Affordable, high quality childcare is a serious problem across America today, reaching all the way down to the smallest of communities.

Big government programs, featuring direct funding supplements and tax breaks, to address this problem will increase the role of state and federal governmental agencies over the daily affairs of citizens – and further bloat the already roaring ‘federal and state budget deficits.’

These big government childcare programs, furthermore, will do nothing to fundamentally change the landscape – and offer American families an upgrade in their quality of life.

The Leviticus 25 Plan is a comprehensive economic acceleration plan with the power to eliminate federal and state budget deficits, eliminate massive sums of household debt, and provide direct economic and social benefits, including childcare needs for all participating U.S. citizens.

……………………………………..

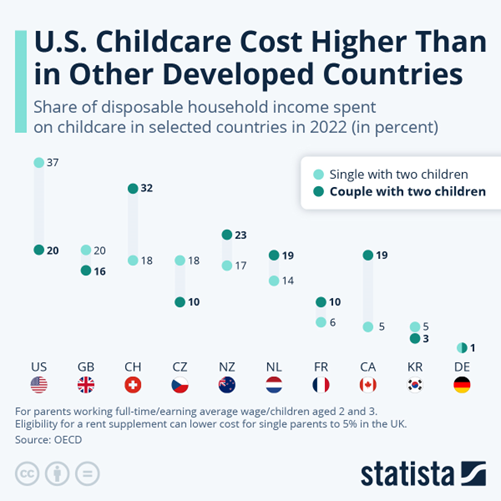

US Childcare Cost Higher Than In Other Developed Countries

ZeroHedge – Nov 10, 2024

U.S. childcare costs surpass those in all other OECD countries when taking into account single parents and couples earning average wage.

The price tag for having two children minded while working full-time is also significantly higher in the U.S. than in most other developed countries that are part of the organization.

Only Switzerland, the United Kingdom and New Zealand come even close to the high price parents have to shoulder for childcare in the United States.

You will find more infographics at Statista

As Statista’s Katharina Buchholz details below, according to 2022 data from the OECD, U.S. couples who both earn average wage in full-time jobs and have two young children need to spend 20 percent of their disposable household income on childcare.

For singles on average wage, this rises to 37 percent.

In most countries, single parents pay less as they receive a more favorable rate.

In Switzerland, the most expensive OECD country after the United States, couples with two children spent a whopping 32 percent of their disposable income on childcare if working full-time and earning average wage. For singles, this was lowered to 18 percent, however. In the U.S. and Switzerland alike, childcare is dominated by the private sector and does not receive substantial amounts of regulation or subsidies, leading to high market rates.

Treasury Secretary Janet Yellen has called this state of childcare in the U.S. a “broken market”.

Many Anglophone nations, also including Ireland, New Zealand and Australia struggle with high private market rates for childcare, low subsidies or a combination of the two.

In 2022, Canadian couples working full-time for average wage still needed to shell out 19 percent of disposable income, but the government has since made changes. Like in Canada, many English-speaking nations began to regulate and subsidize their childcare markets much later than elsewhere, leading to them lagging behind in affordability despite the topic of childcare becoming ever more important in the face of demographic change. Outside of Anglophone OECD countries, couples paid the most for childcare in relative terms in the Netherlands – another place dominated by private childcare – at 19 percent of disposable income. Singles paid the most in the Czech Republic at 18 percent.

In many European countries, parents paid substantially less, often just a couple of percent of their disposable incomes, as childcare centers are either run as a public service or private providers are heavily subsidized and regulated. In France, parents who work full-time and earn average wage spent between 6 percent and 10 pecent, while this number was even lower in South Korea, other German-speaking, Scandinavian and Baltic countries. In Germany, rates were as low as 1 percent of disposable income as all parents receive childcare vouchers depending on work time to be redeemed at private or public institutions.

Working parents pay a small fee on top if they receive more than the standard five care hours. Free childcare was provided in OECD countries Italy and Latvia as well as in associated nations Bulgaria and Malta. Single parents also paid no fees in Greece and were substantially unburdened in Canada, under rent subsidies in the United Kingdom and under social assistance benefits in Japan, if they qualified for those.

_________________________________

The Leviticus 25 Plan has the power to ‘de-stress’ the average American family by granting direct liquidity benefits to resolve the childcare crisis in the U.S. today.

Participating families will be able to reduce/eliminate mortgage payments, credit card bills, car payments, installment debt — and re-balance their family finances in profoundly positive ways.

Millions of mothers who dream of staying at home and being ‘full time moms’ for their children would see that option become an instant reality. The same would apply to dads, where that option happened to be a better fit for their families.

In situations where both parents might wish to remain in the workforce and continue on with childcare, they would have more than adequate funding to cover childcare costs.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2025 (22215 downloads )

{kind=link}

{kind=link}