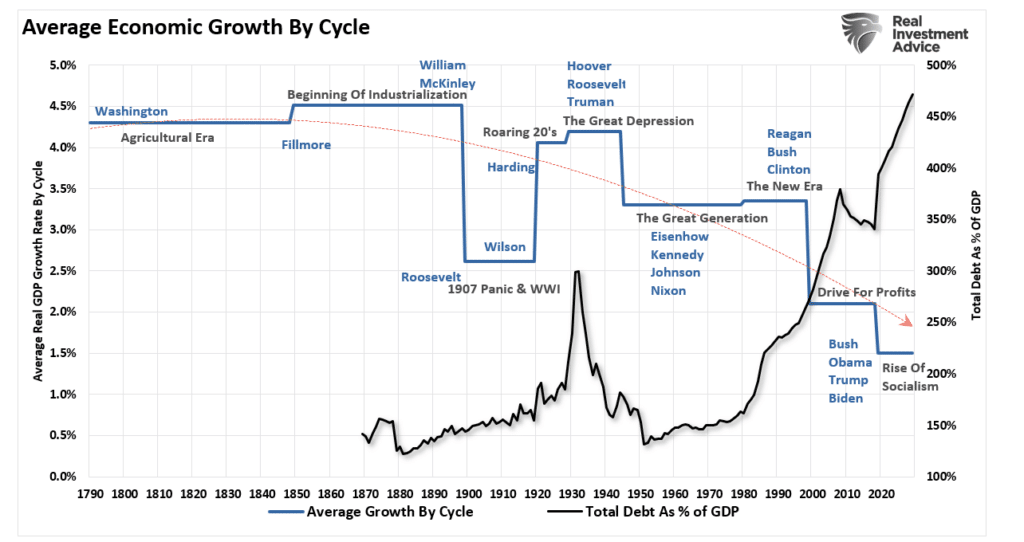

Our U.S. Congress has, as a practical matter, completely jettisoned fiscal discipline in their budgeting process.

The Government Accountability Office (GAO) stated in their March 23, 2021 report, The Nation’s Fiscal Health: “The unsustainable fiscal path strains the federal budget and contributes to growing debt. According to CBO, high and rising federal debt increases the likelihood of a fiscal crisis and could lead to a large drop in the value of the dollar or to a loss of confidence in the government’s ability or commitment to repay its debt in full.”

To accommodate the ongoing failure of our U.S. Congress to address this debt crisis, The Federal Reserve has had no choice but to ‘create’ new money, primarily to purchase large amounts of Treasury and Agency debt…..

………………………………………………………..

Felder Report: “Is It ‘Monetization’ Yet, Dr. Bernanke?”

Feb 19, 2022 | Authored by Jesse Felder via The Felder Report, | https://thefelderreport.com/2022/02/16/is-it-monetization-yet-dr-bernanke/

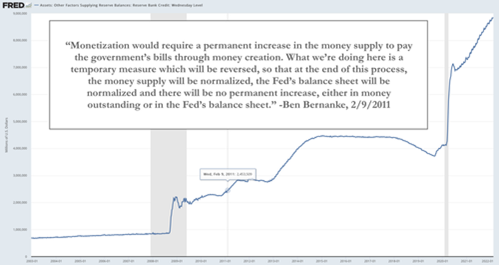

Eleven years ago, shortly after the onset of QE 2, Ben Bernanke gave us his definition for “monetization” of the debt, telling Congress (hat tip, Grant’s):

Monetization would require a permanent increase in the money supply to pay the government’s bills through money creation.

What we’re doing here is a temporary measure which will be reversed, so that at the end of this process, the money supply will be normalized, the Fed’s balance sheet will be normalized and there will be no permanent increase, either in money outstanding or in the Fed’s balance sheet.

At the time, The Fed’s balance sheet was approaching $2.5 trillion.

Today, it stands at nearly $9 trillion, more than triple the figure from a decade ago.

And so it only seems fair to ask, ‘Is it monetization yet, Dr. Ben?’

__________________________________________

The Leviticus 25 Plan is the one and only plan that is ‘primed up’ and ready to launch.

The Leviticus 25 Plan will provide a dynamic ‘recharge’ to the U.S. economy and restore economic liberty in America – and work get America’s budget deficits back under control and protect the long-term viability of the U.S. Dollar.

The Leviticus 25 Plan will generate $583 billion federal budget surpluses for the initial 5 years of activation (2023-2027), and completely pay for itself over the next 10-15 years.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America 2023

Economic Scoring links:

· The Leviticus 25 Plan 2023 – $583 Billion Federal Budget Surpluses Annually (2023-2027), Part 4: VA, TRICARE, FEHB, SSDI Recapture Benefits

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2023 (3972 downloads)

{kind=link}

{kind=link}