The Leviticus 25 Plan has the power to fix these ‘imbalances’…

…………………………………………..

Rents spike as big-pocketed investors buy mobile home parks

MICHAEL CASEY and CAROLYN THOMPSON

July 25, 2022

LOCKPORT, N.Y. (AP) — Excerpts:

Nationwide… institutional investors, led by private equity firms and real estate investment trusts and sometimes funded by pension funds, swoop in to buy mobile home parks. Critics contend mortgage giants Fannie Mae and Freddie Mac are fueling the problem by backing a growing number of investor loans.

The purchases are putting residents in a bind, since most mobile homes — despite the name — cannot be moved easily or cheaply. Owners are forced to either accept unaffordable rent increases, spend thousands of dollars to move their home, or abandon it and lose tens of thousands of dollars they invested.

“You’re putting people in a snare and a trap, where they have no ability to defend themselves,” he added.

Driven by some of the strongest returns in real estate, investors have shaken up a once-sleepy sector that’s home to more than 22 million mostly low-income Americans in 43,000 communities. Many aggressively promote the parks as ensuring a steady return — by repeatedly raising rent.

There’s also a growing industry, featuring how-to books, webinars and even a mobile home university, that offers tips to attract small investors.

“You went from an environment where you had a local owner or manager who took care of things as they needed fixing, to where you had people who were looking at a cost-benefit analysis for how to get the penny squeezed lowest,” Bellus said. “You combine it with an idea that we can just keep raising the rent, and these people can’t leave.”

George McCarthy, president and CEO of the Lincoln Institute of Land Policy, a Cambridge, Massachusetts-based think tank, said parks containing about a fifth of mobile home lots nationwide have been purchased by institutional investors over the past eight years.

McCarthy singled out Fannie Mae and Freddie Mac for guaranteeing the loans as part of a what the lending giants bill as expanding affordable housing. Since 2014, the Lincoln Institute estimates Freddie Mac alone provided $9.6 billion in financing for the purchase of more than 950 communities across 44 states.

A spokesman for Freddie Mac countered that it had purchased loans for less than 3% of the mobile home communities nationwide, and about 60% of those were refinances.

___________________________________

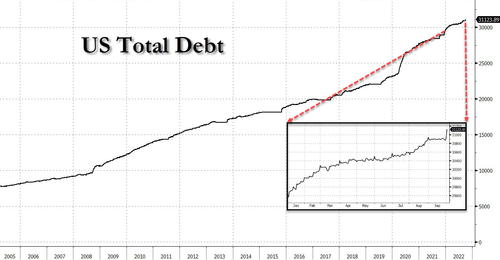

Note – Fannie Mae and Freddie Mac, were bailed out in the fall of 2008 to the tune of $187 billion from the U.S. Treasury Department, which was in turn receiving massive support via direct ‘Treasury debt’ purchases from the Federal Reserve (funded by freshly created electronic money).

And now we have Fannie Mae and Freddie Mac backing “big-pocketed investors,” scheming for profits by spiking the rents of mobile home park residents.

There is a way to ‘fix’ these types of imbalances.

Allow individual U.S. citizens the opportunity to upgrade their standard of living by moving out of mobile home parks and into their very own ‘rent-to-own’ homes – funded by direct liquidity extensions from a Federal Reserve Citizens Credit Facility.

Fannie Mae and Freddie Mac paid back their $187 bailout bonanza over the course of the following 10 years.

U.S. citizens, under the provisions of The Leviticus 25 Plan will also pay back their liquidity extensions – over the ensuing 10-15 years.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2023 (5005 downloads