“The free man will ask neither what his country can do for him nor what he can do for his country. He will ask rather “What can I and my compatriots do through government” to help us discharge our individual responsibilities, to achieve our several goals and purposes, and above all, to protect our freedom? And he will accompany this question with another: How can we keep the government we create from becoming a Frankenstein that will destroy the very freedom we establish it to protect? Freedom is a rare and delicate plant.

Our minds tell us, and history confirms, that the great threat to freedom is the concentration of power. Government is necessary to preserve our freedom, it is an instrument through which we can exercise our freedom; yet by concentrating power in political hands, it is also a threat to freedom. Even though the men who wield this power initially be of-good will and even though they be not corrupted by the power they exercise, the power will both attract and form men of a different stamp.” – Milton Friedman, Capitalism and Freedom, 1962

__________________________________

The path to restoring freedom in America begins with reducing, by millions, the number of people who need to depend on government for their daily sustenance.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

America needs a qualitatively new economic strategy – one that will elevate large segments of our population up the scales of financial security, so they do not need so many of these social programs to survive…

…………………………………………………

The GAO Shows That Data Matching Can Reduce Waste, Fraud, and Abuse

In 2021, the GAO conducted a review of several programs that assist low-income individuals and concluded, among other things, that better data matching can prevent fraud, waste, and abuse, and can better direct funds to people that really need it.

In a report, the GAO looked at Earned Income Tax Credit (EITC), Housing Choice Vouchers, Low Income Home Energy Assistance Program (LIHEAP), Medicaid (Modified Adjusted Gross Income (MAGI) eligible), Supplemental Nutrition Assistance Program (SNAP), and Supplemental Security Income (SSI). All of these programs have income eligibility requirements.

The amount of improper payments made for a number of federal assistance programs is staggering. In 2019, improper payments for four programs was around $90b: Medicaid ($57.4b), the Earned Income Tax Credit (EITC) ($17.4b), Supplemental Security Income (SSI) ($5.5b), and SNAP ($4b).

For energy assistance programs, the GAO added that “[b]ased on [its] review of state plans, 13 agencies administering LIHEAP reported using no electronic data to verify beneficiaries’ income, verifying income in other ways, such as checking beneficiaries’ documents.” The report added that while the U.S. “Department of Health and Human Services (HHS) has encouraged LIHEAP agencies to use electronic data to improve program integrity, [it] has not taken recent steps to share information that could facilitate its use. HHS officials said that doing so could help state agencies’ verification efforts.

___________________________________________

The Leviticus 25 Plan will eliminate massive amounts of personal and household debt for working, tax-paying Americans – and grant millions of American families liquidity benefits that will allow them to directly allocate resources that best suit their needs – particularly in the realm of health care.

The Plan will help lift people up economically to a level where they will not need, and subsequently will not qualify for, many of these social programs.

Reducing the raw numbers of people enrolled in these programs will also serve to reduce the scope of fraud, waste, and abuse.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Navient is a Government-Sponsored Enterprise (GSE), formerly known as Sallie Mae, which effectively took over the student loan market in 2010. It is now losing a ‘boat-load’ of money, and taxpayers are ‘on the hook’ for billions.

………………………………………………………….

WSJ: Navient, the Student Loan Punching Bag

The Wall Street Journal Editorial Board, Jan 14, 2022 – Excerpts:

The Democrats’ government student loan takeover in 2010 is one of the great policy fiascoes of the age. But politicians can never admit it, so instead they’re kicking Navient, the student loan servicer.

Navient, formerly Sallie Mae, on Thursday agreed to settle 39 state Attorneys General lawsuits by cancelling $1.7 billion in defaulted debt. It will also make $260 payments to 350,000 federal student loan borrowers who were allegedly wrongly placed in long-term forbearance.

The State AGs accused Navient of “predatory lending” for making private loans to lower-income borrowers who attended for-profit schools, and for charging higher interest rates due to their higher credit risk. Heaven forbid a private lender, unlike the feds, try to avoid losing money.

Lower-income students couldn’t pay tuition with federal aid alone, so Navient filled the gap. For-profits also must derive at least 10% of their revenues from sources other than federal aid. So Navient indirectly helped those schools stay in business—and compete with community colleges. That’s another Navient political sin.

…..

The AGs accused Navient of wrongly placing borrowers in forbearance, which lets them defer payments while continuing to accrue interest. Borrowers enrolled in loan forgiveness plans also accrue interest because they often don’t pay enough to reduce their balance. This is a big reason the federal student loan balance sheet has doubled over the last decade to $1.6 trillion.

Navient denies wrongdoing and continues to fight similar legal charges filed by Obama Consumer Financial Protection Bureau Director Richard Cordray in early 2017. But it says settling the AG lawsuits was less expensive than continuing to fight. In September it also sought to end its government servicing contract because it was more hassle than it is worth.

But get this—Mr. Cordray, now chief operating officer of the Education Department’s Federal Student Aid office, requested that Navient renew the contract through 2023. Democrats need to keep around a punching bag as the government student loan debacle grows.

_______________________________

Note – “The average student loan debt for recent college graduates is nearly $30,000,” according to U.S News data, Sept. 14, 2021.

The Leviticus 25 Plan grants U.S. citizens the same direct access to liquidity that was provided to major banks and insurers during the great financial crisis. Each participating/qualifying citizen would receive a deposit of $60,000 into a Family Account (FA) and $30,000 into a Medical Savings Account (MSA).

The Plan would put students back in control of their college financing – and allow the government to dramatically shrink its student loan footprint.

It would facilitate a free market environment for higher education financing and provide It would provide direct liquidity extensions to reduce/eliminate loan balances.

It would provide liquidity for loan recipients of non-government financing – and help them also reduce/eliminate debt.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The headline 3.9% unemployment rate looks positive, but job creation fell significantly below consensus, at 199,000 in December versus a consensus estimate of 450,000.

The weak jobs figure should be viewed in the context of the largest stimulus plan in recent history. With massive monetary and fiscal support and a government deficit of $2.77 trillion, the second highest on record, job creation falls significantly short of previous recoveries and the employment situation is significantly worse than it was in 2019.

The most alarming datapoint is that real wages are plummeting. Average hourly earnings have risen 4.7% in 2021, but inflation is 6.8%, sending real wages to negative territory and the worst reading since 2011.

___________________________________________

“Government is not the answer,” as Pres. Ronald Reagan once said. “Government is the problem.”

Government, over the long haul, has an individualizing characteristic of complicating social issues and making problems worse.

It is high time to decentralize the system – and allow U.S. citizens to directly allocate resources, on their own behalf, in ways that best serve their personal needs and wishes, and free them from the tentacles of government control over their daily lives.

It is time to decentralize the system in a way that will eliminate massive amounts of ground-level debt in America, generate significant government budget surpluses and reduce long-term debt, and restore economic liberty for all Americans.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

“Economic control is not merely control of a sector of human life which can be separated from the rest; it is the control of the means for all our ends. And whoever has sole control of the means must also determine which ends are to be served, which values are to be rated higher and which lower — in short, what men should believe and strive for.” ― Friedrich Hayek

In January, Democrats plan to bring back the so-called Build Back Better Bill. If your Congressman, your Senator vote for it, that vote says everything you need to know about who she/he represents. And it is not you.

Here is what your Congressmen and Senators say the bill costs: $1,750,000,000,000.

However, the permanent cost—as estimated by the Congressional Budget Office—to fund this pork-filled so-called Build Back Better Bill is up to $4,730,000,000,000.

So much for the president’s claim that this bill is “free” or “costs nothing.” Do the politicians really think we are that stupid?

Try to even imagine what $1 trillion—$1,000,000,000,000—is. We all know what a day is, what a year is. Instead of dollars, let’s think in terms of trillions of days. How many years are one trillion days?

2.7 billion years. 2,700,000,000. That is a lot of lifetimes!

If your trillion-touting Congressman and Senator vote for this bill, here is how they want to spend your present and future tax dollars.

This billgives tax breaks to reporters, the media, unions, and trial attorneys. The bill-voting Congressman and Senators, obviously, believe it is more important to give tax breaks to reporters, the media, unions, trial attorneys than to plumbers, truck drivers, etc.—than to you, than to cut your tax dollars. This is a clear statement of who they really represent. And Mr. and Ms. Taxpayer Voter—it is not you.

If your Congressman, if your Senator vote for this bill, they have voted to give rich taxpayers in states like California, Illinois, and New York a big tax break. Again, not you.

If your Congressman, if your Senator vote for this bill, they are targeting small businesses. The bill increasing the occupational safety penalties (this is hard to believe) 10 times to $700,000 per violation. $700,000? It would break many businesses. If you, Mr. and Ms. Small Business Owner, do not follow the vaccine regulations you’re bankrupt.

Ronald Reagan stated, “The nine most terrifying words in the English language are: I’m from the government, and I’m here to help.”

This bill brings those terrifying words into reality. With this bill, your Congressman, your Senator voted to give the EPA $7 billion to employ a “climate corps.” Really? $7,000,000,000. That’s enough to fund an army of climate corps cops. If this bill passes, be prepared. That $7 billion climate corps army has to have something to do. The local climate cop will be on your doorstep surveying your carbon footprint.

Items as irresponsible as the above fill every page of this 2,466-page bill. All with lots of zeros. 2,466 pages… when is the last time you read 10 books?

Think of the price pain you are already feeling at the gas pump, in the grocery store. If this bill passes, that price pain will become more painful. Wait until you receive your heating bill this winter. This bill will accelerate the inflation price pain for a long time.

Your vote counts. Call, e-mail your Congressman. Call, e-mail your Senator. Ask why they voted for the bill. Will they vote for the bill? Ask them if they read this 2,466-page, 10-book bill. In all likelihood, few, if any, Congressmen or Senators read this bill, especially those who voted for the bill or will vote for it. To find your Congressman’s or Senator’s phone number and e-mail address, go to www.house.gov or www.senate.gov.

If your Congressman, your Senator vote for this bill, that vote says everything you need to know about whether they represent you. About whether they are qualified to remain in office. About whether you should ever vote for them again.

________________________________

Our Washington-based Democrat and Republican members of Congress should consider the one and only plan that favors individual citizens, rather than special interest groups… and that will actually reduce government deficits, rather than grow them precipitously… and that reduces dependence on government and restores economic liberty for all Americans

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Glenn Hubbard, dean of the Columbia Business School and former chairman of the Council of Economic Advisers during the George W. Bush presidency,. recently urged that financial crisis interventions should not be limited to banks.

“To be sure, recapitalizing financial institutions was an important element of the policy response. The depletion of capital buffers before the crisis reduced loan supply and exacerbated fire sales of distressed assets once the market collapsed. Cash infusions by the Treasury under the Troubled Asset Relief Program, in concert with the Fed’s bold lender-of-last-resort interventions, blunted the impact of the crisis.

That said, the perceived lack of attention to “Main Street” fed public suspicion of the bailouts. The government appeared to be more interested in addressing the decline in bank capital than the decline in home values. Millions of homeowners who were current in their mortgage payments were unable to refinance at lower interest rates because they were underwater. Yet many of these mortgages were already guaranteed by Fannie Mae and Freddie Mac , meaning taxpayers held the credit risk. Banks and investors holding the mortgages would never receive less than par.

The government should have directed a mass refinancing of mortgages for primary homes in which the borrower was current in payments. This would have led to an increase in disposable income and in home prices totaling more than $100 billion, according to a proposal Christopher Mayer and I offered at the time. The Treasury instead offered a tepid version of this with the Home Affordable Modification Program and the Home Affordable Refinance Program. These initiatives lacked the boldness of the bank bailouts, and Americans noticed…”

_____________________________

Hubbard concluded, “Ten years on, the U.S. still lacks a detailed plan for postcrisis intervention…”

What America really needs, to restore financial health to working families and ‘power up’ economic vitality throughout Main Street America – is a detailed plan for ‘pre-crisis’ intervention.

America needs a comprehensive economic plan that will insulate Main Street America from the next financial crisis and generate massive new tax revenue flows with a powerful, sustainable reduction in government deficits.

America’s new economic plan is currently loaded up and ready to go…

The Leviticus 25 Plan – An Economic Acceleration Plan for America

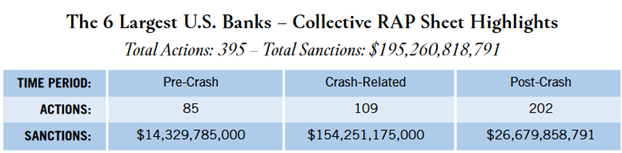

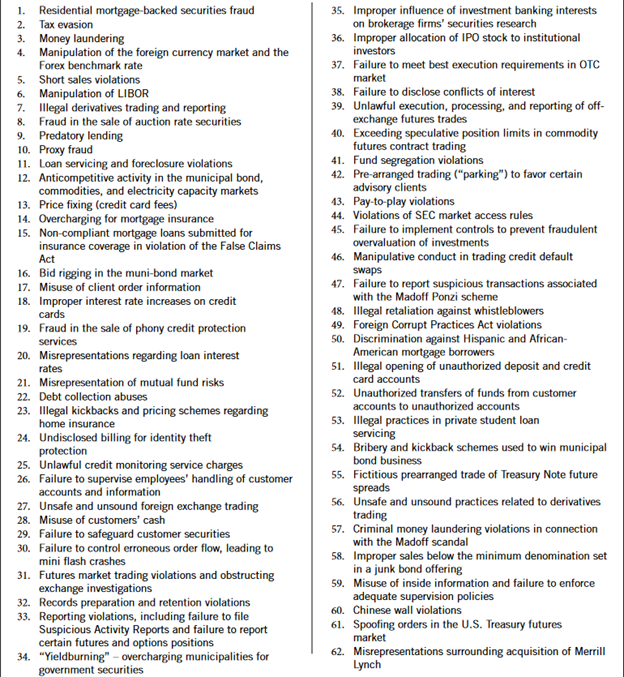

The six major Wall Street Banks highlighted below received highly preferential ‘targeted’ liquidity flows from the U.S. Treasury and the Federal Reserve over the past two decades, while at the same time engaging in a long list of criminal activities and lawless practices, including:

• money laundering; • bribery; • massive fraud in the sale of mortgage-backed securities; • credit card and checking account abuses; • foreclosure and debt collection violations; • breaches of fiduciary duty; • antitrust violations; • market manipulation; • enabling Ponzi schemes; and • even violations of election law.

The Special Report below further highlights these details. The $195 billion in sanctions that were levied against these six megabanks were a mere ‘slap on the wrist’ in comparison to the TARP funding, Federal Reserve ‘Secret Liquidity Lifelines’ funding, and access to the Fed’s discount window that they received. Source: bettermarkets.org

WALL STREET’S RAP SHEET Illegal Activity at the Nation’s Six Largest Megabanks Has Continued Since the 2008 Crash

The Leviticus 25 Plan is a powerful economic acceleration plan that ‘levels the playing field’ by granting U.S. citizens that same direct access to liquidity that was provided to major Wall Street banks before, during, and following the great financial crisis (2007-2010).

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Fan and Fred will buy mortgages up to $1 million, repeating the mistakes that led to the 2008 crash.

By Peter J. Wallison

Wall Street Journal, 11-25-21 – Excerpts:

The Federal Housing Finance Agency’s headquarters in Washington, March 20, 2019.

When the Supreme Court ruled last year that President Trump’s director of the Federal Housing Finance Agency could be removed without cause, many of us who follow housing policy knew what was coming. The next day, the Biden administration replaced the FHFA director, Mark Calabria, with a temporary appointment. Get ready for another housing boom—and bust.

FHFA is the regulator of the two government-backed housing lenders Fannie Mae and Freddie Mac. Mr. Calabria had been working to spin off Fannie and Freddie, hoping to reduce the harm they could do to the economy. But the Biden administration’s replacement immediately reversed course. “There is a widespread lack of affordable housing and access to credit, especially in communities of color,” said Acting Director Sandra Thompson. “It is FHFA’s duty through our regulated entities to ensure that all Americans have equal access to safe, decent, and affordable housing.”

This was no surprise. In an earlier pursuit of affordable housing, begun during the Clinton administration, Fannie and Freddie had brought down the U.S. housing market by reducing down payments and loosening underwriting standards.

By June 2008, the two government-backed housing lenders had acquired 16.5 million subprime or otherwise risky mortgages, with a principal amount of $2.5 trillion, and created an unprecedented housing bubble. When that bubble burst, it caused the 2008 financial crisis, the worst since the Great Depression.

With a Democratic president now in charge, it seems clear that the GSEs will once again be deployed—as they were before 2008—as instruments of the government’s efforts to increase affordable housing.

But this time there’s a more ominous twist. This newspaper has reported that the GSEs will also intervene in a market that doesn’t need any help—homes priced up to $1 million. The problem the administration sees is that housing and rental prices are too high. The fact that the administration’s own policies have caused an inflationary trend in housing along with food, energy and gasoline, among others, is no deterrent……

But the government’s lower underwriting standards drive down standards for private lenders, too. Banks and other mortgage lenders—if they want to stay in the business—have to offer their mortgages on similar terms. People who own homes then dive into the market to take advantage of the low down payments, and housing prices rise even faster. This encourages cash-out mortgages, in which homeowners reduce the equity in their homes, sometimes to buy a boat.

The process goes on for years until prices are so high that sales growth falls and homeowners can’t sell their homes to pay off their mortgages. Housing prices then collapse, mortgages go unpaid. Banks, other lenders, and even Fannie and Freddie incur losses and another financial crisis begins.

Americans would know all of this if Democrats in Congress, the media, and the Obama administration had not blamed the 2008 crisis on insufficient regulation. Instead of fixing housing finance, and privatizing or eliminating Fannie and Freddie, Democrats gave us the Dodd-Frank Act and a more intrusive government. Those who refused to acknowledge the true cause of the 2008 financial crisis are now on the way to repeating it.

Mr. Wallison is a senior fellow emeritus at the American Enterprise Institute and author of “Hidden In Plain Sight: What Really Caused the World’s Worst Financial Crisis and Why It Could Happen Again.”

__________________________________________

“Government is not the solution. Government is the problem.” – President Ronald Reagan, Inaugural Address, January 20, 1981

Rather than re-instituting failed policies, that continually ‘grow government,’ America needs policies that will reduce our government’s footprint, and scale back dependence on government largess, particularly when that generosity in bestowing money targets already wealthy Americans.

America doesn’t need another round of GSEs underwriting mountains of risky debt. It needs a plan that will improve the financial wherewithal of American families, and raise the quality of debt that flows within the structure of a free market economy.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

““However human, envy is certainly not one of the sources of discontent that a free society can eliminate. It is probably one of the essential conditions for the preservation of such a society that we do not countenance envy, not sanction its demands by camouflaging it as social justice, but treat it, in the words of John Stuart Mill, as ‘the most anti-social and evil of all passions.’” – Friedrich von Hayek, 1974 Nobel Prize, Economic Sciences