U.S. Senate Committee on Homeland Security & Governmental Affairs – December 2025

Excerpts:

Executive Summary

On July 15th, 2025, Chairman Rand Paul of the U.S. Senate Committee on Homeland Security and Governmental Affairs (HSGAC) launched an investigation on the Federal Reserve’s use of Interest on Reserve Balances (IORB). After months of correspondence, the Federal Reserve Board of Governors produced over 40,000 pages of documents detailing IORB payments for every two-week period from July 2013 through July 2025.

July 2013 through July 2025. This report outlines the following key findings from the contents of the data:

- IORB payments equal 10 percent of the Federal Deficit:

a. The magnitude of IORB payments equaled 10.3 percent ($187 billion) of the

FY24 Federal deficit and 8.8 percent ($149 billion) of the FY23 deficit. - The Federal Reserve has used IORB payments to subsidize Wall Street’s largest banks:

a. IORB payments account for 12 percent of all profits for the 5 largest American

banks from 2013-2024.

b. In 2024, IORB payments accounted for 16 percent of U.S. banking sector’s

net interest income.

c. The top 20 banks account for over half ($305 billion) of total payments with

the remaining 4,500 banks accounting for the remaining half ($302 billion). - IORB payments are also subsidizing foreign banks:

a. 11 of the top 20 recipients of IORB payments are foreign banks.

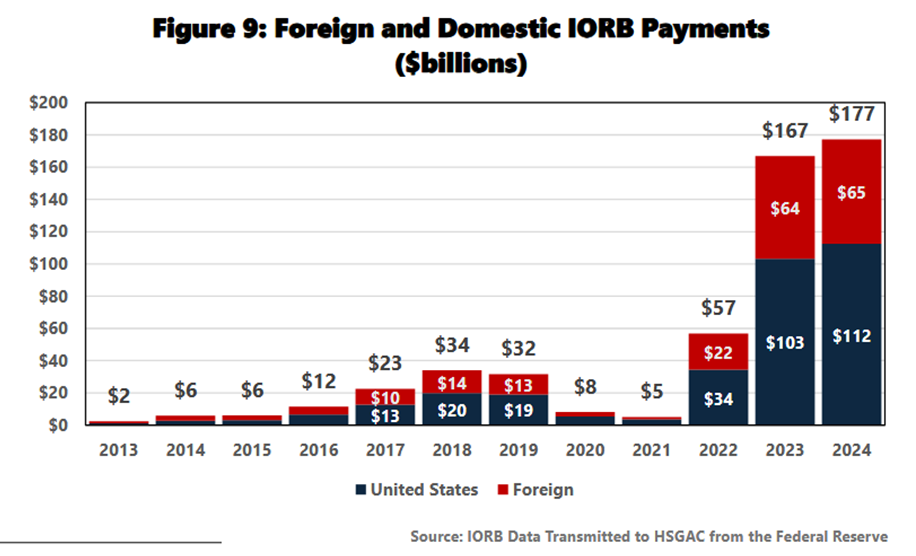

b. From July 2013 – July 2025, $235 billion has been paid to foreign banks by

the Fed through IORB payments (see figure 9).

c. $10 billion of these payments were made to Chinese banks such as Bank of

China, China Construction Bank, Industrial and Commercial Bank of China,

and Bank of Communication…..

…………

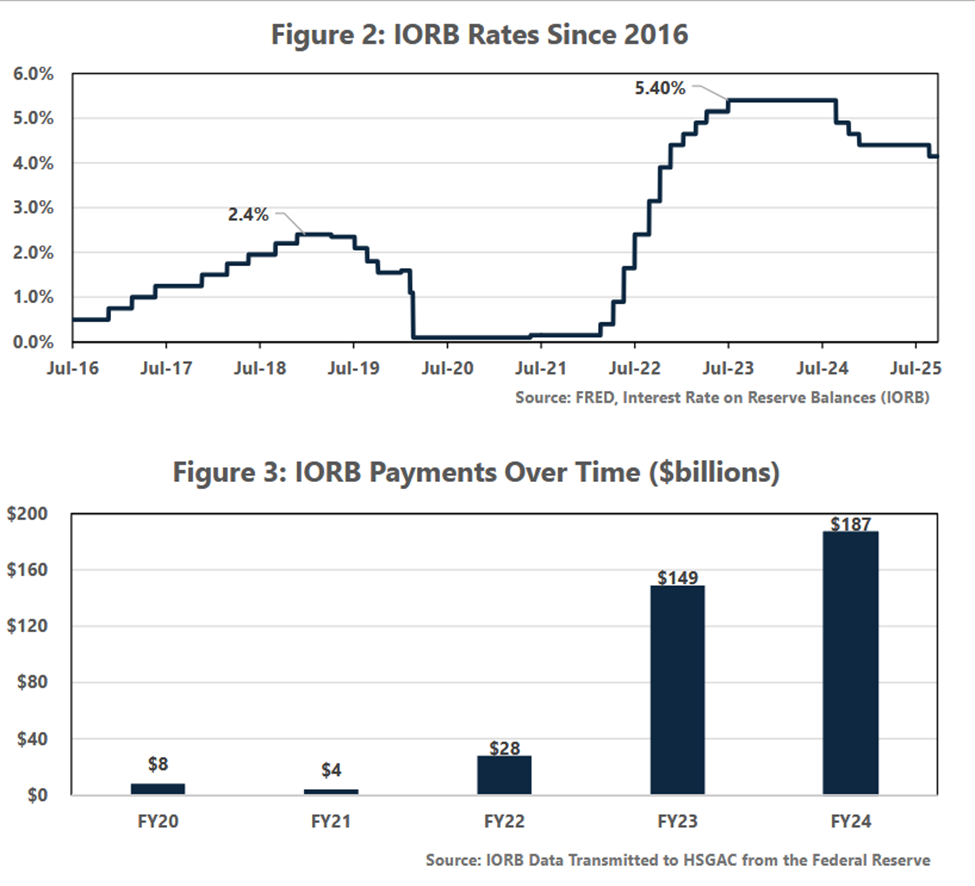

IORB Rates Rise

Prior to 2021, IORB rates peaked at 2.4 percent, however in the inflationary period after the COVID stimulus in 2021, the Fed began to raise rates in an attempt to rein in inflation. The Fed raised IORB rates to a high of 5.4 percent in July 2023 (see figure 2).

The Fed’s increased IORB rates incentivized eligible domestic and foreign banks to place reserves at the Fed instead of lending out these funds, buying treasury bills, or other financial activities effectively setting a floor on interest rates. IORB payments from the fed ballooned from an average of $17 billion prior to the pandemic to over $100 billion in each of the last two fiscal years (See figure 3).

IORB Payments as Corporate Welfare

Introduction – IORB payments, as currently structured, take the Fed’s operating profits that could be used to pay down the deficit and pay these funds out to the world’s largest banks. Since 2013, the Fed has paid $607 billion in identified payments to both foreign and domestic financial institutions to keep their reserves idle and interest rates artificially high. This costly means of conducting monetary policy has prevented the Fed from remitting profits to Treasury to pay down the Federal deficit and instead directed these funds into Wall Street’s profit margins.

Characteristics of IORB Payment Recipients

Analysis of these payments shows that large banks are the primary beneficiary of this reallocation of taxpayer funds. The allocation of IORB payments is disproportionately skewed to large financial institutions. The top 20 bank recipients (see Figure 6) received approximately the same amount of IORB payments from 2020-2025 ($305 billion) as the next 4,500 banks received ($302 billion).

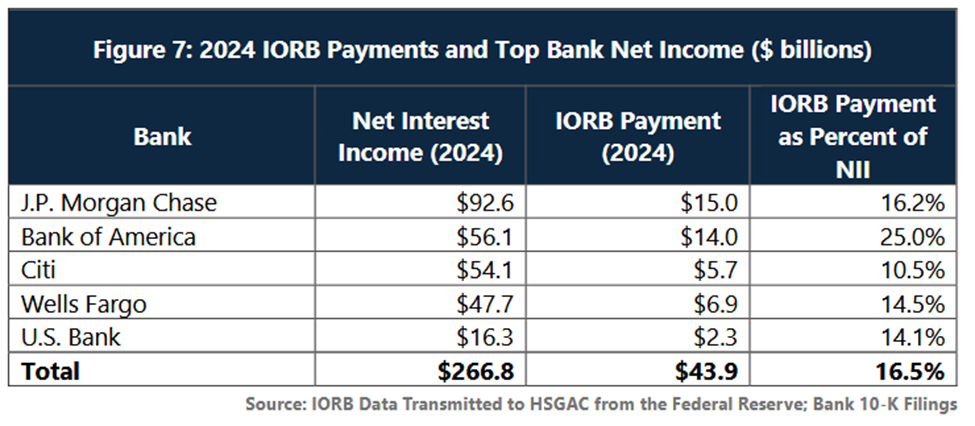

IORB Payments as a Driver of Bank Profits

The five largest banks in the U.S. by consolidated assets: JP Morgan Chase, Bank of America, Citibank, Wells Fargo, and U.S. Bank received $136 billion in IORB payments from 2013 to 2024, with 2024 payments alone amounting to $43.9 billion. In 2024, taxpayer-financed IORB payments were a considerable driver for profitability for these banks accounting for 16.5 percent of net interest income for the U.S.’s 5 largest banks in 2024. Looking at the entirety of the banking sector, IORB payments accounted for 16.1 percent of all net interest income of U.S. banks in 2024.

……….

Share of Foreign and Domestic Payments

While the proportion of IORB payments to foreign banks has decreased slightly since 2013, the gross amount in payments sent to foreign banks continues to grow substantially each year as the Fed has increased IORB rates. In 2019, prior to the pandemic, $13 billion in IORB payments were paid to foreign banks. Since 2022, however, the Fed has paid an average of $50 billion in IORB payments to foreign institutions and this number continues to grow.

As IORB rates drastically increased in late 2021 and 2022, not only did domestic banks rush to park capital at the Fed, but foreign banks also seemed to inject dormant capital from their international banks into their U.S. subsidiary to take advantage of the more generous risk-free interest offered for excess reserves. The share of IORB payments jumped from 28.5 percent foreign banks (the lowest since 2013) to nearly 40 percent of payments….

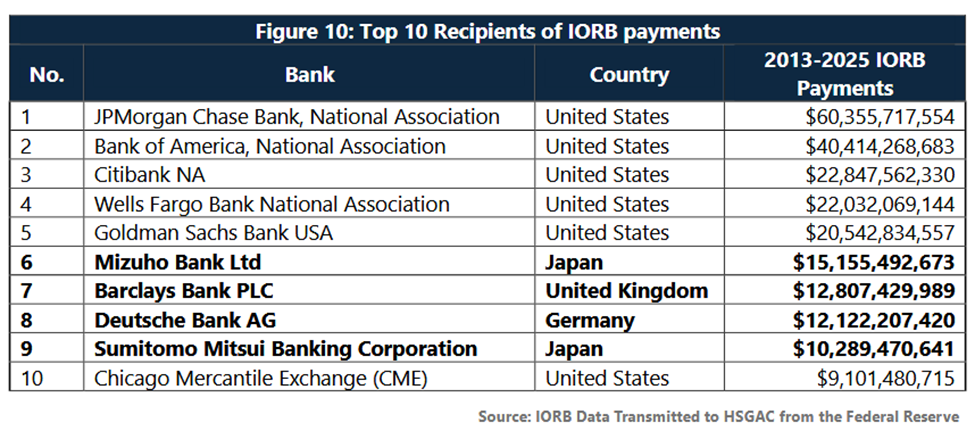

Many of the world’s largest banks have been the largest beneficiaries of IORB payments. Of top 10 recipients of IORB payments from July 2013 to July 2025, 4 are foreign banks (bolded), and 11 of the top 20 are foreign banks…:

IORB Payments as a Foreign Bank Subsidy

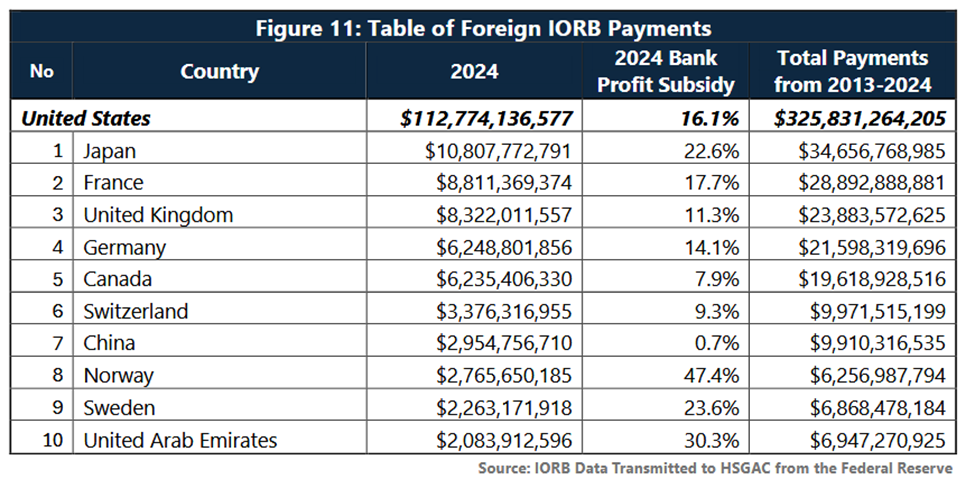

In 2024, while 16.1 percent of the U.S.’s banking sector’s net interest income comes at the expense of the taxpayer through IORB, 5 percent of all the participating foreign banks net interest income comes from the U.S. taxpayer. Figure 11 shows the top 10 benefitting nations and the percentage of bank profits is subsidized by the U.S. taxpayer.

“Bank profit subsidy” reflects the percent of participating depository institution’s net interest income that is attributable to IORB payments from the Fed. Notably,

the American taxpayer has financed over 50 percent of Bahrain’s bank profits, 47 percent of Norway’s bank profits, and 22 percent of Japan’s bank profits…

Conclusion: Hundreds of billions of dollars for the taxpayer have been sent to foreign banks, hundreds of billions of dollars for the taxpayer have padded Wall Street’s profit margin, all without a single election, public debate, or independent audit. This is the first step in what should be a continued effort to audit the Federal Reserve.

Full report: https://www.tristatehomepage.com/wp-content/uploads/sites/92/2025/12/2025.12.08_IORB-Report-VFINAL.pdf

__________________________________

Again: “This costly means of conducting monetary policy has prevented the Fed from remitting profits to Treasury to pay down the Federal deficit and instead directed these funds into Wall Street’s profit margins.”

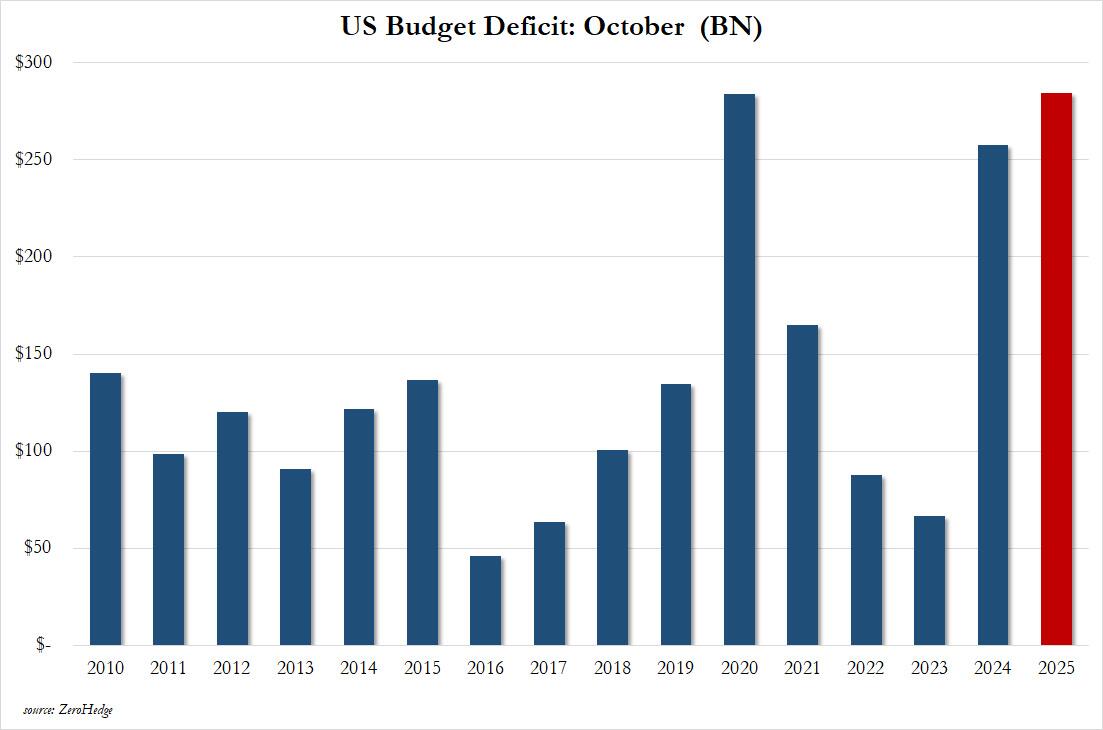

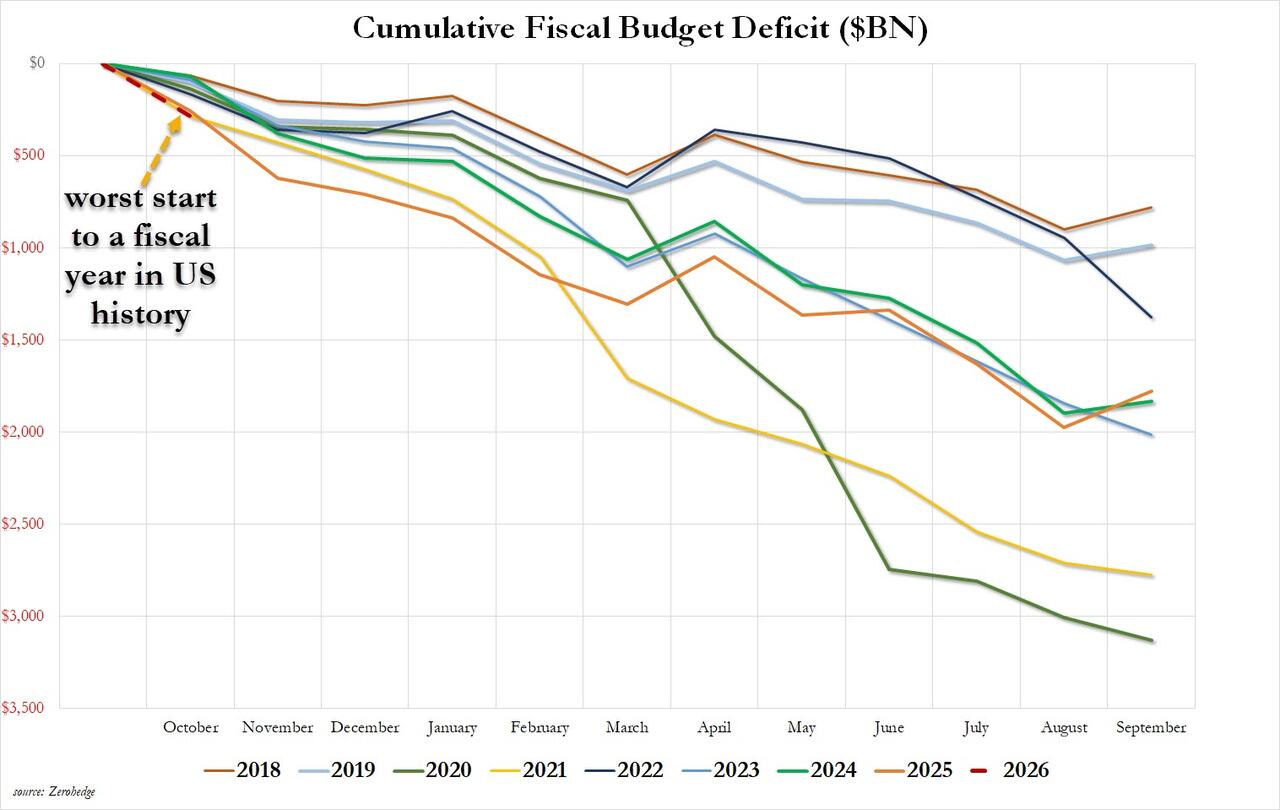

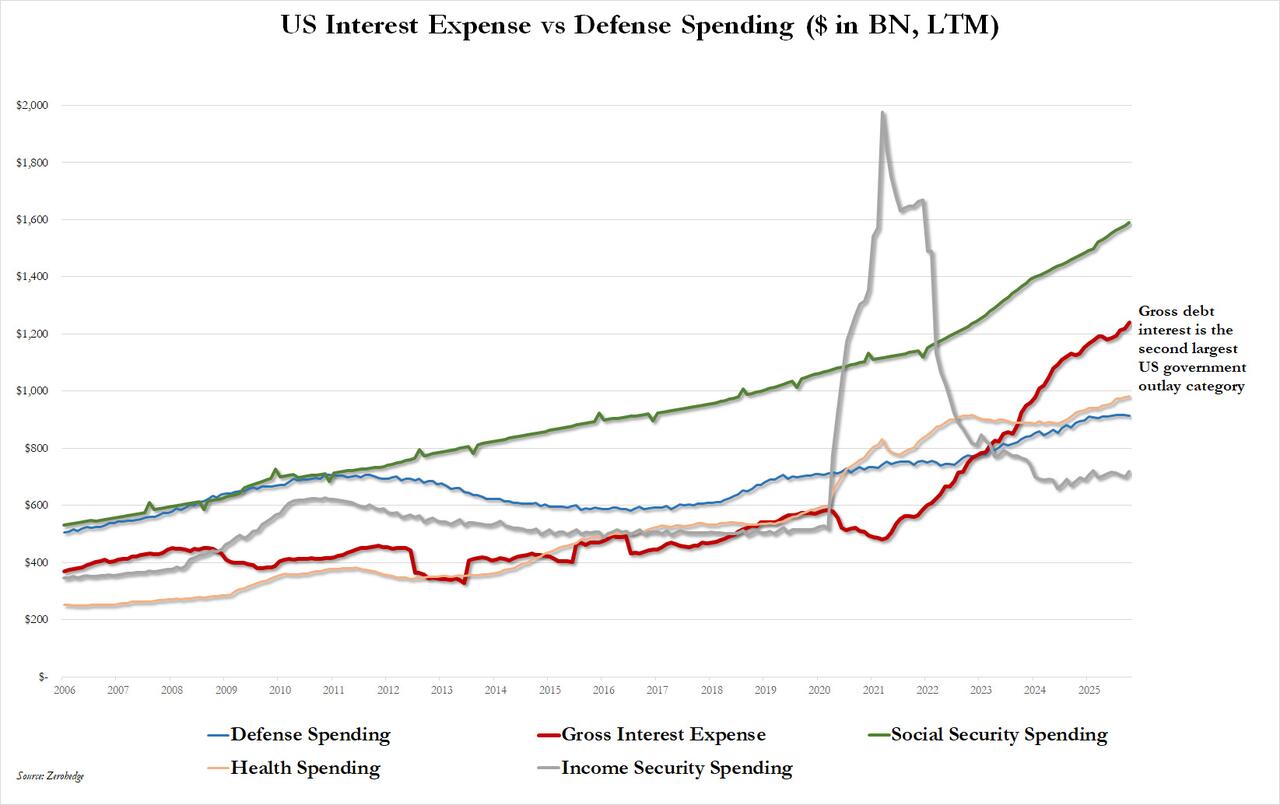

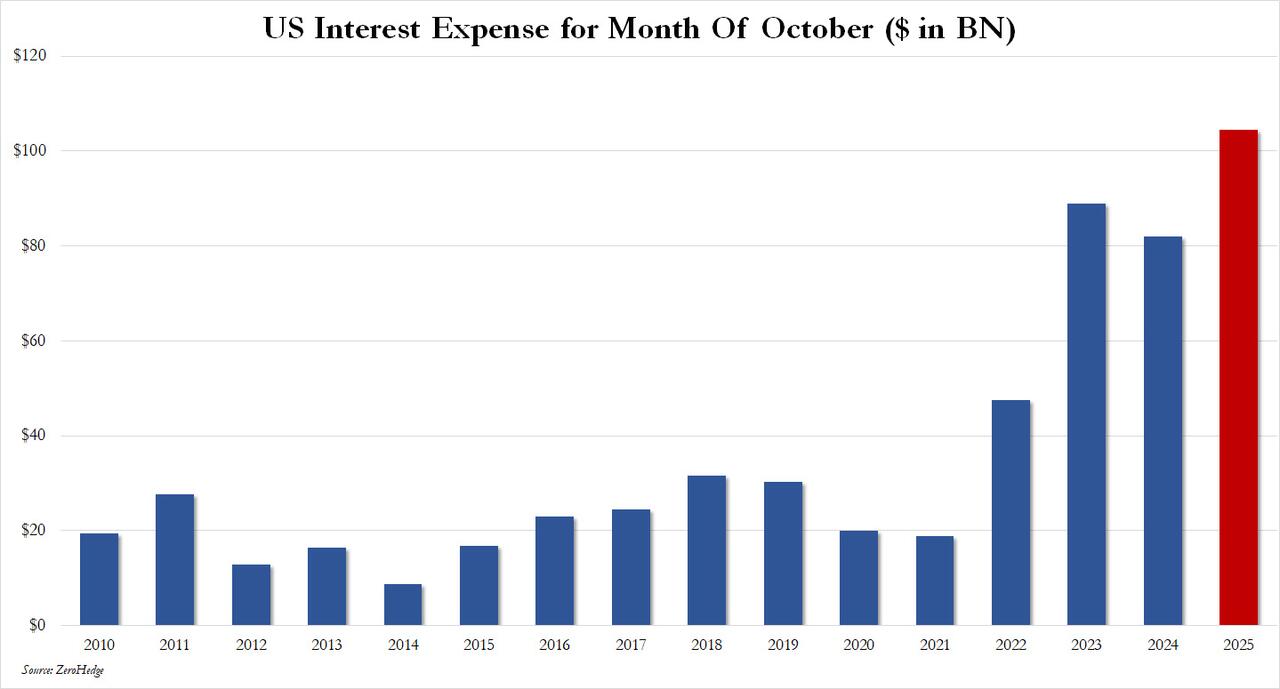

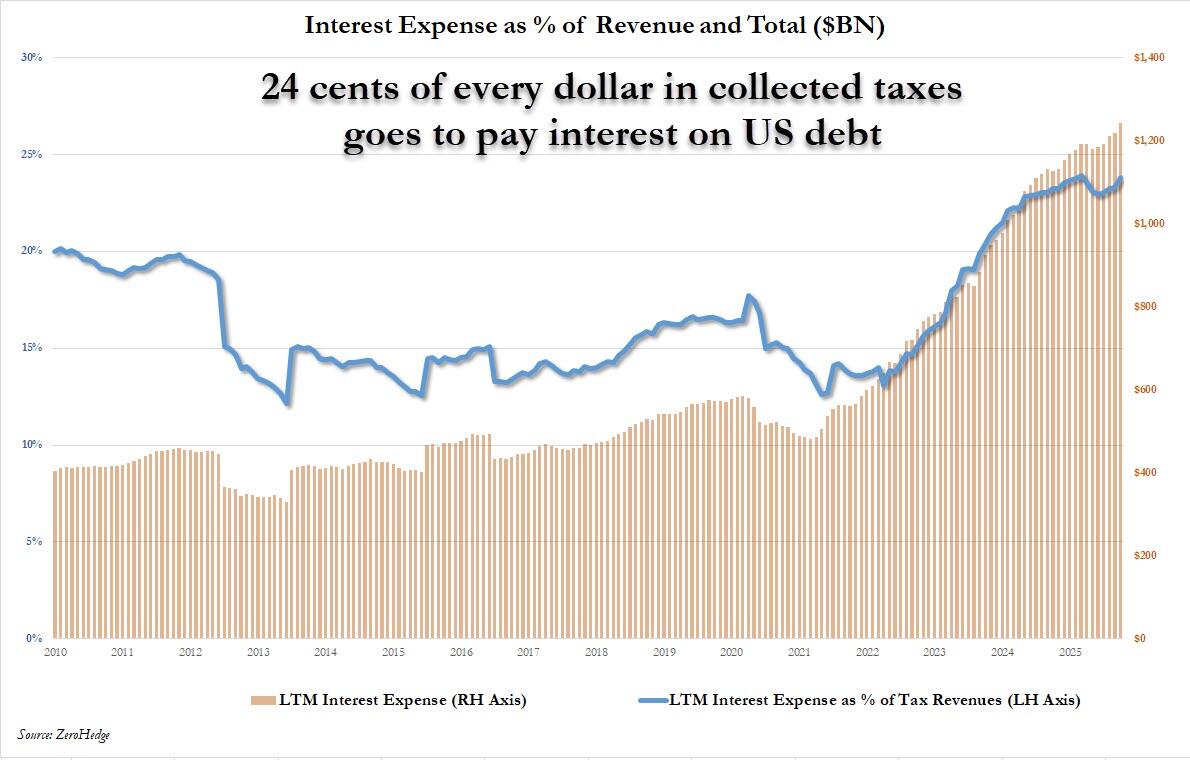

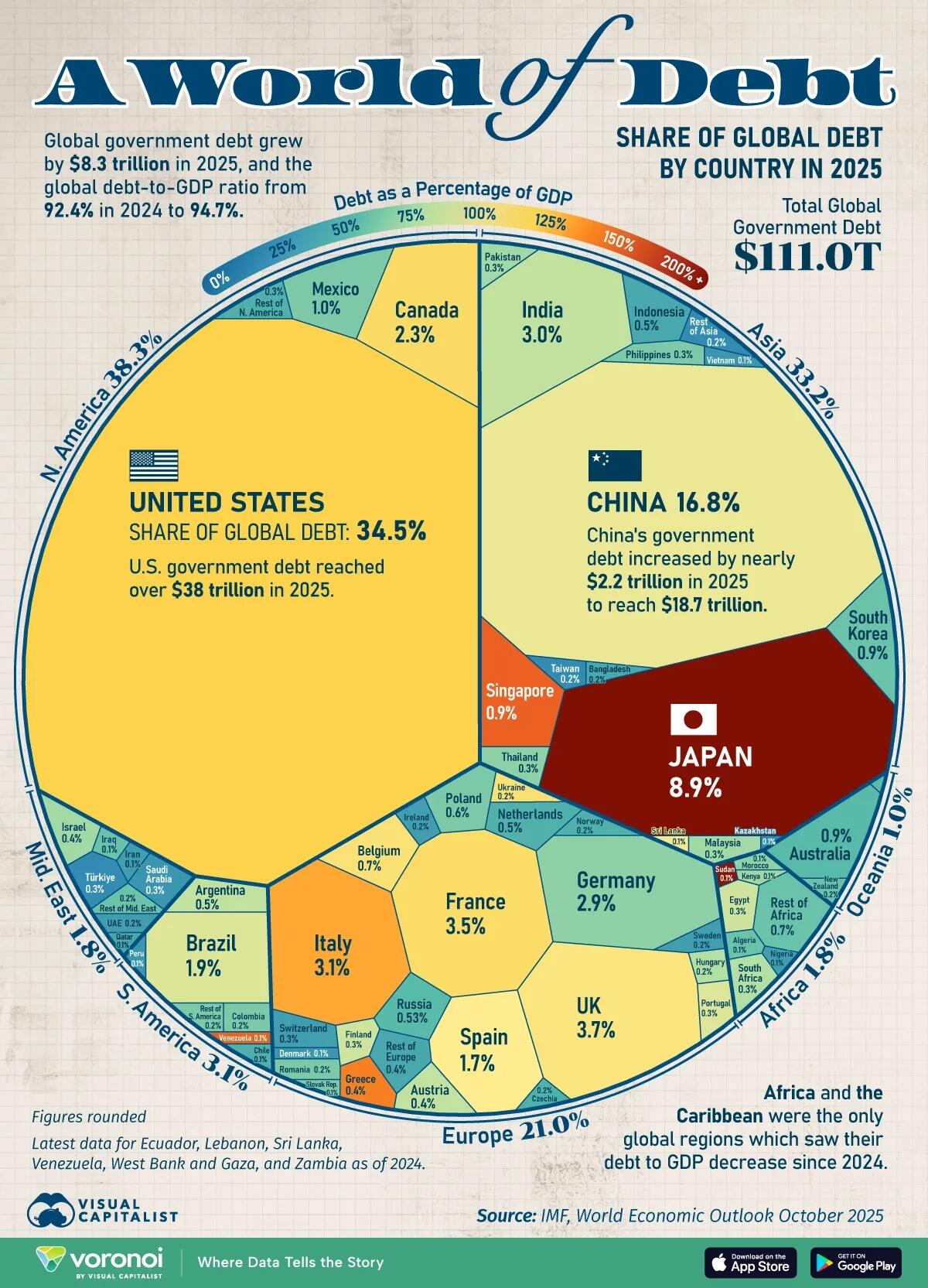

Federal budget deficits are skyrocketing as major Wall Street and foreign banks are being subsidized with hundreds of billions of dollars in Fed IORB payments.

Main Street America is paying a steep price for this ongoing kleptocratic snow job. The country is wallowing in debt… while the Fed is doling out hundreds of billions of dollars to pump up the profit margins of Wall Street’s largest banks and major foreign banks.

Main Street America Republicans have the plan to re-target Fed liquidity flows to pass through the hands of tax-paying U.S. citizens first, and then into the banking system (through Household debt service / elimination), and into America’s small business sector, and into savings and investing vehicles.

The Leviticus 25 Plan will generate federal budget surpluses of $37.303 billion each of its first five years of activation (2027-2031) and pay for itself entirely over the succeeding 10-15 years.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$95,000 per U.S. citizen – Leviticus 25 Plan 2026 (43426 downloads )

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}