On Tuesday [Jun 25, 2019] after the close, the CFTC announced that Merrill Lynch Commodities (MLCI), a global commodities trading business, agreed to pay $25 million to resolve the government’s investigation into a multi-year scheme by MLCI precious metals traders to mislead the market for precious metals futures contracts traded on the COMEX (Commodity Exchange Inc.). The announcement was made by Assistant Attorney General Brian A. Benczkowski of the Justice Department’s Criminal Division and Assistant Director in Charge William F. Sweeney Jr. of the FBI’s New York Field Office…..

As MLCI itself admitted, beginning in 2008 and continuing

through 2014, precious metals traders employed by MLCI schemed to

deceive other market participants by injecting materially false and

misleading information into the precious metals futures market.

………………………………………………………………..

Federal Reserve emergency lending –

Merrill Lynch & Co.

“Merrill Lynch & Co.‘s

stock surged 30 percent after the New York-based securities firm announced an

agreement to sell itself to Bank of America Corp. in September 2008. The deal

didn’t stop the firm’s liquidity from shrinking by about $27 billion in three

days that month, according to internal Federal Reserve Bank of New York

documents. In the ensuing weeks, the firm drew as much as $62.1 billion from

the Federal Reserve’s Primary Dealer Credit Facility, Term Securities Lending

Facility and single-tranche open market operations. After the takeover

closed on Jan. 1, 2009, Charlotte, North Carolina-based Bank of America let

Merrill’s Fed loans roll off while increasing its own liquidity draws from the

central bank.”

Peak amount of debt on

09/26/2008: $62.1B

………………………………………..

Merrill Lynch engaged in a high-stakes leveraged speculation gambit which blew up when the subprime default wave hit and the mortgage backed securities (MBS) warehoused on their balance sheet plunged in value. They were subsequently rescued by the Fed, to the lively tune of $62.1 billion.

Additional background information on some of the investment practices engaged in by ML over

several years immediately preceding the $62.1B secret bailout:

Merrill Lynch “agreed to pay $10

million on Tuesday to settle fraud accusations by securities regulators.”

“The Securities and Exchange Commission had accused

Merrill of fraud, saying that the firm misused private information from its

customers to place trades on its own behalf and that the firm repeatedly

charged its customers trading fees without their knowledge.”

___________________________________

The Leviticus 25 Plan provides a mechanism for U.S. citizens to be granted the same direct liquidity access that was provided to Merrill Lynch and numerous other global financial heavyweights at the height of the financial crisis.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Major foreign banking interests, with U.S. subsidiaries, enjoyed massive liquidity infusions to help them survive their faltering financial prospects and debt burdens during the great financial crisis 2007-2010.

Bloomberg Nov 28, 2011:“Deutsche Bank AG, Germany’s biggest bank, navigated the financial crisis without capital injections from the German government. The Frankfurt-based bank, which in 2008 reported its first annual loss since World War II, wasn’t so shy about getting liquidity in secret from the U.S. Federal Reserve. The lender tapped the Fed for $66 billion on Nov. 6, 2008 — $28.2 billion from the Term Securities Lending Facility, $21.8 billion from single-tranche open market operations and $16 billion from the Term Auction Facility. John Gallagher, a Deutsche Bank spokesman, declined to say whether the bank took emergency loans during the crisis from other central banks, such as Germany’s Bundesbank.”

Could it be possible that we are on the verge of the next “Lehman Brothers moment”?

Deutsche Bank is the most important bank in all of Europe, it

has 49 trillion dollars in exposure to derivatives, and most of the

largest “too big to fail banks” in the United States have very deep

financial connections to the bank. In other words, the global

financial system simply cannot afford for Deutsche Bank to fail, and

right now it is literally melting down right in front of our eyes. For

years I have been warning that this day would come, and even though it

has been hit by scandal after scandal,

somehow Deutsche Bank was able to survive until now. But after what we

have witnessed in recent days, many now believe that the end is near

for Deutsche Bank. On July 7th, they really shook up investors all over

the globe when they laid off 18,000 employees and announced that they

would be completely exiting their global equities trading business…

It takes a lot to rattle Wall Street.

But Deutsche Bank managed to. The beleaguered German giant announced

on July 7 that it is laying off 18,000 employees—roughly one-fifth of

its global workforce—and pursuing a vast restructuring plan that most notably includes shutting down its global equities trading business.

Though Deutsche’s Bloody Sunday seemed to come out of the blue, it’s

actually the culmination of a years-long—some would say

decades-long—descent into unprofitability and scandal for the bank,

which in the early 1990s set out to make itself into a universal banking

powerhouse to rival the behemoths of Wall Street.

These moves may delay Deutsche Bank’s inexorable march into oblivion, but not by much.

And as Deutsche Bank collapses, it could take a whole lot of others down with it at the same time. According to Wall Street On Parade, the bank had 49 trillion dollars in exposure to derivatives as of the end of last year…

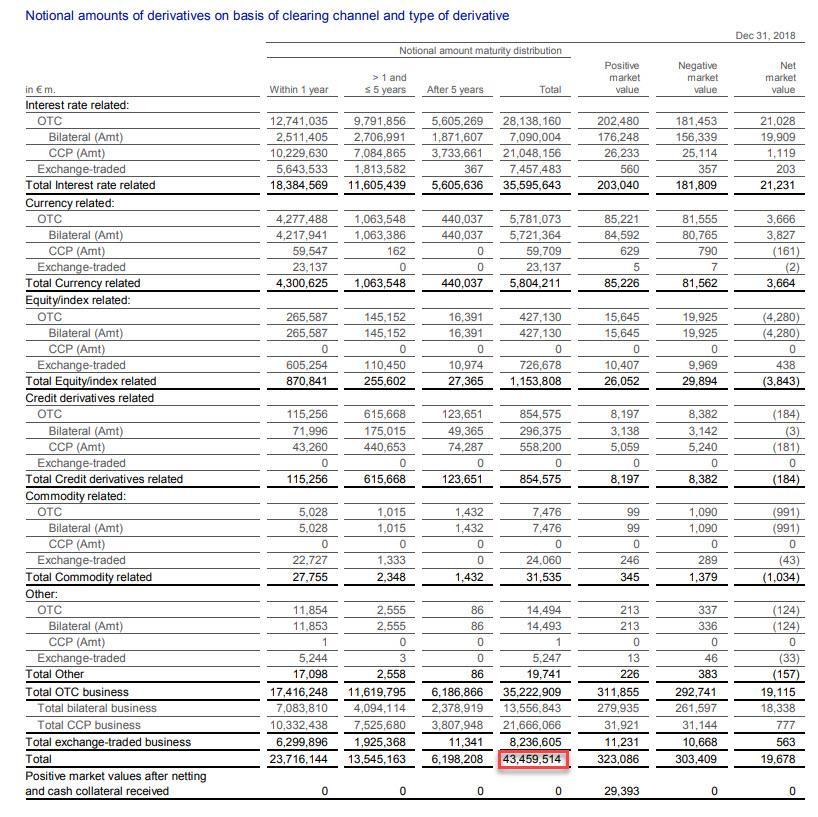

During 2018, the serially troubled Deutsche Bank – which still has a

vast derivatives footprint in the U.S. as counterparty to some of the

largest banks on Wall Street – trimmed

its exposure to derivatives from a notional €48.266 trillion to a

notional €43.459 trillion (49 trillion U.S. dollars) according to its

2018 annual report. A derivatives book of $49 trillion notional puts

Deutsche Bank in the same league as the bank holding companies of U.S.

juggernauts JPMorgan Chase, Citigroup and Goldman Sachs, which logged in

at $48 trillion, $47 trillion and $42 trillion, respectively, at the

end of December 2018 according to the Office of the Comptroller of the

Currency (OCC). (See Table 2 in the Appendix at this link.)

Yes, the actual credit risk to Deutsche Bank is much, much lower than

the notional value of its derivatives contracts, but we are still

talking about an obscene amount of exposure.

And this is especially true when we consider the state of Deutsche Bank’s balance sheet. According to Nasdaq.com,

as of the end of last year the bank had total assets of 1.541 trillion

dollars and total liabilities of 1.469 trillion dollars.

In other words, there wasn’t much equity there at the end of

December, and things have deteriorated rapidly since that time. In

fact, it is being reported that a billion dollars a day is being pulled out of the bank at this point.

I know that most Americans don’t really care if Deutsche Bank lives or dies, but as the New York Post has pointed out, the failure of Deutsche Bank could quickly become a major crisis for the entire global financial system…

But the important fact to remember is that Deutsche Bank traded these

derivatives with other financial firms. So, is this going to be another

Lehman Brothers situation whereby one bank’s problems becomes other

banks’ problems?

Pay close attention to this.

If the situation gets out of hand, the Federal Reserve and other

central banks will have no choice but to cut interest rates even if it’s

not the best thing for the world economies.

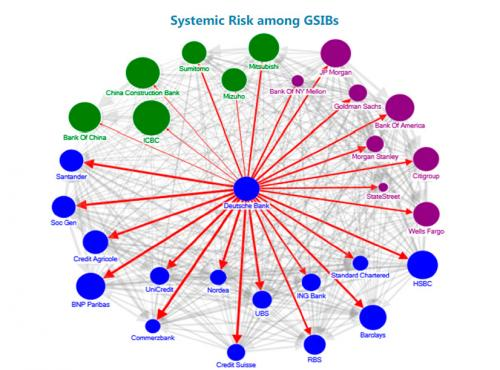

In particular, some of the largest “too big to fail banks” in the United States are “heavily interconnected financially” to Deutsche Bank. The following comes from Wall Street On Parade…

We know that Deutsche Bank’s derivative tentacles extend into most of the major Wall Street banks. According to a 2016 report from the International Monetary Fund (IMF), Deutsche Bank is heavily interconnected financially to JPMorgan Chase, Citigroup, Goldman Sachs, Morgan Stanley and Bank of America as well as other mega banks in Europe. The IMF concluded that Deutsche Bank posed a greater threat to global financial stability than any other bank as a result of these interconnections – and that was when its market capitalization was tens of billions of dollars larger than it is today.

Until these mega banks are broken up, until the Fed is replaced by a competent and serious regulator of bank holding companies, and until derivatives are restricted to those that trade on a transparent exchange, the next epic financial crash is just one counterparty blowup away.

As long as I have been doing this, I have been warning my readers to watch the global derivatives market. It played a starring role during the last financial crisis, and it will play a starring role in the next one too.

The fundamental structural problems that were exposed during 2008 and

2009 were never fixed. In fact, many would argue that the global

financial system is even more vulnerable today than it was back during

that time.

And now it appears that the next “Lehman Brothers moment” may be playing out right in front of our eyes.

Now more than ever, keep a close eye on Deutsche Bank, because it appears that they could be the first really big domino to fall.

__________________________________________

Now consider this: If the U.S. Federal Reserve can see fit to bailout Deutsche Bank and dozens of other major banks whose leveraged speculation schemes and worm-holed risk management strategies landed them in cavernous capital holes during the Great Financial Crisis….

And if Deutsche Bank, with its rapidly deteriorating balance sheet, is once again all all wired up in derivatives exposure with the same interconnected cast of global banks….

And the global financial system could be ‘setting up’ once again for another major crisis….

Then it is time, now, for the U.S. Federal Reserve to run their next round of massive liquidity infusions, through a “Citizens Credit Facility,” directly to U.S. citizens – to insulate them from the shock waves that are sure to follow.

The Leviticus 25 Plan is a dynamic economic

initiative providing direct liquidity benefits for American families,

while at the same time scaling back the role of government in managing

and controlling the affairs of citizens. It is a comprehensive plan

with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

According to the latest IIF Global Debt Monitor released today, debt around the globe hit $246 trillion in Q1 2019, rising by $3 trillion in the quarter, and outpacing the rate of growth of the global economy as total debt/GDP rose to 320%

NEW Global Debt Monitor: Global debt hit $246T in Q1 2019, nearly 320% of GDP.

Debt by sector, Q1 2019 (as % of GDP):

🔹Households: 59.8%

🔹Non-financial corporates: 91.4%

🔹Gov’t: 87.2%

🔹Financial corporates: 80.8% pic.twitter.com/4Qu0ekvpZw

— IIF (@IIF) July 15, 2019

[snip]

The IIF pointed out the obvious, namely that lower borrowing costs thanks to central banks’ monetary easing had encouraged countries to take on new debt. Amusingly, by doing so, this makes rising rates even more impossible as the world’s can barely support 100% debt of GDP, let alone 3x that.

[According to Sonja Gibbs the IIF’s managing director for global policy initiatives] “It’s almost Pavlovian. Rates go down and borrowing goes up. Once they are built up, debts are hard to pay down without diverting funds from other goals, whether that’s productive investment by companies or government spending.”

And that, in a nutshell, is why the world is doomed to a central-bank

created boom-bust cycle, as once there is just too much debt, there

will either by hyperinflation or a wave of global sovereign and

corporate defaults.

________________________________________________

This will not end well. In fact, it will end in financial chaos and economic disaster.

There is a way to clean this mess up, at least for the United States.

The Leviticus 25 Plan is the most powerful and dynamic ‘ground-level’ debt elimination plan on the face of the earth, eliminating massive tracts of household and consumer debt, along with federal, state and local government debt.

The Leviticus 25 Plan, in fact, produces $465 billion in federal government budget surpluses in each of the first 5 years following activation. Source: https://leviticus25plan.org/2019/03/

The Leviticus 25 Plan is a dynamic economic

initiative providing direct liquidity benefits for American families,

while at the same time scaling back the role of government in managing

and controlling the affairs of citizens. It is a comprehensive plan

with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Nomi Prins is a former managing director at Goldman-Sachs, a former Senior Managing Director at Bear Stearns, and a former senior strategist at Lehman Brothers and analyst at the Chase Manhattan Bank. She is currently an American author, journalist, and public speaker.

Too big to fail is a seven-year

phenomenon created by the most powerful central banks to bolster the

largest, most politically connected US and European banks. More than that, it’s

a global concern predicated on that handful of private banks controlling too

much market share and elite central banks infusing them with boatloads of cheap

capital and other aid.

Synthetic bank and market

subsidization disguised as ‘monetary policy’ has spawned artificial asset and

debt bubbles – everywhere.

The most rapacious speculative capital and associated risk flows from these

power-players to the least protected, or least regulated, locales.

There is no such thing as isolated

‘Big Bank’ problems. Rather, complex products, risky practices, leverage and

co-dependent transactions have contagion ramifications, particularly in

emerging markets whose histories are already lined with disproportionate shares

of debt, interest rate and currency related travails.

………………………………..

Prins: “I’m talking about an

entirely rigged political-financial system.”

________________________________

It is time to get the system… “de-rigged.” It is time to ‘level the playing field.’

The mechanism: Granting U.S. citizens the same direct access to liquidity extensions that the Fed so generously provided to Wall Street’s financial sector: Goldman Sachs, Bank of America, State Street, JP Morgan, Merrill Lynch, AIG, Morgan Stanley, UBS, Barclays, Royal Bank of Scotland, and many others – during the great financial crisis years (2008 – 2010).

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

July 2019 quote: “Taxation has surrounded itself with doctrines of justification; it had to; no miscreant can carry on without a supporting philosophy. Until recent times this pilfering of private property sought to gain the approval of its victims by protesting the need for maintaining social services. The growing encroachments of the state upon property rights necessarily brought about a lowering of the general economy, resulting in disaffection, and now taxation is advocated as a means of alleviating this condition; we are now being taxed into betterment.” – Frank Chodorov, “Socialism via Taxation” (1946)

_____________________________________________

There is one bright, clean economic solution with the raw power to re-fire America’s free enterprise engines. It will generate massive new tax revenue growth and reduce government social spending obligations. It will restore financial health to ‘ground level’ American families and Main Street America.

There is no other plan like it anywhere in the world.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

As the annual deficits begin to seriously ‘widen’ and the Federal government is forced to ‘float’ more paper, or ramp up its borrowing, there will evidently be a significant shortage of interested purchasers of that paper – at the target rates set by Treasury.

So…. the Federal Reserve will need to step in to ‘fill the gap.’ In other words, they will need to ‘create,’ out of thin air, new money. Lots of new money….

……………………………………………………..

The Daily Shot, Jun 2, 2019:

Rates: The Fed is expected to buy a great deal of Treasury bills as it resumes expanding its balance sheet.

Source:

Deutsche Bank Research

___________________________________________

Escalating fiat currency creation by the Fed, and other Central Banks, is certain to erode the value of money. And that, over the long term, is a threat to liberty – everywhere.

“It is impossible to grasp the meaning of the idea of sound money if one does not realize that it was devised as an Instrument for the protection of civil liberties against despotic inroads on the part of governments. Ideologically, it Belongs in the same class with political constitutions and bills of rights.” – The Theory of Money and Credit (1912), Austrian economist Ludwig von Mises

There is one economic acceleration plan that sets thing back in order. It eliminates vast amounts of public and private debt, balances the federal budget, and restores economic liberty for all Americans.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Bloomberg’s Bob Ivry discovered,

through an FOIA request, that the Federal Reserve had been running a “secretive

bailout operation between March and December 2008, under which banks borrowed

as much as $855 billion over the time frame for a rate as low as 0.01%.”

The Fed subsequently disclosed: “The

Federal Reserve System conducted a series of single-tranche term repurchase

agreements from March 2008 to December 2008 with the intention of mitigating

heightened stress in funding markets.

These operations were conducted by

the Federal Reserve Bank of New York with primary dealers as

counterparties…this program helped to address liquidity pressures evident

across a number of financing markets and supported the flow of credit to U.S.

households and business.” (Source: ZeroHedge 07/06/2011 –

Fed Releases Details On Secret $855 Billion Single-Tra… )

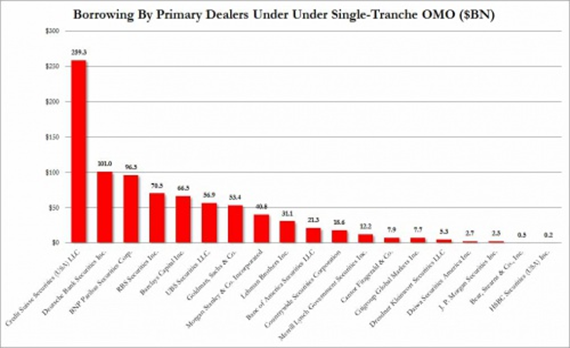

The 5 heaviest borrowers were foreign banks – raking in a cool $593 billion: Credit Suisse, Deutsche Bank, BNP Paribas, RBS and Barclays.

UBS Securities, LLC ($56.9 billion) was #6 on the list.

#7 Goldman Sachs received $53.4

billion – much of it borrowed at a rate of .01% (one basis point).

__________________

The Fed ‘created’ various funding

facilities during the financial crisis to bailout Wall Street’s financial

market: Term Auction Facility (TAF) Commercial Paper Funding Facility (CPFF) Primary Dealer’s Credit Facility (PDCF) Term Securities Lending Facility (TSLF) Asset-backed Commercial Paper Money Market Mutual Fund Liquidity Facility

(AMLF)

Wall Street financial institutions

also received massive liquidity transfusions at the Fed’s Discount Window (DW).

The one the Fed tried hard to keep out of the spotlight involved the “secret” single-tranche OMO’s – through which they ‘ladled out’ a whopping $855 billion.

Again, the Fed deemed this necessary

to mitigate the “heightened stress in funding markets” (translation: Wall

Street’s leveraged speculation strategies got broad-sided by the great mortgage

market default wave, and funding markets ‘seized up’).

In the Fed’s own words, the secret ST OMO program “helped to address liquidity pressures evident across a number of financing markets and supported the flow of credit to U.S. households and business” (translation: the biggest and mightiest financial institutions on Wall Street had suddenly developed gaping capital holes… many were on the verge of ‘going under’… and they needed a liquidity lifeline to survive). ________________________

Fast forward to 2019. It is now time to “mitigate heightened stress” and to “address liquidity pressures” that have been experienced by American families over the past decade. It is time to grant U.S. citizens the same direct access to liquidity that was ‘”secretly” provided to major U.S. and foreign banks..

The Leviticus 25 Plan is a dynamic economic initiative providing direct

liquidity benefits for American families, while at the same time scaling back

the role of government in managing and controlling the affairs of

citizens. It is a comprehensive plan with long-term economic and social

benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Populist solutions for serious, mainstream issues are known to take root and blossom in an era when public policies have shifted dramatically in favor of government control over people’s lives, and unabashedly favor wealthy, politically-connected individuals and groups.

Populist fervor thrives when public

policies have so distorted the economic and social landscapes that trust in

government is lost.

William A. Galston (WSJ – Dec 16, 2014) summarized the hallmarks of the current populist wave several years ago: Populist movements flourish when established leaders and parties fail to solve their countries’ most urgent problems. Throughout the market democracies, one problem dominates all others: the economic squeeze on working- and middle-class families. Neither the center-left nor the center-right has responded in ways that make sense to rank-and-file citizens. So they are looking elsewhere.

Populism offers many satisfactions.

Its narrative is clear and easy to understand. It identifies villains—corrupt

officials, unresponsive bureaucracies, arrogant elites, large corporations, giant

banks…

It legitimizes outrage, the

expression of which is one of the greatest human pleasures. It flatters the

people, whose virtue and common sense, it claims, could set the country right

if only rich and powerful forces didn’t stand in their way. “The humblest

citizen in all the land,” declaimed William Jennings Bryan more than a century

ago, “when clad in the armor of a righteous cause, is stronger than all the

whole hosts of error that they”—the elites—“can bring.”

Populism is the politics of nostalgia.

It appeals to a better time in the past…. The ills against which populists inveigh are rarely illusory. On the

contrary: Populism typically gives voice to genuine grievances, and in so doing

gains credibility and energy.

At the heart of the American dream is the promise of opportunity. But in the ABC/Washington Post survey conducted days before the 2014 midterm elections, 71% of Americans said the U.S. economic system generally favors the wealthy. Only 24% disagreed. The favors-the-wealthy super-majority included 54% of Republicans, 59% of conservatives, 64% of college graduates—and even 57% of those making more than $100,000 per year. _________________________________

Government leaders in America over the past several decades have failed to solve our nation’s most urgent problems,” both social and economic. The same can be said for the governments of many other nations around the world.

Governments have not “responded in

ways that make sense to rank-and-file citizens.”

The Leviticus 25 Plan appeals to “virtue and common sense….its narrative is clear

and easy to understand. It identifies villains – corrupt officials,

unresponsive bureaucracies, arrogant elites, large corporations, giant banks…”

The Leviticus 25 Plan levels the playing field. It grants individual citizens the same direct access to liquidity that was awarded to the likes of Morgan Stanley, Goldman Sachs, UBS, Citigroup, Bank of America, State Street, Merrill Lynch, AIG, Deutsche Bank, Barclays, GE Capital, and many, many others during the financial crisis years of 2007-2010..

The Leviticus 25 Plan provides for massive debt relief and economic liberty for ‘ground level’ America. It unleashes the power of free-market dynamics and counters price and supply distortions that have thrived with government control over markets.

It generates massive government tax

revenues – without raising taxes. And it pays for itself over a 10-15

year period.

This is the only plan, anywhere, that restores order, and cleans up corruptive influences, and re-fires the engines of economic growth..

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The gravy train stopped at Russia’s doorstep in the spring of 2015 to drop off $60 million in U.S. taxpayer dollars. Yes, this is the same Russia that annexed Crimea and invaded Ukraine. The same Russia that has been provoking Europe and the U.S. – and rattling its nuclear saber.

Fox News – April 9,

2015

UN paid Russian air charters hundreds of millions while Putin invaded

Ukraine Excerpts: EXCLUSIVE: In the 14 months since Russian President Vladimir Putin annexed

Crimea and sent proxy fighters to invade eastern Ukraine, Russian companies

have won more than $212 million in United Nations contracts to ferry troops,

supplies and equipment — on peacekeeping missions.

The tally amounts to nearly

one-third — 32 percent — of the money U.N. headquarters has spent on

peacekeeping air transport during that time, according to the U.N.’s

procurement website.

The U.S. pays 28.4 percent of all

U.N. peacekeeping expenses, so the Obama administration’s contribution to

the Russian bottom line amounts to more than $60 million.

_____________________________

America has been leaking out a lot of money over the last decade – to help bailout Ukraine, Greece, Egypt, and other financially stressed nations. And now we’re leaking $60 million in new money to Russia via obligatory deals they have with the U.N..

This is all on top of the trillions

of dollars in direct cash transfers, discount window access, credit guarantees,

and toxic asset purchases that our government and Federal Reserve employed to

bail out Wall Street’s financial sector during the financial crisis 2008-09.

This asymmetrical largess has gone on long enough. It is now time to even things out and grant the same direct liquidity access for U.S. citizens that our government and the Federal Reserve have been providing to foreign nations and foreign banks..

The Leviticus 25 Plan is a powerful economic acceleration plan that restore financial health for American families, stimulates long-term economic growth and stability, and generates $465 billion budget surpluses at the federal level over each of its first five years of activation.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

“The IMF is delighted to announce that it just approved a €3.2 billion disbursement of cash for Greece, its fifth, as part of the €12 billion in money that Greece needs in order to continue operating in the months of July and August. And just for what purpose will this money be used, one may ask? Well, as explained a few weeks ago, in Greek Math: €12 Billion In, €18.2 Billion Out the entire amount will be promptly recycled by global financial institutions in the form of debt maturities and interest payments, which amount to €18.2 billion in the months of July and August.

Simply said ECB, EU and IMF money

in, money owed to bankers out. The kicker: 17.09% of the money coming from the

IMF, comes from, that’s right dear US taxpayer, you (and since 21% of the quota

contributions allocated to the IMF are deemed “non-usable”, the

actual number funded by the US is likely much higher).

But this plot has a bonus kicker: …

the actual Greek debt is no longer owed by European banks to the extent it had

been previously expected: a development that threatens to scuttle the entire

second Greek bailout plan as currently proposed. So as the banks have been

selling Greek debt, who has been buying?

Mostly hedge funds…

So to recap: US taxpayers have just paid out about $780 million of the $4.6 billion in order to fund interest owed to… hedge funds.“

______________________________________

This begs the question: If the U.S. government can funnel U.S. tax-payer dollars to bailout Greece, to the tune of $780 million, in order to help Greece make their interest payments to … hedge funds, then should not U.S. citizen taxpayers receive that same direct access to liquidity to help Americans eliminate debt at the family level?

Answer: Yes.

The Leviticus 25 Plan is a dynamic economic

initiative providing direct liquidity benefits for American families,

while at the same time scaling back the role of government in managing

and controlling the affairs of citizens. It is a comprehensive plan

with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

{kind=link}