The U.S. Health Care Freedom Plan is a dynamic health care initiative with the power to restore citizen-centered health care for America.

The U.S. Health Care Freedom Plan grants a substantial initial deposit, $25,000 per family member, into a participating family’s Medical Savings Account (MSA). This robustly-funded MSA would make it possible for families to pay cash for their day-to-day, primary care healthcare needs over the course of the initial 5-year plan period.

Cash payments for day-to-day health care needs would give patients the freedom of choice in choosing their providers, taking greater ownership in their healthcare decisions, and avoiding unnecessary red tape and delays in treatment. It would avoid penalties families might otherwise pay — for not doing things, precisely, according to government mandates.

The U.S. Health Care Freedom Plan would eliminate massive amounts of administrative costs and bureaucratic overhead. It would allow American families to tailor their spending according to their individual needs, rather than requiring costly coverage in areas that are irrelevant to their needs.

It would provide millions of Americans (those left “uncovered” by the current health law) with access to primary care – without expanding Medicaid.

Cash-paying customers would open the door for countless new efficiencies to be woven back into the system.

It would be a welcome development for nearly all providers. Instead of turning patients away, due to unacceptable reimbursement rates, they would find ways to appropriately accommodate patients in this newly energized system.

…………………………….

Our current big government program is a massive, inefficient, bureaucracy-driven quagmire…

Columnist Holoman Jenkins, Jr., WSJ 9-25-13:

“Our point is that when Washington legislates on a grand scale, it sets in motion a game whose long-run outcome nobody can predict.

ObamaCare, to be sure, was not reform—it was a piling on of subsidies that can only throw fuel on the fire of health-care inflation. Not even the usual mouthpieces pretend otherwise anymore.

But a society can’t give a subsidy to everybody for the same reason you can’t give a subsidy to yourself—you end up paying for your own subsidy and aren’t better off. In fact, you are worse off thanks to the administrative overhead involved in taking money away from you and giving it back to you.

You are also worse off because of the perverse incentives engendered by diverting yours and everyone’s health-care spending through a common pot.

These pathologies have undermined U.S. health care for two generations, and nothing has been solved, nothing has been fixed…”

______________________________________

The U.S. Health Care Freedom Plan

It is time for a new strategy – that puts citizens back in charge of their health care resources and decision-making..

_________________________________

The U.S. Health Care Freedom Plan is the only comprehensive, citizen-centered health care plan in America. It ‘resets’ the health care industry to present a clean, efficient and responsible system. Most importantly, this plan restores individual freedom and liberty for all participating Americans.

The Plan:

- The U.S. Health Care Freedom Plan is available to each and every U.S. citizen – with no coverage mandates. Each U.S. citizen who wishes to participate will be granted a full and complete exemption from the ACA.

- This plan offers freedom of choice and equal justice for all. Those Americans who might wish to stay with the ACA may stay (‘If you like your ObamaCare, you can keep your ObamaCare’).

- Each participating U.S. citizen shall receive a credit extension, through a special Federal Reserve Citizens Credit Facility, of $25,000, electronically deposited into a Medical Savings Account (MSA) – for direct allocation toward family health care needs.

- Private insurance – Families shall be allowed to enroll in high-deductible ($10,000 – $15,000) major medical plans, to include basic, ‘no frills’ medical plans which best suit their individual needs and desires. These streamlined plans would lower premium costs for employees and employers, encouraging employers to cost-share savings with employees through incentive-based employer MSA contributions.

- Policies would not be automatically loaded with expensive government healthcare mandates.

- Those with extraordinary medical issues may be included in a high-risk category, with such plans being eligible for a government subsidy (similar to current Medicare Advantage).

- Federal / state programs – Individuals enrolled in Medicare / Medicaid / VA / TRICARE / FEHB programs would maintain their covered status, with an annual deductible of $5,000 per year per enrolled family member, for a period of five years for those benefits. The dedicated MSA funds would fully fund the offset for the higher ($5,000) deductible feature for that five-year period. MSA funds could also be used to pay Medicare supplement premiums and other potential co-pay obligations.

- Where health care services paid by patients directly with MSA funds, providers would not be bound by federal / state rules pertaining to Electronic Medical Records (EMRs), and other unnecessary administrative burdens.

Benefits:

Lower health care costs – With the elimination of millions of minor insurance claims across the nation over the course of each month, system-wide efficiency would improve, medical costs would drop significantly, and the direct patient-provider relationship would be restored. Medical professionals would not have to answer to HMOs, insurance companies, or government agencies in providing basic day-to-day healthcare access for their patients.

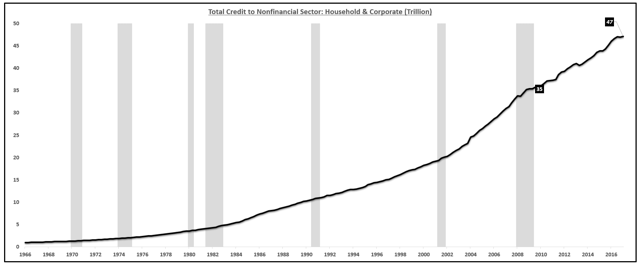

Scoring – if 300 million U.S. citizens were to participate in the plan, the total dollar transfer into family-based Medical Savings Accounts (MSAs) would amount to $7.5 trillion.

The potential cost savings from the $5,000 deductible provision for the approximate 150 million people currently enrolled in Medicare (55 million), Medicaid (72 million), VA (6.16 million), TRICARE (9.5 million), and FEHB (8.2 million) would amount to just under $3.75 trillion over the first 5 years (or, one-half the $7.5 trillion initial roll out cost).

Summary:

This plan would generate trillions of dollars in cost savings from streamlining, vastly improved efficiency, and reductions in waste and fraud.

This plan would improve quality and ease of access to health care for all participating Americans.

For patients: It would dramatically lower the cost of health care, while improving quality and access for all who chose to participate.

For providers: It would restore the patient-provider relationship and significantly reduce massive cost and time burdens imposed by a centralized system.

The U.S. Health Care Freedom Plan an integral part of a larger, comprehensive economic plan:

The Leviticus 25 Plan 2018 – $75,000 per U.S. citizen

The Leviticus 25 Plan 2018 (2570)

___________________________________

Notes:

Exemptions: ObamaCare currently offers hardship exemptions for individuals who have a recognizable inability to pay for a plan or pay the penalty. The ACA also currently offers exemptions from certain provisions within the health care law, such as the reinsurance provisions, for various union organizations.

And certain U.S. Territories are exempt from specific ACA measures: The Hill, 7-17-14: “Insurance companies in Puerto Rico, Guam, American Samoa, the U.S. Virgin Islands and the Northern Mariana Islands are no longer required to implement a number of ObamaCare measures such as the community rating system, a single-risk pool, the medical loss ratio or guaranteed benefits.”

Administrative costs – bureaucracy:

The Federal government has spent hundreds of billions of dollars to construct the monstrous ACA ‘machine.’

Billions of dollars have been spent on the roll out costs, insurer subsidies, management, monitoring, advertising, technical ‘fixes,’

There will be hundreds of billions of dollars yet to come with legal costs/prosecution, audits, regulatory costs/burdens, and much, much more.