Four key points:

1. The global financial system is careening toward a centralized digital currency system. It is beginning now with the world’s major central banks (U.S. Federal Reserve, European Central Bank, Bank of England, Bank of Japan, Bank of Canada, Swiss National Bank, along with individual countries, developing/implementing digital currencies.

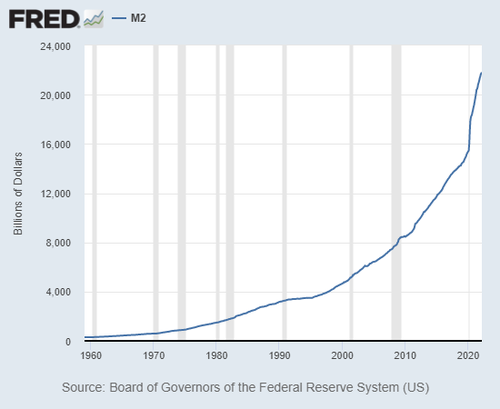

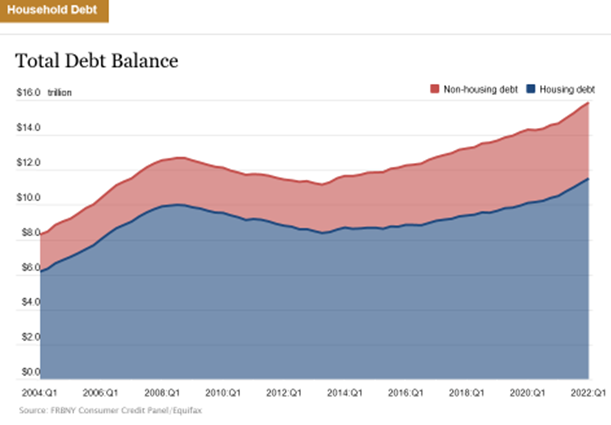

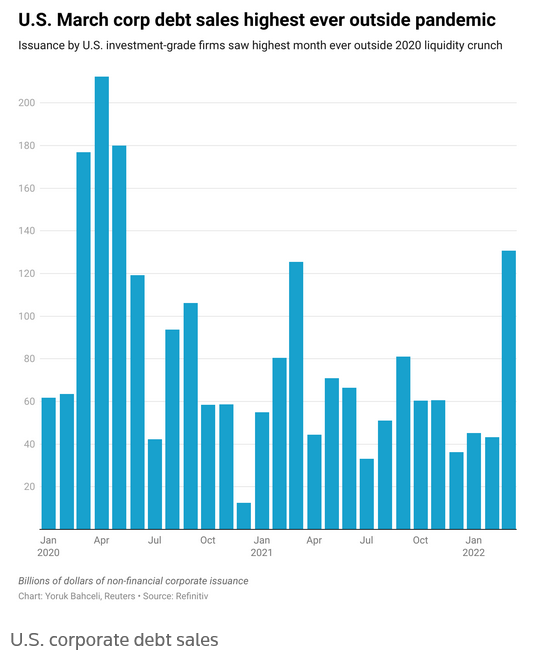

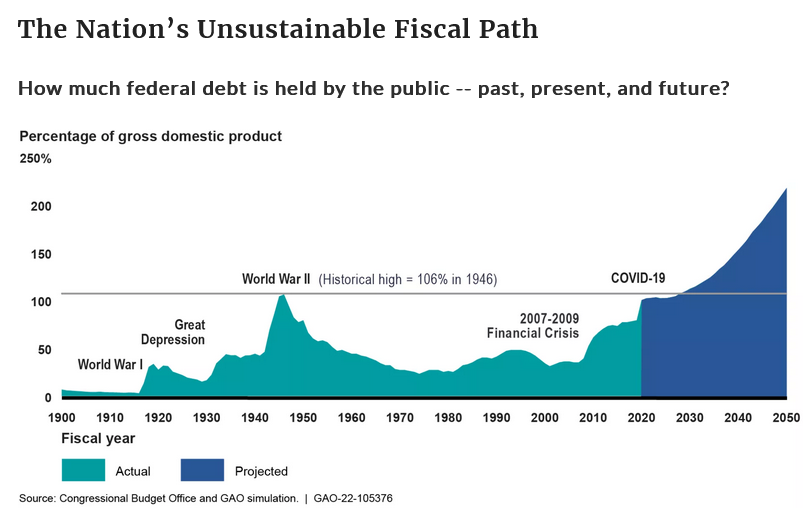

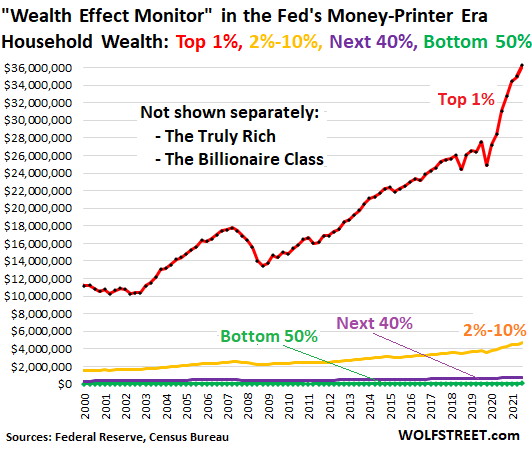

2. The enormous debt loads amassed by the U.S., Europe, Japan, China will inevitably lead into periods of paper (fiat) currency instability and potentially credit market disorder. America’s national debt is listed today as $20.348 trillion (125.6% debt to GDP ratio). The true debt, also known as the fiscal gap, or the net present value of unfunded liabilities (NPV), is believed to be over $180 trillion.

The Federal Reserve, for one, will then have an open door to ‘rescue’ the U.S. financial system by offering citizens a conversion opportunity – out of paper Dollars, and into a new Federal Reserve-based digital currency (possibly termed, ‘Stable Coin’).

These initial Central Bank implementations will eventually be followed by a natural and unavoidable migration onto a global platform as a necessary standard for engaging in international trade.

3. Anyone who believes that President Biden is the author/originator of this Executive Order (EO) below is giving him far too much credit. There is clearly a globalist-minded cabal, behind the scenes, pulling all the levers and pushing all of the right buttons to coordinate the flow of these events.

4. There is nobody in the U.S. Congress offering forth a legitimate plan to deleverage America’s enormous debt load – which would have the tremendously beneficial effect of stabilizing the U.S. Dollar, recharging the U.S.economy, and providing a qualitatively new measure of financial security for millions of American families.

The Leviticus 25 Plan, the most powerful economic acceleration plan on the face of the earth, will deleverage America – and preserve our liberties.

……………………………………………

Fox Business: Biden’s proposal for a new digital currency is an attack on liberty

A central bank digital currency would put even greater authority in the hands

By Justin Haskins FOXBusiness, March 26, 2022 – Excerpts:

While the world remains focused on the tragic situation in Ukraine, the Biden administration is preparing to launch America’s first government-backed digital currency. If a new digital dollar is rolled out, it could substantially reduce individual rights and give the Federal Reserve and the national government significantly more power over the U.S. economy.

On March 9, the White House released an executive order covering digital assets, including cryptocurrencies like Bitcoin. Under the far-reaching executive order, a long list of government agencies would develop plans for regulating, studying, and/or monitoring cryptocurrencies and the various exchanges where consumers buy, sell, and trade them.

The White House’s intrusion in the use of blockchain technology should be enough to worry advocates of free markets, but there’s an even more troubling part of Biden’s executive order: the potential development of an entirely new, digital currency.

The EO states the White House has placed “the highest urgency on research and development efforts into the potential design and deployment options” of a novel central bank digital currency (CBDC).

It further instructs numerous federal departments, including the Treasury Department, to work on the development of a “report on the future of money and payment systems, including the conditions that drive broad adoption of digital assets.”

The Treasury Department must submit the report within 180 days, about six months.

The White House is also asking the chairman of the Federal Reserve to “develop a strategic plan for Federal Reserve and broader United States Government action, as appropriate, that evaluates the necessary steps and requirements for the potential implementation and launch of a United States CBDC.” And within 210 days of the executive order, a CBDC “legislative proposal” must be presented to the president.

This is a truly remarkable and deeply troubling development. If a CBDC were to be created, it would dramatically expand the power and influence of the federal government and Federal Reserve, in ways most Americans won’t understand until it’s too late to roll the CBDC back.

Unlike blockchain-based digital currencies such as Bitcoin, which are by design decentralized, a central bank digital currency would likely be programmable, meaning that it could be designed so that Americans could only use it for specific purposes. And it would be easy for banks and government agencies to track digital dollars and the people using them, unlike printed U.S. dollars available today.

Although some might be tempted to dismiss these fears as too far-fetched to be of serious concern for a country like the United States, there is strong evidence that the White House and Federal Reserve have already considered making a new digital dollar programmable, in line with their various social and economic goals

For instance, Biden’s executive order states that a CBDC should be designed to advance “financial inclusion and equity” and with “climate change and pollution” in mind.

A “fact sheet” released by the White House about the executive order also stated that its EO will “Promote Equitable Access to Safe and Affordable Financial Services” and that the government’s report about the development of a digital dollar must “include implications for economic growth” and “financial growth and inclusion.”

A senior administrative official also told reporters that the White House has and will continue to “partner with all stakeholders — including industry, labor, consumer, and environmental groups, international allies and partners” when developing plans for a central bank digital currency.

Why would unions, environmental groups, and business lobbyists be involved in the creation of a new currency, unless that currency is programmable?

A central bank digital currency could also transform America’s monetary system in important ways. Rather than use interest rates and complex monetary tools to help improve employment rates and keep inflation at target levels, a central bank digital currency could be created at will, with nothing more than a push of a button, and possibly even distributed directly to Americans—giving the Fed more control over the economy than ever before.

Perhaps most disconcerting of all is that a programmable central bank digital currency could be altered at any point in the future, giving it the potential to be politicized or to be subject to even greater restrictions.

The United States has become the world’s most successful society by empowering individuals and businesses, especially small businesses. A central bank digital currency would do just the opposite, putting even greater authority in the hands of a small number of banks, government officials, and bureaucrats. Biden’s plan for a central bank digital currency must be stopped.

Justin Haskins is the director of the Stopping Socialism Center at The Heartland Institute and the co-author, with Glenn Beck, of the forthcoming book, “The Great Reset: Joe Biden and the Rise of 21st Century Fascism.”

_______________________________

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2023 (4004 downloads)