Average annual budget surplus (projected) 2027-2031: $186.517 billion / 5 years: $37.303 billion per year

Note 1: Projected budget surpluses for 2027-2031 do not factor in the additional government tax revenue gains that would accrue from the massive shift in capital away from debt service and into productive economic activity.

Note 2: Projected budget surpluses for 2027-2031 do not factor in the additional government tax revenue gains that would accrue from significantly lower levels of debt deductibility on individual income tax filings.

Note 3: Projected budget surpluses from the Medicaid / CHIP recapture do not take into account the likelihood of fewer citizens actually qualifying for Medicaid / CHIP benefits.

Note 4: Projected budget surpluses from Interest Expense Reductions during each of the first five years of activation (2027-2031) is likely understated due to the fact that ‘debt held by the public’ is projected to increase by 8.5% per year, from $28.278 trillion in 2026 to $40.198 trillion in 2030.

Note 5: The Plan’s funding of individual Medical Savings Accounts (MSAs) with the $7,000 deductible provision per year would result in an enormous drop in the number of claims each year for Medicare reimbursement. Medicare payroll taxes would generate a growing revenue stream, due to stronger economic growth, while outlays would drop significantly from the reduced claims numbers – thereby providing the Fed / Treasury Department with a powerful recapitalization of the Medicare Trust Fund, via the Citizen’s Credit Facility.

The Leviticus 25 Plan – Projection limitations There can be no question that The Leviticus 25 Plan would generate healthy, broad-based economic growth from broad-based debt reduction and improved financial stability at the family level, the restoration of free market dynamics in commerce, and scaling back social program work disincentives.

The Leviticus 25 Plan does not attempt to project how much additional tax revenue and reduced cost of government will be realized, above and beyond the Recapture Provisions, over the course of the initial five years of the plan. In that sense, The Plan understates the effect of additional dynamic economic benefits.

Robust funding of Medical Savings Accounts and the elimination of millions of insurance claims and claims resolutions for basic primary care and everyday healthcare purchases swill save millions of man-hours of health care cost on an annual basis. Scaling back government involvement in basic primary care and everyday healthcare purchases for millions of Americans will also generate massive cost savings.

The Plan makes no attempt to project the positive effects of the streamlined, consumer-driven efficiencies that will emerge, and the cost reduction and improvement in services. The Plan therefore understates the benefits. The Plan projects an 80 percent participation rate by U.S. citizens. It is assumed that a large number of wealthy Americans will not participate, because their tax refunds are larger than the annual Plan benefits. And it is assumed that a large number of Americans receiving significant government benefits for extraordinary health or economic issues will also not participate.

Cost savings from the reductions in massive social welfare spending and other programs, like unemployment insurance, workman’s compensation, SSI and SSDI can be difficult to quantity, since state and federal funding mechanisms may both be involved in various ways. In that regard, The Plan may understate, or it may overstate, the benefits.

The Leviticus 25 Plan 2027 – the world’s most powerful economic acceleration plan: Updated economic scoring summary.

Interest expense on projected deficits 2027-2031

Federal debt has increased from $22.1 trillion in 2020 to $37.64 trillion as of July 1, 2025. Federal debt held by the public was reported to be $30.298 trillion, with remainder, $7.342 trillion, comprised of intra-governmental debt outstanding, which arises when one part of the government borrows from another. This intra-governmental debt interest expense item will be omitted from this calculation, since those dollars are not expensed directly.

St. Louis Fed Q3 2025: Debt held by the public, $30.3 trillion, makes up 80.0% of the $37.64 trillion National Debt. U.S. Department of the Treasury (fiscal data): Interest Expense and Average Interest Rates on the National Debt FYTD 2026: 3.324%

The Bear Traps Report, Dec 30, 2024–Excerpts: “CBO data, Bloomberg. The average weighted coupon on the U.S. debt load is about 2.7% vs. over 4.5% for 10-year U.S. Treasuries. As bonds mature, they get refinanced at much higher yields.”

“Incoming Stress Points – In 2025 the U.S. Treasury faces $9.6Tr of maturities in their so-called publicly held debt. In Q1 alone — the government faces $5.58Tr of maturities (bonds coming due, redemption), but 86% of those are short-term bills that the Treasury department rolls over into new 4-week, 8-week, 3,4, or 6-month bills, among others.”

“As a result, almost daily bill auctions are coming to a theater near you, as the Treasury Department mindlessly keeps pushing new paper into the market to pay back the colossal amount of maturing debt.”

This projection will assume an average monthly interest rate of 3.324% for 2026, and a conservative average monthly interest rate of 3.25% in calculating the interest expense to be eliminated during the budget surplus years of 2027-2031. This projection also assumes that annual federal budget deficits will be funded through Treasury Issuance at an average of 80.0% rate for Debt Held by the Public.

Year / Annual Deficit/2 2025: $1.865 trillion/2 X .79 X .03 = $22.965 billion 2026: $1.713 trillion/2 X .79 X .03 = $21.934 billion 2027: $1.687 trillion/2 X .80 X .0325 = $21.931 billion 2028: $1.911 trillion/2 X .80 X .0325 = $24.843 billion 2029: $1.938 trillion/2 X .80 X .0325 = $25.194 billion 2030: $2.140 trillion/2 X .80 X .0325 = $27.820 billion 2031: $2.233 trillion/2 X .80 X .0325 = $29.029 billion

Recapture: Total interest expense eliminated by projected operating surpluses: $128.817 billion

The Leviticus 25 Plan 2027 – the most powerful economic acceleration plan in the world: Updated economic scoring summary.

Medicaid/CHIP Recapture Each U.S. citizen participating in The Plan will receive a $35,000 deposit, funded through a Federal Reserve / U.S. Treasury Department-based Citizens Credit Facility, into a personal Medical Savings Account (MSA).

The Leviticus 25 Plan assumes 80% participation by Medicaid / CHIP enrollees. Within this comprehensive economic plan, The U.S. Health Care Freedom Plan provides Medical Savings Account (MSA) funding of $35,000 to cover the $7,000 deductible for Medicaid and CHIP eligible primary care events and select out-patient care services – primarily related to routine medical appointments, Medicaid prescription events, disease state monitoring clinics, and other desired primary care services.

September 2025 Medicaid & CHIP Enrollment – 77.05 million individuals were enrolled in Medicaid and CHIP in the 50 states and the District of Columbia that reported enrollment data for September 2025. 69,797,328 people were enrolled in Medicaid; 7,252,967 enrolled in CHIP.

Using a conservative estimate of 77.0 million for 2025, with a projected annual growth rate of 2%: 2025: 77.00 million 2026: 78.54 million 2027: 80.11 million 2028: 81.71 million 2029: 83.34 million 2030: 85.10 million 2031: 86.80 million

Total: 417.06 million receiving benefits 2027-2031

Average annual enrollment (2027-2031): 83.41 million 83.41 million X .8 = 66.728 million X $7,000/year X 5 years = $2.335 trillion

Total Medicaid/CHIP recapture during the 5-year target period (2027-2031): $2.335 trillion

Medicare Recapture Each U.S. citizen participating in The Plan will receive a $35,000 deposit, funded through a Federal Reserve / U.S Treasury Department-based Citizens Credit Facility, into a personal Medical Savings Account (MSA).

The Leviticus 25 Plan assumes 80% participation by Medicare enrollees. Within this comprehensive economic plan, The U.S. Health Care Freedom Plan provides Medical Savings Account (MSA) funding of $35,000 to cover a $7,000 annual deductible for Medicare-eligible primary care events and select out-patient services – primarily related to routine medical appointments, Medicare Part D prescription events, disease state monitoring clinics, and other desired primary care services.

There were 69.6 million people were enrolled in Medicare as of October 2025.

Projection: “Medicare spending grew 7.8% to $1,118.0 billion in 2024, or 21 percent of total National Health Expenditures.”

“Over 2024-33 average NHE growth (5.8 percent) is projected to outpace that of average Gross Domestic Product (GDP) growth (4.3 percent), resulting in an increase in the health spending share of GDP from 17.6 percent in 2023 to 20.3 percent in 2033.”

“Medicare enrollment is projected to grow steadily, with total beneficiaries rising to an estimated 78-79 million by 2030-2031.”

Applying a conservative projected enrollment growth rate of 2.5% annually through 2031, with an 80% participation rate, and a $7,000 annual deductible for the 5-year target period (2027-2031): 2025: 69.60 million X .8 X $6,000 = $334,080,000 2026: 71.34 million X .8 X $6,000 = $342,432,000 2027: 73.12 million X .8 X $7,000 = $409,472,000 2028: 74.95 million X .8 X $7,000 = $419,720,000 2029: 76.82 million X .8 X $7,000 = $430,192,000 2030: 78.74 million X .8 X $7.000 = $440,994,000 2031: 80.70 million X .8 X $7,000 = $451,920,000

Total Medicare recapture during the 5-year target period (2027-2031): $2.152 trillion

VA Healthcare The Leviticus 25 Plan assumes 80% participation by Veterans Administration healthcare enrollees. Within this comprehensive structure, The U.S. Health Care Freedom Plan provides Medical Savings Account (MSA) funding of $35,000, through a Federal Reserve / U.S. Treasury-based Citizens Credit Facility, to cover annual $7,000 deductibles for VA primary healthcare services over the course of the 5-year target period (2027-2031).

FY 2025 – 9.2 million enrollees in the VA health care system. The plan assumes a stable 9.2 million enrollment in the VA Health Care System.

2027: 9.2 X 0.8 X $7,000 = $51,520,000,000 2028: 9.2 X 0.8 X $7,000 = $51,520,000,000 2029: 9.2 X 0.8 X $7,000 = $51,520,000,000 2030: 9.2 X 0.8 X $7,000 = $51,520,000,000 2031: 9.2 X 0.8 X $7,000 = $51,520,000,000

Total recapture: $257,600,000,000

Average annual recapture (2027-2031): $51.52 billion

TRICARE The Leviticus 25 Plan assumes 80% participation by qualified TRICARE enrollees.

Through The U.S. Health Care Freedom Plan component, participating members will receive a Medical Savings Account (MSA) funding injection of $35,000, through a Federal Reserve / U.S. Treasury Department-based Citizens Credit Facility, to cover annual $7,000 deductibles for desired primary care and out-patient services over the course of the 5-year target period (2027-2031).

There are currently ~9.4 million U.S. citizen beneficiaries in various locations around the world. Recapture – total (2027-2031): 9.4 million X 0.8 X $7,000 X 5 years: $263.2 billion

Federal Employee Health Benefits (FEHB) The Leviticus 25 Plan assumes 80% participation by FEHB enrollees. Participating members will receive a Medical Savings Account (MSA) funding injection of $35,000, through a Federal Reserve / U.S. Treasury Department-based Citizens Credit Facility, to cover annual $7,000 deductibles for desired primary care and out-patient services over the course of the 5-year target period (2027-2031).

FEHB Program carriers cover most active, full-time civilian employees and retirees of the U.S. government and their families. The Program now provides benefits to over 8.2 million federal enrollees and dependents and offers over 180 health plan choices to federal members.

Note – the Federal government also pays approximately 72% of premium costs per enrollee. Recapture – total (2027-2031): 8.3 million X 0.8 X $7,000 X 5 = $229.6 billion

Social Security Disability Income (SSDI) The Leviticus 25 Plan specifies that qualifying participants will not be eligible for SSDI benefits. The Plan assumes 80% participation by SSDI recipients.

December 2025 – total beneficiaries: 8.163 million recipients; Total monthly SSDI benefit payments: $12.182 billion; Total annual SSDI benefit payments: $146.184 billion.

This projection assumes a conservative 3% growth per year for 2027-2031, covering both enrollment growth and COLA: 2025: $146.184 billion 2026: $150.570 billion 2027: $155.087 billion 2028: $159.740 billion 2029: $164.532 billion 2030: $169.468 billion 2031: $174.552 billion

Total: $823.379 billion / Average per year: $164.676 billion

Total for 5-year target period 2027-2031: Plan assumes 80% participation – recapture: $823.379 billion X 0.8 = $658.70 billion

“SSDI benefits are financed primarily by part of the Social Security payroll tax..”

“Social Security’s trustees project that the share of people in the United States receiving SSDI will rise somewhat over the next 20 years and then remain stable.”

Note: The 3% growth projection, covering both the enrollment increase and annual COLA, is likely a conservative estimation for the period 2027-2031.

The Leviticus 25 Plan – the most powerful economic acceleration plan in the world: Updated economic scoring summary.

Federal Income Tax Recapture This scoring model assumes that 80% of qualified U.S. citizens will voluntarily participate in The Leviticus 25 Plan. Participants must give up their tax refunds through the Plan’s recapture provisions for the 5-year target period (2027-2031).

According to 2025 IRS Filing season statistics, through Dec 28, 2025: 103,846,000 total refunds were paid out, totaling $328.878 billion.

Refund totals have increased by approximately $25.117 billion over the past eight years, from $303.761 billion (2018) to a current (estimated) $328.878 billion (2025), representing an average increase of $3.14 billion per year.

A conservative estimated average of $3.1 billion per year (2027-2031) will be used for this recapture calculation. 2024: $329.1 billion (actual) 2025: $328.9 billion (actual) 2026: $332.0 billion 2027: $335.1 billion 2028: $338.2 billion 2029: $341.3 billion 2030: $344.4 billion 2031: $347.5 billion

Total: $1.707 trillion

Total recapture X 80%: $1.707 trillion X .8 = $1.366 trillion

Total recapture per annum (2027-2031): $1.366 trillion / 5 = $273.2 billion

Participants in the Plan will forego Economic Security Program benefits and select means-tested welfare benefits for the period 2027-2031.

Economic security programs: Outlays were about 10 percent (or $701.6 billion) of the federal budget in 2025, in funding [safety net] programs that provide aid (other than health insurance or Social Security benefits) to individuals and families facing hardship. Economic security programs include: the refundable portions of the Earned Income Tax Credit and Child Tax Credit, which assist low- and moderate-income working families; programs that provide cash payments to eligible individuals or households, including unemployment insurance and Supplemental Security Income for low-income people who are elderly or disabled; various forms of in-kind assistance for low-income people, including the Supplemental Nutrition Assistance Program (formerly known as food stamps), school meals, low-income housing assistance, child care assistance, and help meeting home energy bills; and other programs such as those that aid abused or neglected children.1

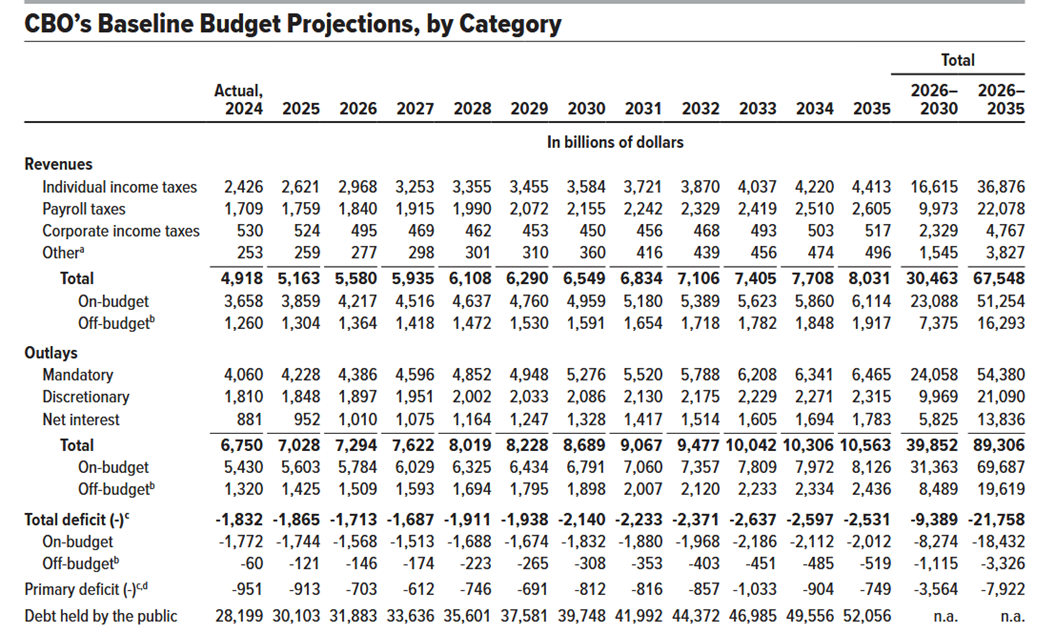

The Leviticus 25 Plan will generate annual budget surpluses of $37.303 billion during each of the first five years of activation (2027-2031), versus the CBO-projected $1.982 trillion average annual deficits, representing a positive budget gain of $2.019 trillion annually for the period.

Budget surpluses would be negotiable for partial transfer back to the Federal Reserve to effect ongoing reductions of the Citizens Credit Facility balance sheet. More importantly, $37.303 billion annual budget surpluses would provide a dynamic counterbalance to the inevitable demands on the Fed to purchase T-Bills and T-Bonds in support of Treasury Auctions throughout 2027-2031.

Overview, Primary Assumptions, Economic Scoring

The Leviticus 25 Plan activation period is slated for the 5-year period beginning in 2027 and ending in 2031.

The Leviticus 25 Plan – Each participating U.S. citizen will receive a $60,000 deposit into a Family Account (FA) and a $35,000 deposit into a Medical Savings Account (MSA).

All U.S. citizens residing in the United States are eligible to participate, contingent upon meeting qualification standards and agreement to specified recapture provisions. Participants (other than ‘custody account’ applicants) must prove stable credit history, stable job history, no recent drug/felony convictions.

These general recapture provisions include:

Waiving all federal income tax refunds for a period of 5 years.

Waiving benefits from economic security programs, select benefits from means-tested welfare programs, SSI, and SSDI for a period of 5 years.

Enrollees in the Medicare, VA Healthcare system, Federal Employees Health Benefits (FEHB), and TRICARE will be subject to a $7,000 deductible for primary care and outpatient services annually for a period of 5 years. (See full plan for more details)

Primary scoring assumptions:

The Plan assumes an 80% participation rate by U.S. citizens. Wealthier Americans would choose not to participate, due to the comparative benefit of income tax refund amounts. Many individuals of lower socio-economic sector would also choose not to participate, due to the comparatively high benefits profiles that they would not wish to give up.

The Plan assumes that participating families would use significant funds to pay down / eliminate debt, and that these longer-term, lower debt service obligations would enhance the financial security of participating families for several decades beyond the opening activation period. Federal, state, and local government entities would benefit from longer-term tax revenue growth and reduced citizen dependence on government-based entitlement program benefits.

The Plan assumes that dynamic new efficiencies would emerge in the healthcare system – with more families managing/directing healthcare expenditures through their MSAs.

The Plan assumes that apart from the recapture provisions, there would also be significant tax revenue growth for federal, state and local government entities from free-market economic revitalization, more people working and paying taxes, and from the elimination of various income tax deductions (e.g. mortgage / HELOC interest expense).

The Plan assumes that there would not be a massive full-scale move back into the means-tested welfare programs, income security programs, SSI, and SSDI at the end of the initial 5-year activation period.

The benefits of a free-market economy and newfound economic liberty for American families would provide positive economic inertia throughout years 5-10, and for several decades beyond.

Recapture provisions would provide substantial federal budget surpluses for each year of the initial 5-year period. Economic growth over the following 10-15 years would generate sufficient recapture funding and tax revenue growth to offset the entire initial Federal Reserve balance sheet expansion.

Significant inertia from The Plan would also provide on-going, market-based growth benefits over succeeding years that far exceed any prospect for healthy economic growth that may be expected under America’s current big-government, central-planning approach.

Dynamic economic benefits would flow from:

Family level massive debt elimination, financial security gains.

Timely, sweeping reversal of big government “central planning” control.

Productivity gains from reversal of work disincentives currently embedded in social programs.

Stabilization of bank capitalization, housing market.

Strengthen / stabilize long-term value of U.S. Dollar.

Minimizing the role of government in managing, directing, controlling the affairs of citizens.

Federal Budget Deficit Projections – Congressional Budget Office The Budget and Economic Outlook: 2025-2035 projects budget deficits ranging from $1.713 trillion 2026 to $2.140 trillion in 2030, and on up to $2.531 trillion by 2035. Actual deficits for the out years are likely to be higher than CBO projections, based upon history (“actual” versus “projected”).

“You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete. –R. Buckminster Fuller

Congress responded to the COVID-19 pandemic by passing the American Rescue Plan Act in early 2021. This $1.9 trillion spending bill was intended to provide relief and spark an economic recovery.

Among other provisions, the law expanded the availability of government-subsidized health care through the Obamacare Marketplace to help low- to middle-income people maintain health coverage until the economy normalized.

The measure brought millions of middle-class Americans into Obamacare, but had the unintended consequence of making many of them dependent on government aid.

The law also introduced temporary, enhanced subsidies, which raised Obamacare premiums, some observers say.

Though the enhanced subsidies expired on Dec. 31, 2025, Congress continues to debate their possible reinstatement.

…………………

During the pandemic, Congress created subsidies that had no income cap. These enhanced subsidies also lowered enrollees’ affordability cap—the maximum amount a customer would pay out of pocket for a monthly premium.

Under the enhanced subsidies, introduced in 2021, no enrollee would spend more than 8.5 percent of their monthly income on premiums. Some would pay no more than 6 percent, others 4 percent or 2 percent, and some would pay nothing.

Enrollment boomed, jumping from 11.4 million to 14.5 million in two years. By 2025, enrollment had doubled from its pre-pandemic level, topping 24 million, according to data from health research organization KFF.

The enhanced subsidies were set to expire in 2022, allowing just enough time to get people back to work.

But when the pandemic ended, the enhanced subsidies remained.

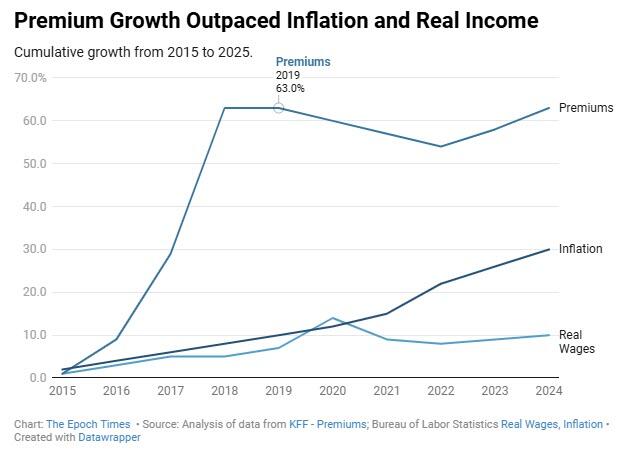

Premiums Increased, Wages Didn’t – Health insurance premiums increased dramatically during Obamacare’s first five years. The average individual premium for a 40-year-old went up at least 75 percent, according to data reported by KFF.

Prices soared in commercial markets, too, where the cost of individual premiums rose about 120 percent from 2013 to 2019, according to The Heritage Foundation.

Obamacare prices leveled out before the pandemic hit and from 2020 to 2022, which includes the first two years of enhanced subsidies, prices dropped 5 percent, according to data reported by KFF.

But in 2022, the year the subsidies were set to end, inflation was on the rise, peaking at more than 9 percent by midyear, according to the Bureau of Labor Statistics.

Economists broadly agree that this was an unintended consequence of American Rescue Plan spending. The rising prices were “the product of easy fiscal and monetary policies, excess savings accumulated during the pandemic, and the reopening of locked-down economies,” Ben Bernanke, former chairman of the Federal Reserve, wrote in a co-authored assessment for Brookings.

Congress responded by spending even more money. The Inflation Reduction Act, passed in August 2022, would pump another $1.2 trillion into the economy within a decade, the Cato Institute estimated. That included a three-year extension of the enhanced subsidies.

Obamacare premiums shot back up, according to data reported by KFF, rising more than 13 percent in three years.

…………………………..

“The [Affordable Care Act] subsidy structure is itself inflationary—driving up health care prices and total premiums,” said Mark Howell and Brian Blase of the think tank Paragon Health Institute. “As Congress considers the future of the COVID Credits . . . it must confront the reality that the [Affordable Care Act] made coverage far less affordable.”

That reality was largely hidden from many who received the enhanced subsidies because their out-of-pocket premium payments were capped based on income. Price hikes above that cap were paid by taxpayers, which meant the enhanced subsidies were now even more important for people with modest incomes.

………………………………..

There has been no dispute among lawmakers that the enhanced subsidies have been a boon to consumers.

The average Obamacare premium for 2025 was $619 per month, of which subsidies covered more than $500. More than 10 million enrollees, 46 percent of those receiving aid, paid $10 or less per month out of pocket for premiums.

That’s exactly the problem, according to some analysts, because the possibility of enrolling large numbers of people who would never receive a bill created a ripe opportunity for fraud.

Many people were enrolled in the program without their knowledge by unscrupulous insurance brokers, Blase alleges, prompting the federal government to send a commission check to them—and premium payments to an insurance company.

These phantom enrollees are detected in part by their lack of activity once enrolled, Blase said.

“In 2024, nearly 12 million enrollees did not use their plan a single time—up from fewer than 4 million in 2021,” Blase told the House Judiciary Committee on Dec. 10.

Overall, 35 percent of all exchange enrollees never used their plan, and 40 percent of fully subsidized enrollees did not have a single claim, which Blase said is double the rate in both the commercial market and pre-pandemic Obamacare.

America’s Health Insurance Providers, the trade association for health insurance companies, disputed that claim.

“A ‘no-claims’ year is evidence that a consumer stayed healthy or only had a few months of coverage—not that taxpayer money was misdirected or that their policy was illegitimate,” the group said in an Aug. 18 statement.

Yet in December 2025, the Government Accountability Office provided evidence of enrollment fraud in Obamacare that suggests fake accounts are being created.

Investigators were able to enroll 20 nonexistent identities in Obamacare in 2024 by using Social Security numbers that had never been issued to any person and other easily created counterfeit documents.

Of the 20 false enrollments, 18 were still active in September 2025, costing taxpayers more than $10,000 per month.

Investigators also found 26,000 accounts that received subsidies in 2023 based on Social Security numbers that matched records in the Social Security Administration’s death file.

More than 7,000 Social Security numbers belonged to people who were reported dead before enrolling in Obamacare, and 19,000 Social Security numbers matched death data by number but not name and address, indicating that false identities may have been created for enrollment.

Taxpayers paid more than $94 million in subsidies for one year based on those numbers.

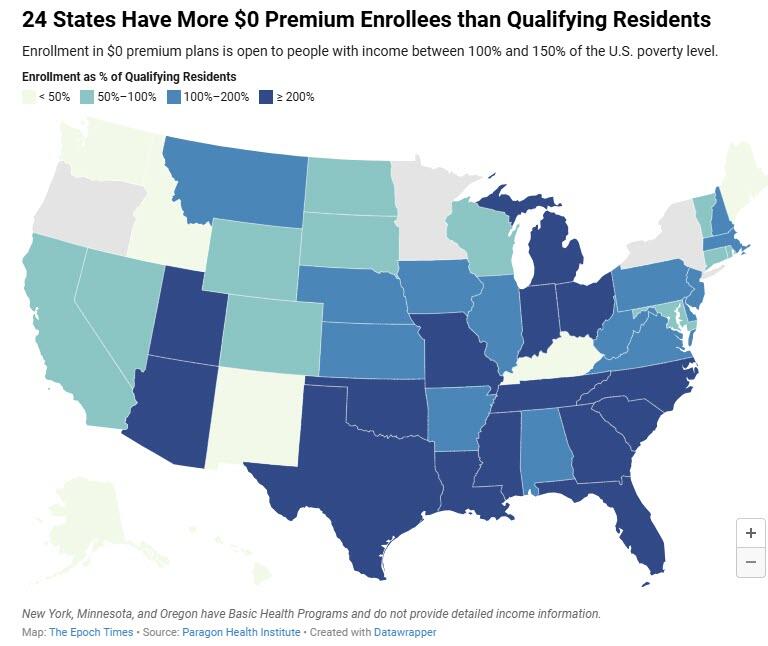

Another indication of fraud is the number of states where enrollment in Obamacare plans with a $0 premium is unreasonably high compared to the number with a qualifying income.

Twenty-four states have more Obamacare enrollees claiming incomes between 100 percent and 150 percent of the federal poverty level than there are people living in the state with that income, according to data from the U.S. Census Bureau.

The problem appears worse in states that have not adopted expanded Medicaid, which would have increased Medicaid eligibility to 138 percent of the federal poverty level.

Obamacare customers are automatically re-enrolled each year, so a fictitious account would continue to generate fraudulent commissions and wasteful insurance payments until detected.

Fraudulent enrollment costs up to $20 billion per year, according to Paragon Health Institute.

Making Health Care Affordable – The enhanced subsidies expired on Dec. 31, 2025. Congressional Republicans and Democrats continue to agree that the U.S. health care system has become unaffordable and want to address the problem. They differ in approach.

Democrats generally favor government intervention in the system, as in the case of Obamacare, where taxpayers pitch in to cover rising costs.

The Senate in December 2025 rejected a proposal to make the enhanced subsidies permanent. House Minority Leader Hakeem Jeffries (D-N.Y.) said at a press conference on Jan. 5 that his party continues to seek an extension of the subsidies “to protect the health care of tens of millions of … everyday Americans, middle-class Americans and working class Americans.”

Without the subsidies, Jeffries said, some consumers would face cost increases of up to $2,000 or more per month.

Republicans generally favor using the power of government to create marketplace competition. Senate Republicans recently presented a plan to provide dedicated funds directly to consumers, which they could use to shop for health care. That plan, too, was rejected by the Senate.

Sen. John Thune (R-S.D.), the Senate majority leader, addressed the differing philosophies in a Dec. 16, 2025, press conference.

“If [Democrats are] willing to accept changes that actually would put more power and control and resources in the hands of the American people, and less of that in the pockets of the insurance companies, I think there’s a path forward,” he said.

President Donald Trump has said he would veto any extension of Obamacare subsidies that came to his desk.

_____________________________________

To Sen. John Thune: Main Street America Republicans have the plan that “would [indeed] put more power and control and resources in the hands of the American people, and less in the pockets of the insurance companies.”

It is a plan that will overwhelmingly win over the hearts and minds of U.S. citizen voters, and get America back on track as a world economic leader.

The Leviticus 25 Plan will reestablish a strong, market-based, citizen-centered health care system in America.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The Leviticus 25 Plan is a clean and powerful, economically viable, and politically feasible master plan to dramatically reduce government handout programs – and end the billions of dollars lost to fraud, waste, and inefficiency each year in the U.S..

…………………………………………………..

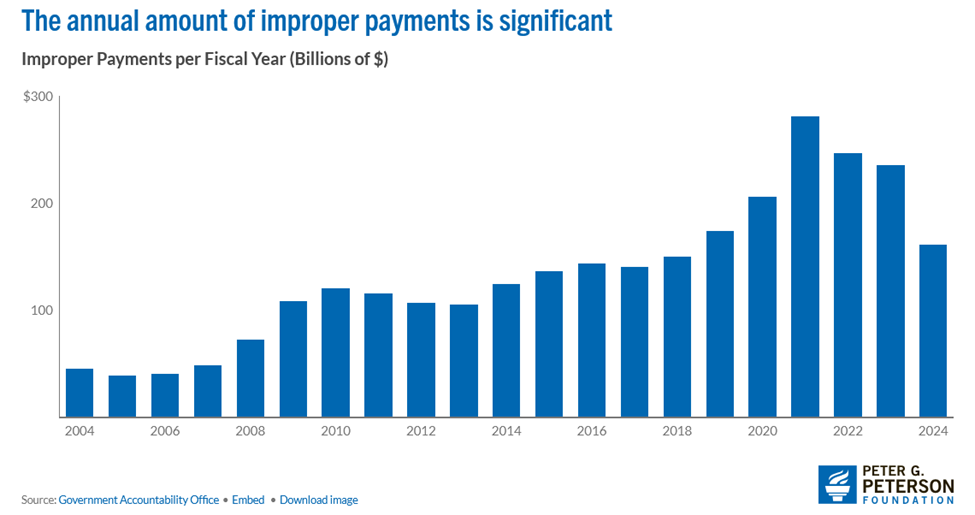

Peter G. Peterson Foundation Report Apr 17, 2026 About $121 billion, or 75 percent, of the improper payments in 2024 came from the following five programs. Each program has been or currently is on GAO’s High Risk List, meaning the capacity for fraud and waste within the program had been identified prior to the recent report.

SBA Investigating $1.2 Trillion On Payments As Part Of Fraud Probe: Loeffler ZeroHedge, Jan 13, 2026 – Authored by Travis Gilmore and Jen Jekielek via The Epoch Times, Excerpt: Federal officials are reviewing approximately $1.2 trillion in payouts to root out fraudsters, according to Kelly Loeffler, administrator of the Small Business Administration (SBA). “Federal contracting and the fraud that happens within it in Washington, D.C., around these programs are probably the worst kept secret in Washington,” Loeffler said ….

……………………………………

WSJ Letters: Get to the bottom of what went wrong with pandemic unemployment benefits before it happens again. Dec. 19, 2022 – Excerpt: Regarding Rep. James Comer’s op-ed “Get Ready for Republican Oversight” (Dec. 12): When it comes to pandemic-relief fraud, there is no time to waste. Pandemic unemployment benefits were hardest hit, with estimates of fraud and abuse as high as $400 billion—the equivalent of a decade and a half of regular unemployment benefit payments. Criminal gangs, including some based in Russia and China, used stolen identities to seize U.S. tax dollars on an industrial scale.

_____________________________________

The Leviticus 25 Plan will restore financial health for millions of U.S. citizen families and thereby eliminate the dependency of vast numbers of people on the myriad of loosely regulated government programs.

The Leviticus 25 Plan will reduce government outlays and generate trillion of dollars in new tax revenue for federal, state, and local government entities.

This dynamic economic acceleration plan is loaded up and ready to launch.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Main Street America Republicans have the one and only economic acceleration plan on record with the raw power to eliminate public and private debt, strengthen the U.S. economy, and restore financial health for millions of hard-working American families….

When asked how far the US government has plunged into the red, many fiscally-conscious Americans will tell you the national debt has reached $37 trillion. As distressing as that official number is, America’s true fiscal situation is even worse — far worse. According to a barely-publicized Treasury report, the actual grand total of Uncle Sam’s obligations is more than $151 trillion.

That huge discrepancy springs from the fact that the federal government doesn’t hold itself to the same accounting standards it imposes on businesses. Rather than using accrual accounting — which recognizes expenses when they’re incurred — our Washington overlords self-servingly use simple cash accounting, only recognizing expenses when they’re paid. As a result, discourse on federal obligations solely focuses on the national debt, comprising Treasury bills, notes and bonds.

Once a year, however, an obscure report delivers a more accurate version of Uncle Sam’s balance sheet. While it receives almost no attention from journalists or public officials, the Treasury Department is required to submit an annual report to Congress detailing the government’s financial condition. Critically, the 1994 law compelling this report mandates that it reflect “unfunded liabilities” — that is, commitments made without any dedicated assets or income streams to ensure they’ll be kept.

…..

One of the larger categories of those unfunded liabilities is future federal employee and veterans benefits. At the end of the 2024 fiscal year, this alone represented a $15 trillion obligation. However, by leaps and bounds, the largest unfunded liabilities spring from America’s social insurance obligations — primarily Social Security and Medicare. At fiscal-year end, these liabilities totaled a towering $105.8 trillion.

Stacking these and other unfunded liabilities on top of the publicly-held national debt and other obligations, you arrive at a grand total of $151.3 trillion at the end of the 2024 fiscal year. Offsetting that by an estimated $7.9 trillion in US government commercial assets — including property, plant, equipment and purported gold holdings — a Just Facts analysis puts Uncle Sam at an overall net-negative $143 trillion.

……………..

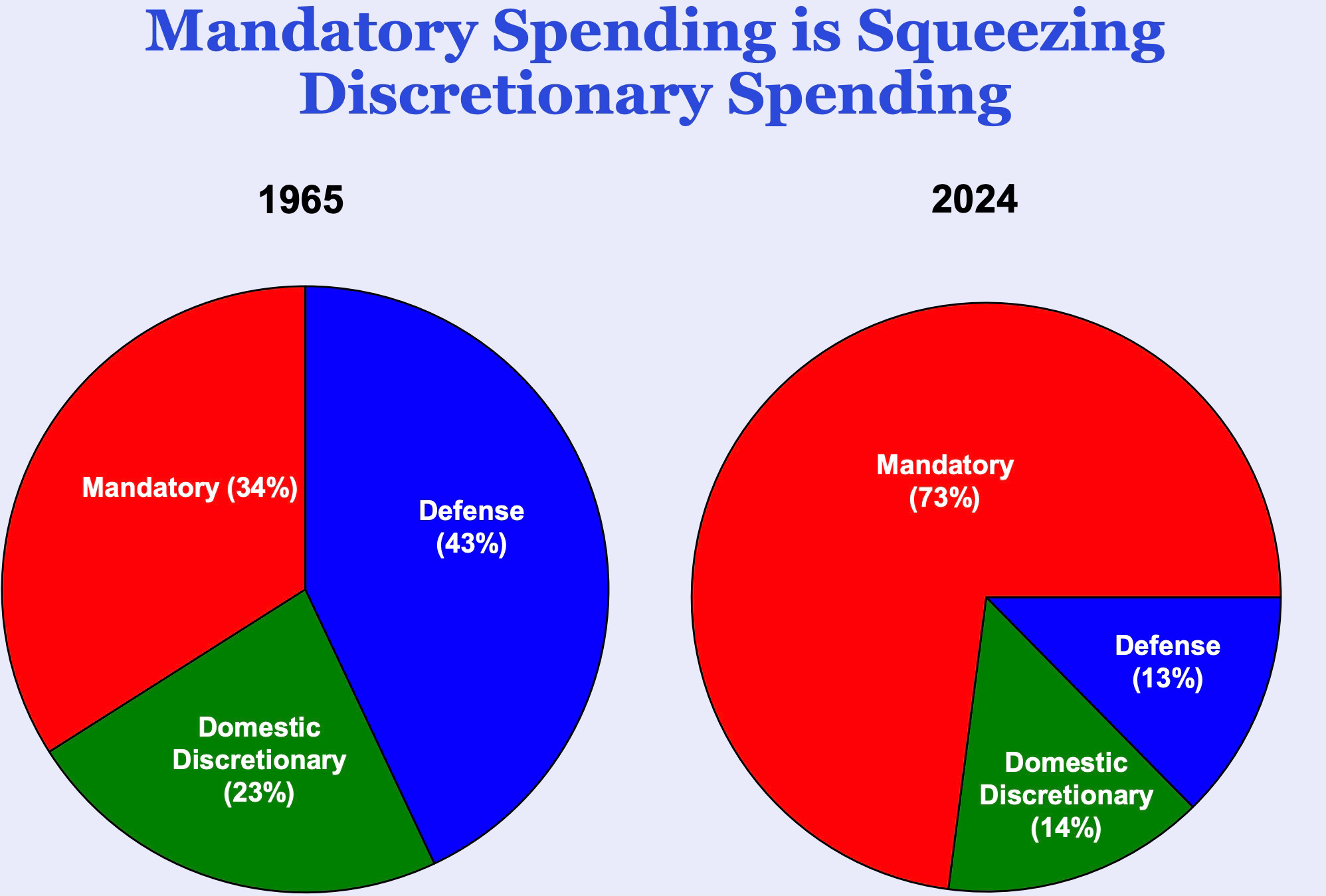

Wrangling over the budget isn’t going to save us. Congressional debates tend to center on discretionary spending — outlays that require a vote by Congress during the appropriations process. However, America’s steady march to insolvency is driven by so-called mandatory spending, which is hardwired by previously-enacted laws.

In what may be the most ominous indication that the government is on an autopilot-course for catastrophe, the proportion of total federal outlays driven by mandatory spending has more than doubled since 1965 — from 34% to 73% in 2024. It was at 71% just two years earlier, in 2022.

The two largest examples of mandatory spending are Social Security and Medicare. Those old-age programs are now well within sight of a crisis that’s been warned about for a generation: According to the latest report from their program trustees, Social Security and Medicare trust funds are now just seven years from insolvency.

……….

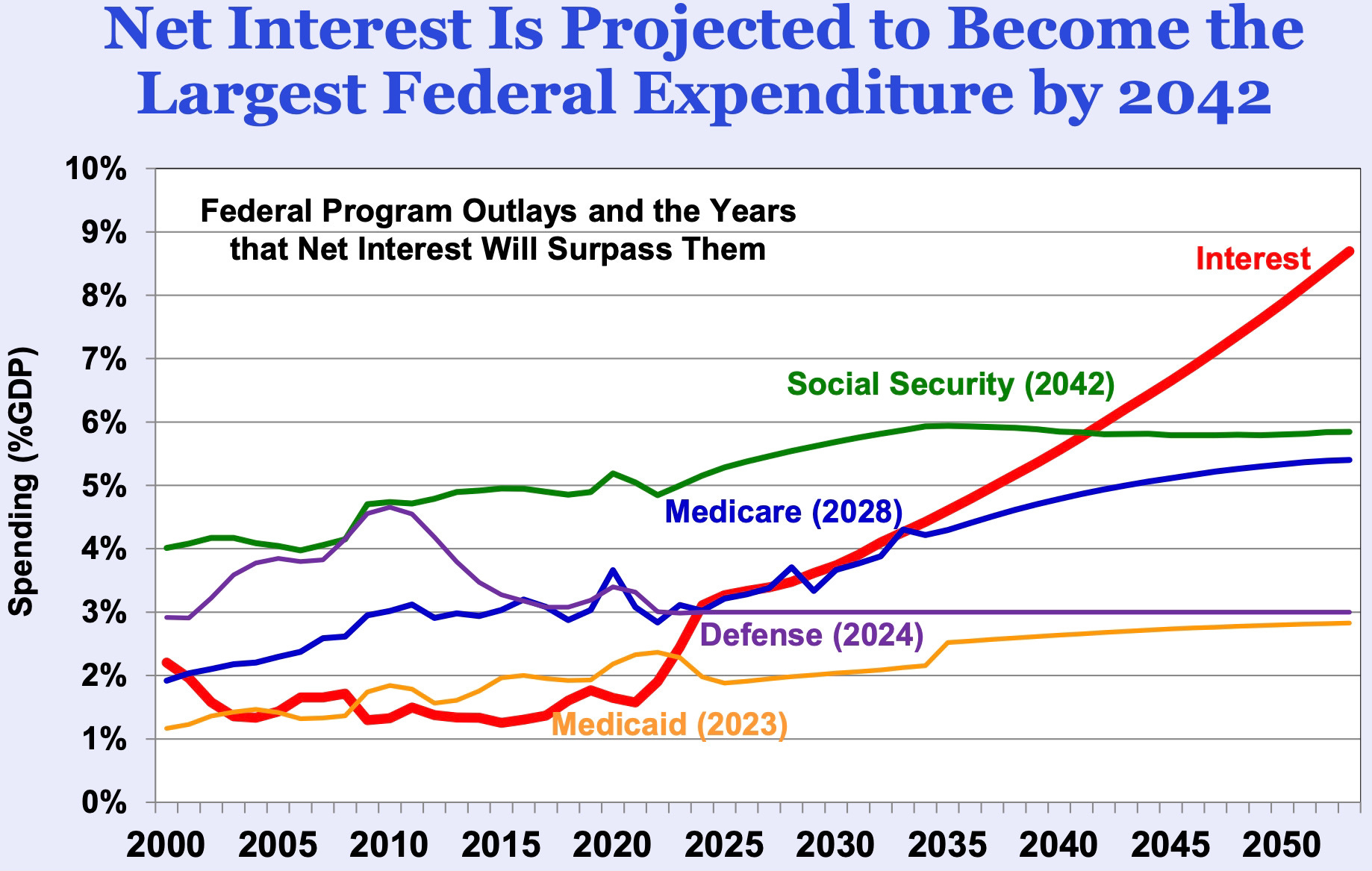

There’s another key component of mandatory spending that isn’t counted in the national debt: interest payments on debt issued to cover past and current spending. “In total, social programs and interest on the national debt—which mainly stems from social programs—account for 75% of all federal spending,” notes Agresti.

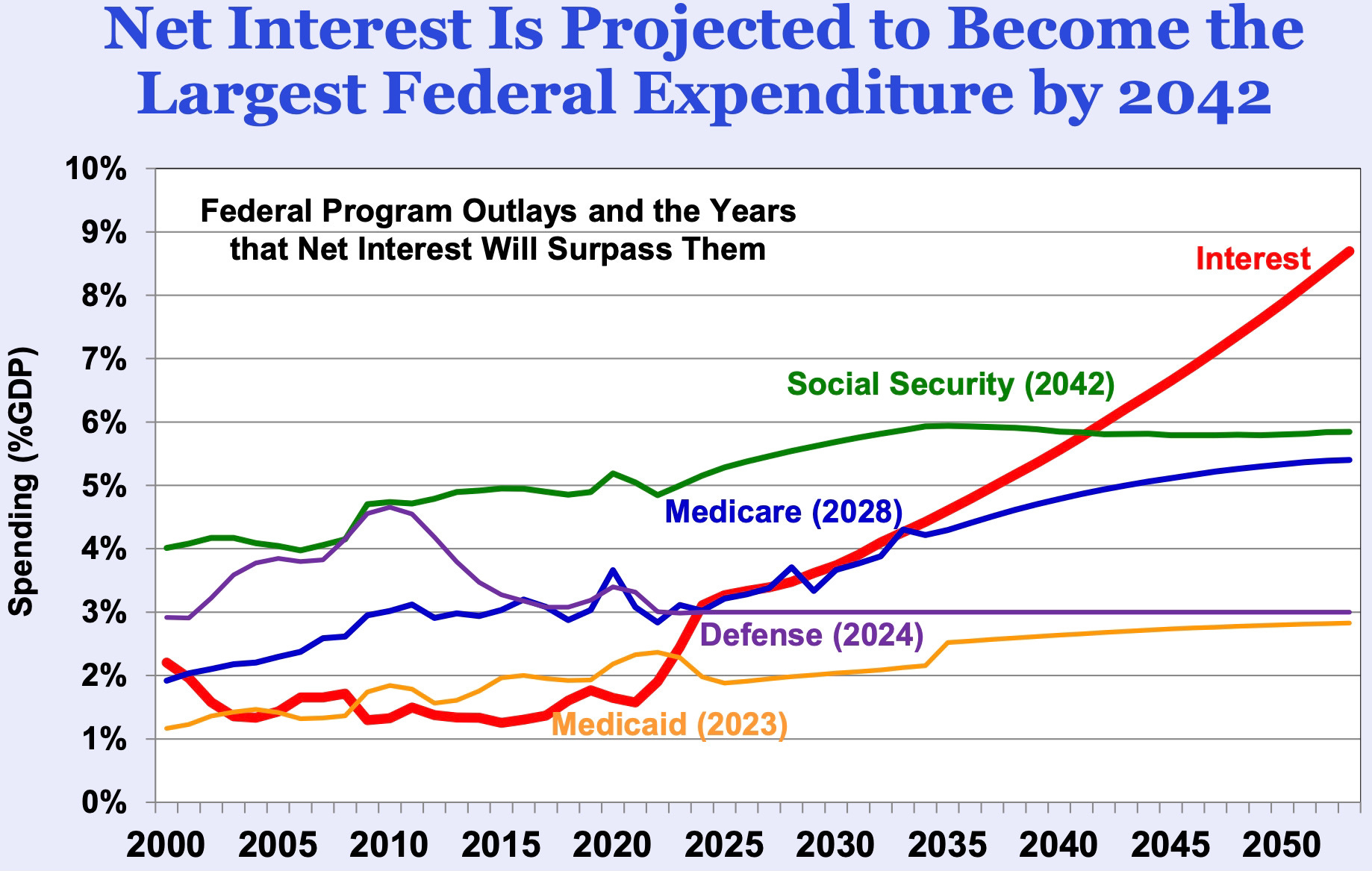

Interest payments also represent a steadily growing share of total outlays, and will total almost $1 trillion this year. Within 10 years, they’re projected to reach $2 trillion, roughly equal to the entire 2025 deficit. Last year saw a grim milestone, as interest expense surpassed spending on both defense and Medicare.

Current projections have interest surpassing Social Security to become the largest single expenditure by 2042, but don’t be surprised if that milestone doesn’t come sooner. The government is already descending into a vicious cycle in which mounting US debt has the buyers of that debt demanding higher interest rates in compensation for the growing risk of inflation and/or default — with those higher rates creating larger interest payouts and even more debt.

Beyond mandatory-vs-discretionary, and funded-vs-unfunded, there’s an even more important but far-less-discussed classification of spending that goes to the very heart of America’s march toward financial disaster: constitutional vs unconstitutional. As I noted in the most-read article at Stark Realities, “Americans Are Fighting For Control Of Federal Powers That Shouldn’t Exist”:

Today’s sprawling federal government, which involves itself in almost every aspect of daily American life, is almost entirely unconstitutional.

To rattle off just a random fistful of the federal government’s unauthorized undertakings and entities — brace yourself — there is zero constitutional authority for the Social Security, Medicare, federal drug prohibitions, the Small Business Administration, crop subsidies, the Department of Labor, automotive fuel efficiency standards, climate regulations, the Federal Reserve, union regulation, housing subsidies, the Department of Agriculture, workplace regulations, the Department of Education, federal student loans, the Food and Drug Administration, food stamps, unemployment insurance or light bulb regulations. Even that sampling doesn’t begin to fully account for the scope of the unsanctioned activity.

This Pandora’s box of unconstitutional endeavors was opened wide by unconscionably expansive Supreme Court interpretations of the Constitution in the 1930s. It’s no coincidence that federal spending represented a mere 3% of GDP in 1930 but soared to an economy-warping 23% by 2024.

Now we find the federal government in a $143 trillion hole, a burden that comes out to $1,085,022 per US household. History suggests this will end with a government default. In the United States, that will likely occur not via an explicit repudiation of the debt, but through rampant price inflation as the Treasury and the Federal Reserve conspire to create new money out of thin air to make debt payments.

“They can’t pay the debt, so they have to liquidate the debt,” said former Congressman Ron Paul in a June conversation with David Lin. “They [won’t] default — they’re always going to pay something for the Treasury bills. What they’re going to do is liquidate the debt by paying it off with counterfeit money.”

While the Fed-Treasury money creation scheme has been with us for a long time, the alarming trajectory of federal debt and spending point to future money-printing on a scale that will trigger hyperinflation and economic collapse. At that point, Americans will stand at a crossroads. Desperation and fear will make them susceptible to the siren song of even more authoritarianism and unconstitutional, centralized command of the economy and society than what put them in such dire straits to begin with.

“People will want to be taken care of,” Paul said. “I see it as an opportunity. If people are promoting the cause of liberty and there’s chaos in the streets, we better get out there and lead the charge and say you don’t need more of what caused this. You don’t need more authoritarianism. What you need is more liberty and more peace, and that means you ought to obey the Constitution.”

________________________________

Mr. Ron Paul, meet The Leviticus 25 Plan: 1) Preserve the cause of liberty and economic freedom for all Americans; 2) Restore financial security to millions of America’s hard-working, tax-paying U.S. citizen families; 3) Reverse big-government “centralized command of the economy and society”; 4) Eliminate massive amounts of entitlement program outlays; 5) Restore citizen-centered health care in America; 6) Generate $37.303 billion federal budget surpluses each of it first five years of activation (2027-2031); 7) Eliminate the looming threat of credit market disorder and banking system instability.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

U.S. Senate Committee on Homeland Security & Governmental Affairs – December 2025

Excerpts:

Executive Summary

On July 15th, 2025, Chairman Rand Paul of the U.S. Senate Committee on Homeland Security and Governmental Affairs (HSGAC) launched an investigation on the Federal Reserve’s use of Interest on Reserve Balances (IORB). After months of correspondence, the Federal Reserve Board of Governors produced over 40,000 pages of documents detailing IORB payments for every two-week period from July 2013 through July 2025.

July 2013 through July 2025. This report outlines the following key findings from the contents of the data:

IORB payments equal 10 percent of the Federal Deficit: a. The magnitude of IORB payments equaled 10.3 percent ($187 billion) of the FY24 Federal deficit and 8.8 percent ($149 billion) of the FY23 deficit.

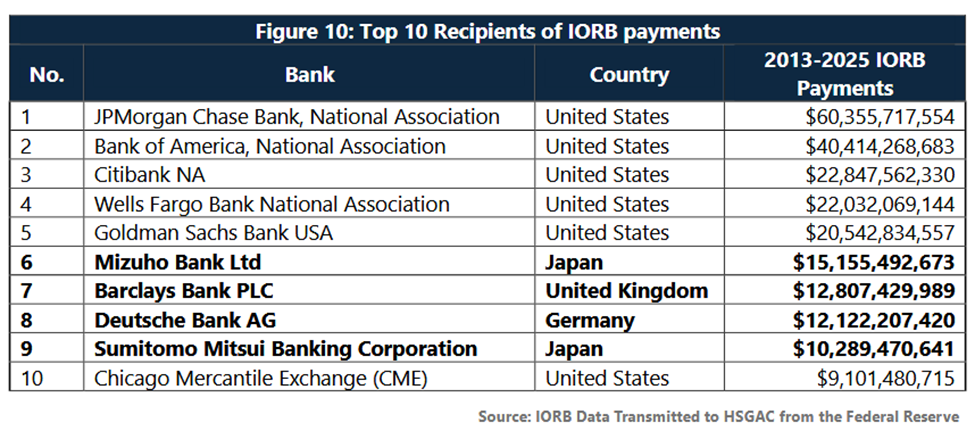

The Federal Reserve has used IORB payments to subsidize Wall Street’s largest banks: a. IORB payments account for 12 percent of all profits for the 5 largest American banks from 2013-2024. b. In 2024, IORB payments accounted for 16 percent of U.S. banking sector’s net interest income. c. The top 20 banks account for over half ($305 billion) of total payments with the remaining 4,500 banks accounting for the remaining half ($302 billion).

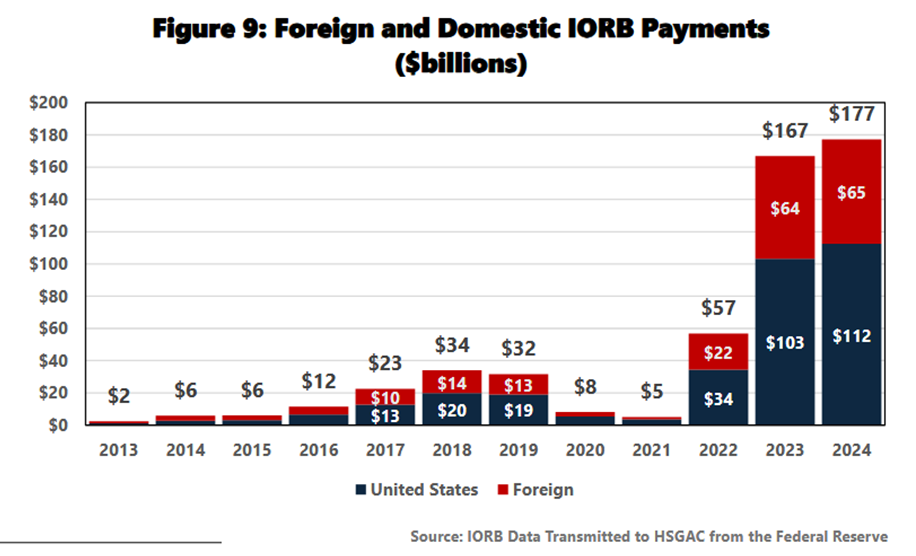

IORB payments are also subsidizing foreign banks: a. 11 of the top 20 recipients of IORB payments are foreign banks. b. From July 2013 – July 2025, $235 billion has been paid to foreign banks by the Fed through IORB payments (see figure 9). c. $10 billion of these payments were made to Chinese banks such as Bank of China, China Construction Bank, Industrial and Commercial Bank of China, and Bank of Communication…..

…………

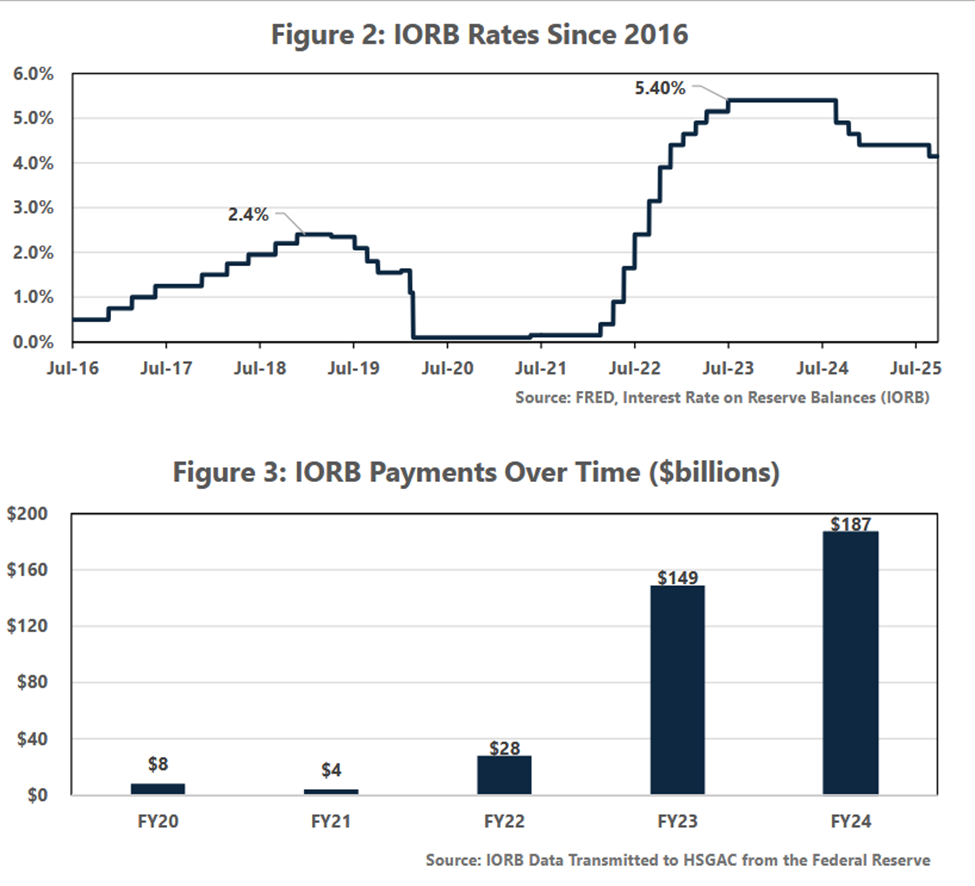

IORB Rates Rise

Prior to 2021, IORB rates peaked at 2.4 percent, however in the inflationary period after the COVID stimulus in 2021, the Fed began to raise rates in an attempt to rein in inflation. The Fed raised IORB rates to a high of 5.4 percent in July 2023 (see figure 2).

The Fed’s increased IORB rates incentivized eligible domestic and foreign banks to place reserves at the Fed instead of lending out these funds, buying treasury bills, or other financial activities effectively setting a floor on interest rates. IORB payments from the fed ballooned from an average of $17 billion prior to the pandemic to over $100 billion in each of the last two fiscal years (See figure 3).

IORB Payments as Corporate Welfare

Introduction – IORB payments, as currently structured, take the Fed’s operating profits that could be used to pay down the deficit and pay these funds out to the world’s largest banks. Since 2013, the Fed has paid $607 billion in identified payments to both foreign and domestic financial institutions to keep their reserves idle and interest rates artificially high. This costly means of conducting monetary policy has prevented the Fed from remitting profits to Treasury to pay down the Federal deficit and instead directed these funds into Wall Street’s profit margins.

Characteristics of IORB Payment Recipients

Analysis of these payments shows that large banks are the primary beneficiary of this reallocation of taxpayer funds. The allocation of IORB payments is disproportionately skewed to large financial institutions. The top 20 bank recipients (see Figure 6) received approximately the same amount of IORB payments from 2020-2025 ($305 billion) as the next 4,500 banks received ($302 billion).

IORB Payments as a Driver of Bank Profits

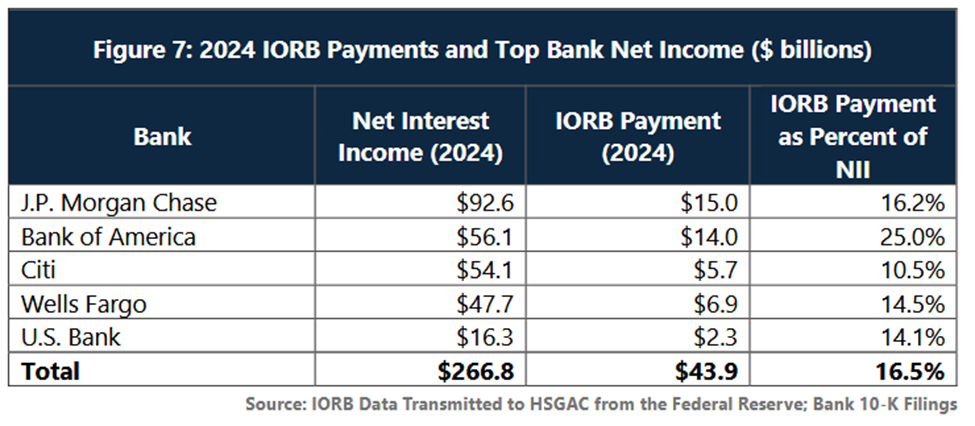

The five largest banks in the U.S. by consolidated assets: JP Morgan Chase, Bank of America, Citibank, Wells Fargo, and U.S. Bank received $136 billion in IORB payments from 2013 to 2024, with 2024 payments alone amounting to $43.9 billion. In 2024, taxpayer-financed IORB payments were a considerable driver for profitability for these banks accounting for 16.5 percent of net interest income for the U.S.’s 5 largest banks in 2024. Looking at the entirety of the banking sector, IORB payments accounted for 16.1 percent of all net interest income of U.S. banks in 2024.

……….

Share of Foreign and Domestic Payments

While the proportion of IORB payments to foreign banks has decreased slightly since 2013, the gross amount in payments sent to foreign banks continues to grow substantially each year as the Fed has increased IORB rates. In 2019, prior to the pandemic, $13 billion in IORB payments were paid to foreign banks. Since 2022, however, the Fed has paid an average of $50 billion in IORB payments to foreign institutions and this number continues to grow.

As IORB rates drastically increased in late 2021 and 2022, not only did domestic banks rush to park capital at the Fed, but foreign banks also seemed to inject dormant capital from their international banks into their U.S. subsidiary to take advantage of the more generous risk-free interest offered for excess reserves. The share of IORB payments jumped from 28.5 percent foreign banks (the lowest since 2013) to nearly 40 percent of payments….

Many of the world’s largest banks have been the largest beneficiaries of IORB payments. Of top 10 recipients of IORB payments from July 2013 to July 2025, 4 are foreign banks (bolded), and 11 of the top 20 are foreign banks…:

IORB Payments as a Foreign Bank Subsidy

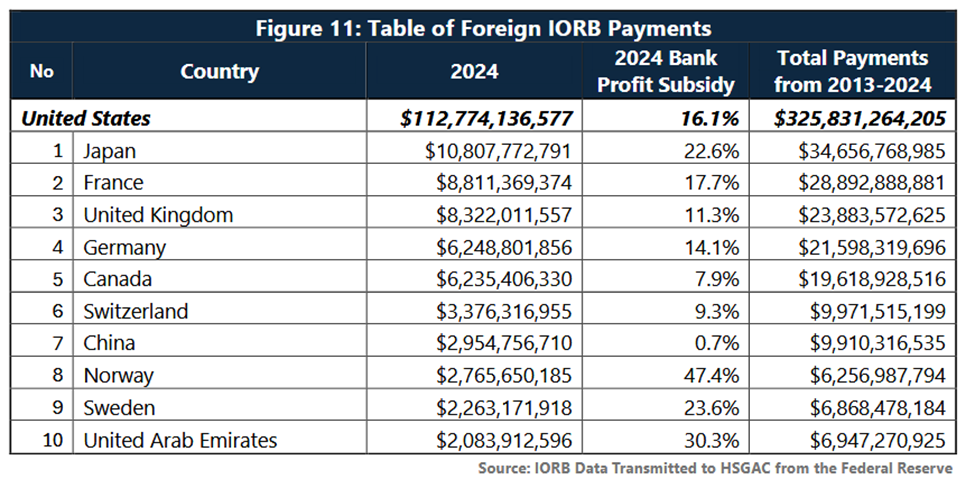

In 2024, while 16.1 percent of the U.S.’s banking sector’s net interest income comes at the expense of the taxpayer through IORB, 5 percent of all the participating foreign banks net interest income comes from the U.S. taxpayer. Figure 11 shows the top 10 benefitting nations and the percentage of bank profits is subsidized by the U.S. taxpayer.

“Bank profit subsidy” reflects the percent of participating depository institution’s net interest income that is attributable to IORB payments from the Fed. Notably,

the American taxpayer has financed over 50 percent of Bahrain’s bank profits, 47 percent of Norway’s bank profits, and 22 percent of Japan’s bank profits…

Conclusion: Hundreds of billions of dollars for the taxpayer have been sent to foreign banks, hundreds of billions of dollars for the taxpayer have padded Wall Street’s profit margin, all without a single election, public debate, or independent audit. This is the first step in what should be a continued effort to audit the Federal Reserve.

Again: “This costly means of conducting monetary policy has prevented the Fed from remitting profits to Treasury to pay down the Federal deficit and instead directed these funds into Wall Street’s profit margins.”

Federal budget deficits are skyrocketing as major Wall Street and foreign banks are being subsidized with hundreds of billions of dollars in Fed IORB payments.

Main Street America is paying a steep price for this ongoing kleptocratic snow job. The country is wallowing in debt… while the Fed is doling out hundreds of billions of dollars to pump up the profit margins of Wall Street’s largest banks and major foreign banks.

Main Street America Republicans have the plan to re-target Fed liquidity flows to pass through the hands of tax-paying U.S. citizens first, and then into the banking system (through Household debt service / elimination), and into America’s small business sector, and into savings and investing vehicles.

The Leviticus 25 Plan will generate federal budget surpluses of $37.303 billion each of its first five years of activation (2027-2031) and pay for itself entirely over the succeeding 10-15 years.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Swirling winds are again picking up in the Washington budget battle. Main Street America Republicans hold the winning hand with a dynamic, debt-busting powerhouse economic plan to solve America’s ongoing budget crisis – and win the hearts and votes of millions of America’s hard-working, tax-paying U.S. citizens.

The House is set to vote Thursday on bipartisan legislation to fund several federal agencies and programs as lawmakers work to avert the threat of another government shutdown later this month.

The vote, set for Thursday afternoon, comes after House and Senate negotiators released the text of the three-bill package, known as a “minibus,” on Monday. The package includes funding through September for science initiatives and the Departments of Commerce and Justice; energy and water development; and the Department of Interior and the EPA.

Congress has until Jan. 30 to fund major parts of the government, after lawmakers approved a short-term funding measure to end the longest government shutdown in history in November. At the time, lawmakers passed a three-bill package that funded part of the government through September, while extending funding for the remaining nine appropriations bills on a temporary basis.

But the remaining funding effort has not been without hurdles, and the latest funding package will be split in two after a conservative rebellion threatened to stall the legislation.

Nine House Republicans joined with House Democrats Wednesday evening to advance a vote on a Democratic healthcare bill that extends Obamacare subsidies that expired at the end of last year.

The vote is considered a major setback for Speaker Mike Johnson, R-La., who has been arguing that a majority of House Republicans opposed extending the subsidies, according to Fox News.

The vote on Wednesday was to advance House Minority Leader Hakeem Jeffries discharge petition, a mechanism for moving legislation to the floor of the House even if the leadership of the majority party opposes it.

The four who had signed onto the discharge petition were Mike Lawler, R-N.Y.; Brian Fitzpatrick, R-Pa.; Rob Bresnahan, R-Pa.; and Ryan Mackenzie, R-Pa. The other five who joined with them to move the legislation to the floor are Reps. Nick LaLota, R-N.Y.; Maria Salazar, R-Fla., David Valadao, R-Calif., Max Miller, R-Ohio, and Tom Kean Jr., R-N.J.

While the bill is now certain to pass in the House on Thursday, it is considered almost certain to fail in the Republican-controlled Senate.

The Treasury Department is implementing President Donald Trump’s No Tax on Car Loan Interest policy, a measure designed to lower costs for American families, Treasury Secretary Scott Bessent said Wednesday.

The policy, enacted as part of Trump’s “big, beautiful bill,” allows eligible taxpayers to deduct up to $10,000 a year in car loan interest on new, U.S.-assembled vehicles purchased between 2025 and 2028.

“Treasury is implementing President Trump’s No Tax on American Car Loan Interest, putting money back in the pockets of working and middle-class families,” Bessent wrote on X.

____________________________________

The Leviticus 25 Plan is loaded up and ready to launch.

This Main Street America Republican powerhouse economic plan will: • Generate a $37.303 billion budget surpluse each of its first five years of activation (2027-2031). • Overwhelmingly reduce dependence on government-based entitlement programs. • Restore citizen-centered, consumer-driven health care. • Cleanly and efficiently eliminate massive amounts of private sector debt (mortgage debt, consumer debt, student loan debt, auto loan debt). • Revitalize real long-term economic growth and prosperity in the U.S..

Those Americans who wish to keep their ObamaCare subsidies may keep them. All other qualifying U.S. citizens, across all income levels, who wish to participate in The Leviticus 25 plan will enjoy health care access and benefits which far exceed the quality and access extended under ObamaCare plans.

Note – If Washington Republicans would hold up this plan and say, “We need to move in this direction,” the budget battle would be over in a matter of seconds. And they would win over the hearts and minds, and votes, of the vast majority of working-class Americans (white, black, Hispanic, Asian, Native American, Middle Eastern) for years to come.

They would de-stress the entire U.S. economic system and get America back on track.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

{kind=link}

{kind=link}

{kind=link}

{kind=link}