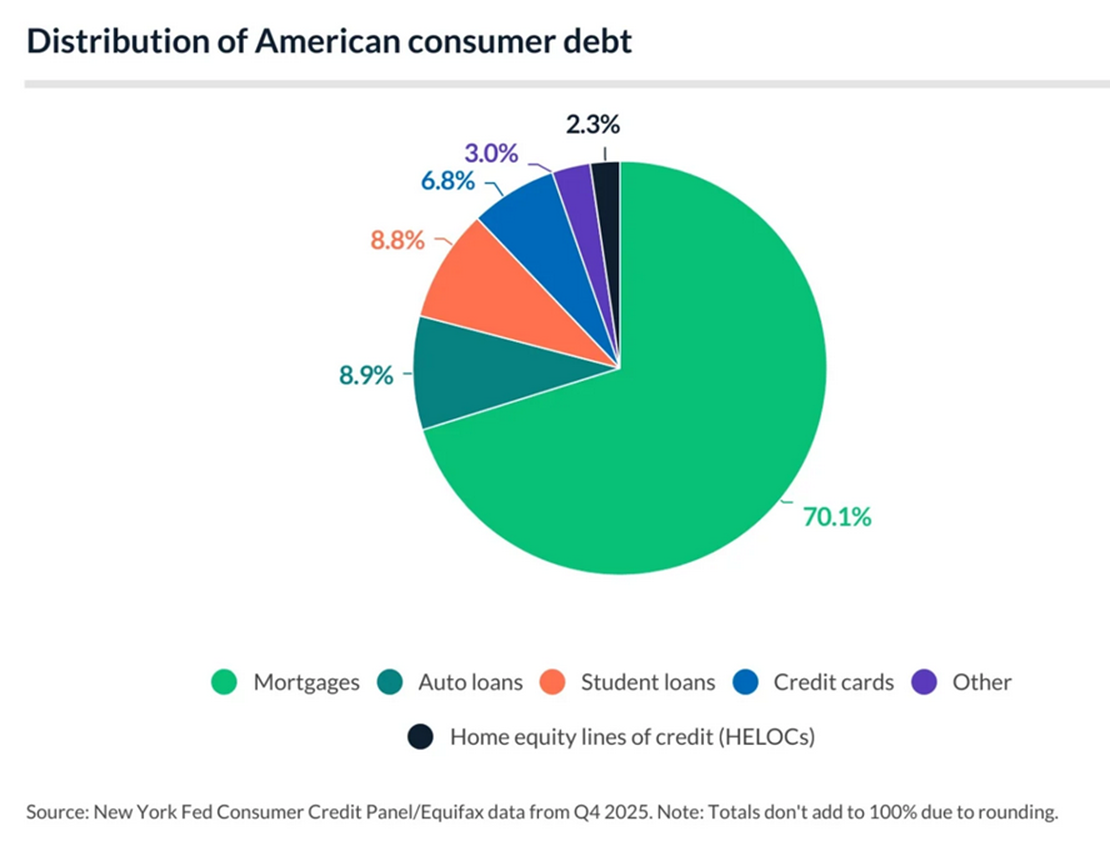

Americans collectively owe $13.17 trillion in mortgage debt, accounting for 70.1% of total U.S. consumer debt. Just 0.92% of mortgage debt is seriously delinquent, indicating that most borrowers are keeping up with their payments.

…………………………………………..

Household Debt and Credit Developments in 2025Q41

Federal Reserve Bank of New York – Quarterly Report on Household Debt and Credit 2025:Q4

Total Household Debt now stands at $18.8 trillion.

Non-mortgage household debt rose $191 billion in 2025Q4 to $5.164 trillion.

Mortgage Balances

• Mortgage balances grew by $98 billion during Q4 2025, totaling $13.17 trillion at the end of December;

• Home equity lines of credit “outstanding HELOC balances,” up $12 billion, to $433 billion.

Non-housing Consumer Debt

• Non-housing consumer debt balances increased by $81 billion to $5.164 trillion;

• Credit card balances rose $44 billion during the fourth quarter, now totaling $1.28 trillion;

• Auto loan balances edged up by $12 billion to $1.66 trillion;

• Other balances, which include retail cards and consumer finance loans, rose $14 billion to $564 billion;

• Student loan balances increased $11 billion in the quarter – current total $1.66 trillion.

Delinquency & Public Records

Aggregate delinquency rates worsened slightly in the fourth quarter of 2025. As of the end of December, 4.8% of outstanding debt was in some stage of delinquency… Transition into early delinquency ticked up slightly for mortgages and more significantly for student loans, but held mostly steady for autos, credit cards, and HELOCs.

___________________________________

The Leviticus 25 Plan will, at a minimum, eliminate several trillion dollars in consumer non-mortgage debt and satisfy delinquent debt obligations and clear bankruptcy notices for over 200,000 consumers.

The Leviticus 25 Plan will also draw down / eliminate trillions of dollars in Home Mortgages and Home Equity Lines of Credit (HELOC), and clear the majority of loan delinquencies and foreclosure filings.

Shifting trillions of dollars from monthly debt service obligations into savings/investments and non-debt based economic growth will: 1) Generate massive new tax revenue flows and payroll tax gains for federal and state government; 2) Reinvigorate/rescue millions of struggling small businesses across America; 3) Restore financial security for millions of hard-working, tax-paying U.S. citizen families; 4) Provide the banking system with trillions of dollars in fresh cash reserves – with the potential of providing critical support for the U.S. Treasury market.

These economic dynamics add to The Leviticus 25 Plan‘s compelling fiscal dynamics, which on their own set the United States federal government on course for $37.303 billion budget surpluses during each of the first five years of activation (2027-2031), while vastly improving balance sheets of virtually all state/local government entities.

The Leviticus 25 Plan – the most powerful economic reset plan in the world. Loaded up and ready to launch.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$95,000 per U.S. citizen – Leviticus 25 Plan 2027 (50979 downloads )