“Economic control is not merely control of a sector of human life which can be separated from the rest; it is the control of the means for all our ends. And whoever has sole control of the means must also determine which ends are to be served, which values are to be rated higher and which lower — in short, what men should believe and strive for.” ― Friedrich Hayek

In January, Democrats plan to bring back the so-called Build Back Better Bill. If your Congressman, your Senator vote for it, that vote says everything you need to know about who she/he represents. And it is not you.

Here is what your Congressmen and Senators say the bill costs: $1,750,000,000,000.

However, the permanent cost—as estimated by the Congressional Budget Office—to fund this pork-filled so-called Build Back Better Bill is up to $4,730,000,000,000.

So much for the president’s claim that this bill is “free” or “costs nothing.” Do the politicians really think we are that stupid?

Try to even imagine what $1 trillion—$1,000,000,000,000—is. We all know what a day is, what a year is. Instead of dollars, let’s think in terms of trillions of days. How many years are one trillion days?

2.7 billion years. 2,700,000,000. That is a lot of lifetimes!

If your trillion-touting Congressman and Senator vote for this bill, here is how they want to spend your present and future tax dollars.

This billgives tax breaks to reporters, the media, unions, and trial attorneys. The bill-voting Congressman and Senators, obviously, believe it is more important to give tax breaks to reporters, the media, unions, trial attorneys than to plumbers, truck drivers, etc.—than to you, than to cut your tax dollars. This is a clear statement of who they really represent. And Mr. and Ms. Taxpayer Voter—it is not you.

If your Congressman, if your Senator vote for this bill, they have voted to give rich taxpayers in states like California, Illinois, and New York a big tax break. Again, not you.

If your Congressman, if your Senator vote for this bill, they are targeting small businesses. The bill increasing the occupational safety penalties (this is hard to believe) 10 times to $700,000 per violation. $700,000? It would break many businesses. If you, Mr. and Ms. Small Business Owner, do not follow the vaccine regulations you’re bankrupt.

Ronald Reagan stated, “The nine most terrifying words in the English language are: I’m from the government, and I’m here to help.”

This bill brings those terrifying words into reality. With this bill, your Congressman, your Senator voted to give the EPA $7 billion to employ a “climate corps.” Really? $7,000,000,000. That’s enough to fund an army of climate corps cops. If this bill passes, be prepared. That $7 billion climate corps army has to have something to do. The local climate cop will be on your doorstep surveying your carbon footprint.

Items as irresponsible as the above fill every page of this 2,466-page bill. All with lots of zeros. 2,466 pages… when is the last time you read 10 books?

Think of the price pain you are already feeling at the gas pump, in the grocery store. If this bill passes, that price pain will become more painful. Wait until you receive your heating bill this winter. This bill will accelerate the inflation price pain for a long time.

Your vote counts. Call, e-mail your Congressman. Call, e-mail your Senator. Ask why they voted for the bill. Will they vote for the bill? Ask them if they read this 2,466-page, 10-book bill. In all likelihood, few, if any, Congressmen or Senators read this bill, especially those who voted for the bill or will vote for it. To find your Congressman’s or Senator’s phone number and e-mail address, go to www.house.gov or www.senate.gov.

If your Congressman, your Senator vote for this bill, that vote says everything you need to know about whether they represent you. About whether they are qualified to remain in office. About whether you should ever vote for them again.

________________________________

Our Washington-based Democrat and Republican members of Congress should consider the one and only plan that favors individual citizens, rather than special interest groups… and that will actually reduce government deficits, rather than grow them precipitously… and that reduces dependence on government and restores economic liberty for all Americans

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

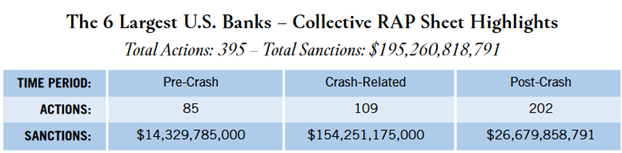

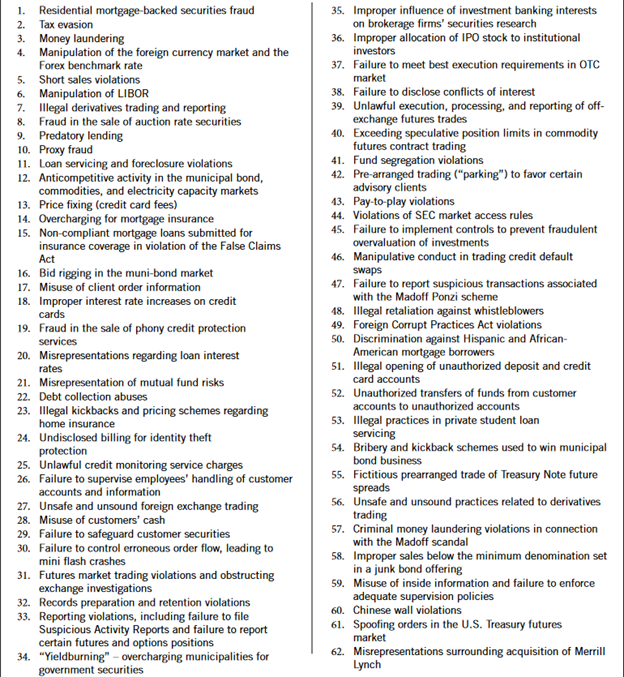

The six major Wall Street Banks highlighted below received highly preferential ‘targeted’ liquidity flows from the U.S. Treasury and the Federal Reserve over the past two decades, while at the same time engaging in a long list of criminal activities and lawless practices, including:

• money laundering; • bribery; • massive fraud in the sale of mortgage-backed securities; • credit card and checking account abuses; • foreclosure and debt collection violations; • breaches of fiduciary duty; • antitrust violations; • market manipulation; • enabling Ponzi schemes; and • even violations of election law.

The Special Report below further highlights these details. The $195 billion in sanctions that were levied against these six megabanks were a mere ‘slap on the wrist’ in comparison to the TARP funding, Federal Reserve ‘Secret Liquidity Lifelines’ funding, and access to the Fed’s discount window that they received. Source: bettermarkets.org

WALL STREET’S RAP SHEET Illegal Activity at the Nation’s Six Largest Megabanks Has Continued Since the 2008 Crash

The Leviticus 25 Plan is a powerful economic acceleration plan that ‘levels the playing field’ by granting U.S. citizens that same direct access to liquidity that was provided to major Wall Street banks before, during, and following the great financial crisis (2007-2010).

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America