BNP Paribas is the largest bank in the Eurozone and 10th largest bank worldwide. This French financial behemoth is headquartered in Paris, with global headquarters in London. It owns subsidiaries all over the world, including BankWest in the U.S..

BNP was a major recipient of U.S taxpayer funds courtesy of the Federal Reserve and U.S. Treasury Department during the financial crisis years – to help restore them to ‘financial health.’ BNP has been involved in some distinctly ‘shady’ (and blatantly illegal) schemes in the past. They have recently ‘rolled the dice’ on an $80 million derivatives trade – and came up empty…

ZeroHedge (Feb 6, 2019): BNP lost $80 million in S&P500-linked derivative trades around Christmas; the massive trading loss emerged after Antoine Lours, BNP’s head of US index trading, put on positions on the S&P 500 which then quickly started losing money.

“BNP Paribas escaped the 2007–09 credit crisis relatively unscathed reporting a €3 billion net profit for the year of 2008, and €5.8 billion for 2009.” (Source: Wikipedia)

Thanks in no small part to U.S. taxpayers…

Background – Exhibit A:

Zero Hedge Feb 13, 2014: US Taxpayer “Bailed Out” BNP Paribas Probed By DoJ & Fed “TARP Recipient BNP Paribas got $4.9bn of bailouts from the U.S. Taxpayer – Today, as the WSJ reports we learn BNP Paribas has been funding transactions in Iran, Syria and other countries subject to U.S. Sanctions since 2002. The bank set aside $1.1 billion to settle investigations by the Department of Justice and the Federal Reserve but as the NY Times reports, investigations are playing out on multiple fronts – centering on whether the firm did “a significant amount” of business in “blacklisted” countires (and routed the deals through the US financial system).”

Via WSJ, – “…an internal probe conducted over the past few years “a significant volume of transactions” between 2002 and 2009 that could be “considered impermissible under U.S. laws and regulations...” “involving entities that were doing business in U.S.-sanctioned countries, such as Iran, Cuba, Sudan and Libya during the 2002 to 2009 period.

“BNP Paribas SA on Thursday became the latest bank to disclose the extent of its litigation problems in the U.S., saying it has set aside $1.1 billion against potential penalties related to transactions in countries under sanctions...

…………………………………

Background – Exhibit B:

BNP Paribas Sued by US Over Banker’s Alleged Role in Fraud

Oct. 19, 2011 (Bloomberg) — “BNP Paribas SA was sued by the U.S. over allegations the Paris-based bank aided a grain export fraud scheme involving commodity payment guarantees provided by the Department of Agriculture.

A corporate banker in BNP’s Houston office allegedly helped a scheme that defrauded the Agriculture Department of at least $78 million through deals he made with four U.S. grain exporters, according to a complaint filed yesterday in federal court in Houston.”

………………………….

Bloomberg Nov 28, 2011 – #18 recipient of Fed’s “secret liquidity lifelines”

“The credit crisis accelerated after BNP Paribas SA, France’s biggest bank, announced in August 2007 that it would halt withdrawals from three funds because mortgage-market turmoil “made it impossible” to value certain assets. BNP began taking Federal Reserve loans in December 2007 when the Term Auction Facility opened. By April 2008, its Fed debt reached $29.3 billion. In 2009, BNP became the euro region’s largest bank by deposits, purchasing Brussels-based Fortis’s units in Belgium and Luxembourg for 10.4 billion euros ($15.2 billion). It issued 5.1 billion euros of preference shares to the French government in March 2009, and reimbursed the state by October. In December 2010, when the Fed disclosed the loans, BNP said it used the TAF “to assist in recycling and facilitating liquidity.”

Peak Amount of Debt on 4/18/2008: $29.3B

_______________________________________

BNP Paribas received $4.9 billion in TARP funds from the U.S., and they went on to rake in a tidy $29.3 billion credit extension from the Fed via the Term Auction Facility… “to assist in recycling and facilitating liquidity.”

They were meanwhile funding significant transactions (Bloomberg) “involving entities that were doing business in U.S.-sanctioned countries, such as Iran, Cuba, Sudan and Libya during the 2002 to 2009 period.” And they ran a “grain export fraud scheme” which ‘cooked’ the U.S. Department of Agriculture for a cool $78 million.

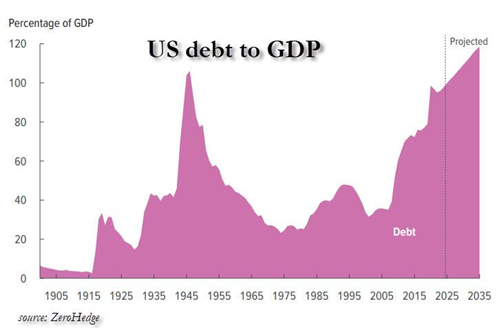

Begging the question: If BNP Paribas is deserving of direct liquidity infusions from the U.S. government and the Fed, then would it not be perfectly reasonable for U.S. citizens to also qualify for their own direct liquidity extensions “to assist in recycling and facilitating liquidity” at the family level.

………………………………………….

The Leviticus 25 Plan is the most powerful and dynamic economic acceleration plan in the world – delivering citizen-driven economic growth and citizen-centered healthcare.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2026 (24699 downloads )

{kind=link}