Fortis Bank SA/NV was a large Dutch-Belgian banking and insurance conglomerate, the 20th largest revenue-generating company in the world in 2007. It rolled the liquidity-draining dice with its massive 2007 acquisition of ABN AMRO, and then again with its heavy exposure to U.S. subprime mortgages. The financial crisis hit, and down went Fortis. The Fed promptly opened up its big beautiful bailout water cannon and pumped billions of dollars directly onto Fortis’ tattered and worn balance sheet.

Bloomberg Nov 28, 2011: “Fortis Bank SA/NV, the banking unit of Brussels-based Fortis, was broken up after getting 7.2 billion euros ($10.3 billion) of capital from the governments of Belgium and Luxembourg in September 2008. It was later nationalized. Belgium sold a 75 percent stake in the bank to Paris-based BNP Paribas SA in an all-stock transaction that took seven months to complete. In a 2009 report, Fortis disclosed borrowing as much as 58.7 billion euros from the emergency liquidity lending facilities of the Belgian and Dutch central banks in October 2008. Data show Fortis Bank also tapped the U.S. Federal Reserve’s discount window, taking a $7 billion overnight loan on Sept. 29, 2008, and as much as $26.3 billion in February 2009 from the Commercial Paper Funding Facility and Term Auction Facility.

Peak Amount of Debt on 2/26/2009: $26.3B _____________________________________

The Federal Reserve’s “secret liquidity lifeline” bailouts of U.S. and foreign banks set the stage for a gradual, long-term erosion of the U.S. Dollar.

American citizens indirectly financed those massive ‘free money’ Wall Street financial sector bailouts through a loss of U.S. Dollar purchasing power.

American families deserve nothing less than the same direct access to credit that U.S. and foreign banks received during the global financial crisis of 2007-2010. It is time to restore American families to economic “health.”

Hypo Real Estate Holding AG, based in Munich, Germany, is a financial enterprise consisting of a group of banks that specialize in real estate financing.

Hypo purchased Ireland-based Debfa Bank in October 2007. Debfa promptly ‘took on water’ in 2008 when a boat load of municipal bonds it had underwritten got downgraded.

Depfa’s heavy debt burdens quickly dragged Hypo down into the debt swamp during the global financial crisis.

And then…..

The U.S. Federal Reserve galloped in to the rescue, courtesy of U.S. taxpayers, to help bail out Germany-based Hypo in the fall of 2008.

Bloomberg Nov 28, 2011: “Hypo Real Estate Holding AG, a German commercial-property lender with 1,366 employees, borrowed as much as $28.7 billion in November 2008 from the U.S. Federal Reserve through the New York branch of its Depfa Bank Plc unit. That’s about $21 million per employee. It borrowed almost one-third as much as Citigroup Inc., which has 190 times as many employees.

The Fed aid came in addition to 142 billion euros ($206 billion) of emergency credit lines and debt guarantees from German authorities. Hypo, which invested in mortgage-backed securities in the years before the financial crisis, said in a 2009 report that it lost access to short-term funding after Lehman Brothers Holdings Inc.’s bankruptcy. Hypo didn’t disclose any Fed borrowings until the loans became public in 2011.”

Peak Amount of Debt on 11/4/2008: $28.7B

_______________________________________

If the U.S. Federal Reserve can rescue foreign financial corporations like Hypo Real Estate Holding ($28.7B in direct liquidity transfusions), from their disastrous investment decision-making – then the Fed also has the power to grant direct liquidity extensions also to American families to help relieve debt burdens and restore the financial health of U.S. citizens.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

BNP Paribas is the largest bank in the Eurozone and 10th largest bank worldwide. The French bank is headquartered in Paris, with global headquarters in London. It owns subsidiaries all over the world, including BankWest in the U.S..

“BNP Paribas escaped the 2007–09 credit crisis relatively unscathed reporting a €3 billion net profit for the year of 2008, and €5.8 billion for 2009.”

“TARP Recipient BNP Paribas got $4.9bn of bailouts from the U.S. Taxpayer – Today, as the WSJ reports we learn BNP Paribas has been funding transactions in Iran, Syria and other countries subject to U.S. Sanctions since 2002. The bank set aside $1.1 billion to settle investigations by the Department of Justice and the Federal Reserve but as the NY Times reports, investigations are playing out on multiple fronts – centering on whether the firm did “a significant amount” of business in “blacklisted” countries (and routed the deals through the US financial system).”

Via WSJ, – “…an internal probe conducted over the past few years “a significant volume of transactions” between 2002 and 2009 that could be “considered impermissible under U.S. laws and regulations...” “involving entities that were doing business in U.S.-sanctioned countries, such as Iran, Cuba, Sudan and Libya during the 2002 to 2009 period.

“BNP Paribas SA on Thursday became the latest bank to disclose the extent of its litigation problems in the U.S., saying it has set aside $1.1 billion against potential penalties related to transactions in countries under sanctions...

Oct. 19, 2011 (Bloomberg) — “BNP Paribas SA was sued by the U.S. over allegations the Paris-based bank aided a grain export fraud scheme involving commodity payment guarantees provided by the Department of Agriculture.

A corporate banker in BNP’s Houston office allegedly helped a scheme that defrauded the Agriculture Department of at least $78 million through deals he made with four U.S. grain exporters, according to a complaint filed yesterday in federal court in Houston.”

“The credit crisis accelerated after BNP Paribas SA, France’s biggest bank, announced in August 2007 that it would halt withdrawals from three funds because mortgage-market turmoil “made it impossible” to value certain assets. BNP began taking Federal Reserve loans in December 2007 when the Term Auction Facility opened.

By April 2008, its Fed debt reached $29.3 billion. In 2009, BNP became the euro region’s largest bank by deposits, purchasing Brussels-based Fortis’s units in Belgium and Luxembourg for 10.4 billion euros ($15.2 billion). It issued 5.1 billion euros of preference shares to the French government in March 2009, and reimbursed the state by October. In December 2010, when the Fed disclosed the loans, BNP said it used the TAF “to assist in recycling and facilitating liquidity.”

Peak Amount of Debt on 4/18/2008: $29.3B

_______________________________________

BNP Paribas received $4.9 billion in TARP funds from the U.S., and they went on to rake in a tidy $29.3 billion credit extension from the Fed via the Term Auction Facility… “to assist in recycling and facilitating liquidity.”

They were meanwhile funding significant transactions (Bloomberg) “involving entities that were doing business in U.S.-sanctioned countries, such as Iran, Cuba, Sudan and Libya during the 2002 to 2009 period.” And they ran a “grain export fraud scheme” which ‘cooked’ the U.S. Department of Agriculture for a cool $78 million.

The $64,000 question: If BNP Paribas is deserving of direct cash infusions from the U.S. government and the Fed, then would it not be perfectly reasonable for U.S. citizens to also qualify for their own direct credit extensions “to assist in recycling and facilitating liquidity” at the family level.

“Former Bear Stearns mortgage executives who now run mortgage divisions of Goldman Sachs, Bank of America, and Ally Financial have been accused of cheating and defrauding investors through the mortgage securities they created and sold while at Bear.

Last week a lawsuit filed in 2008 by mortgage insurer Ambac Assurance Corp against Bear Stearns and JPMorgan was unsealed. The lawsuit’s supporting e-mails, going back as far as 2005, highlight Bear traders telling their superiors they were selling investors like Ambac a “sack of [sh#%].”

………

According to the lawsuit, the Bear traders would sell toxic mortgage securities to investors and then sell back the bad loans with early payment defaults to the banks that originated them at a discount. The traders would pocket the refund, and would not pass it on to the mortgage trust, which was where it should have gone to be distributed to the investors who owned the bonds.

It was this blatant internal awareness inside the Bear mortgage trading division that the Ambac suits says led Bear to implement an across-the-board strategy to disregard its contractual promises and conceal the defective loans….

In 2007, when Ambac started to realize something was very wrong with its high-rated bonds, it demanded Bear provide loan-level detail and reviewed 695 non-performing loans in its portfolio. Ambac’s audit concluded that 80 percent of the loans showed an early payment default….

Bear Stearns Cos. Chairman James “Jimmy” Cayne told the Financial Crisis Inquiry Commission that the Federal Reserve’s Primary Dealer Credit Facility, set up in March 2008 to supply emergency funding to brokerage firms, came “just about 45 minutes” too late. Without access to liquidity from the central bank, New York-based Bear Stearns had to sell itself to JPMorgan Chase & Co., ending 85 years as an independent firm. To prop up Bear Stearns while the deal could be negotiated, the Fed extended a $12.9 billion emergency loan to the firm through JPMorgan. After the deal was inked, the Fed supplied as much as $30 billion to Bear Stearns through the PDCF and single-tranche open market operations to float the firm while the takeover was pending.

Peak Amount of Debt on 3/28/2008: $30B

_______________________________________

U.S. citizens, who did not cheat and defraud investors by peddling toxic mortgage securities – deserve nothing less than to be granted the same access to liquidity that the Federal Reserve supplied to Bear Stearns and scores of other major banks and insurers during great financial crisis of 2007 – 2010.

The mechanism for this direct access to liquidity – a Citizens Credit Facility – via The Leviticus 25 Plan.

“Wells Fargo & Co. became the largest U.S. home lender and fourth-biggest bank after purchasing Wachovia Corp. in 2008 as that bank was teetering near collapse. Wells Fargo, based in San Francisco, borrowed as much as $45 billion in February 2009, a day after regulators released details of how they would conduct stress tests on the nation’s 19 largest banks.

The Fed’s Term Auction Facility was “one of several programs offered by the government that Wells Fargo and other financial institutions were encouraged or required to participate in,” said Ancel Martinez, a spokesman for the bank.”

Peak amount of debt on 2/26/2009: $45B

……………………………..

Wells Fargo By Philip Mattera Wells Fargo is the smallest of the four giants that now dominate the U.S. commercial banking business, but it has surpassed its larger counterparts in the extent to which it has been embroiled in a series of scandals involving reckless lending practices and customer deception.

Honest, hard-working, tax-paying U.S. citizens, the backbone of our Republic, deserve nothing less than to be granted the same direct access to liquidity, through a U.S. Citizens Credit Facility, that the Fed so graciously provided to Wells Fargo & Co and other major banks during the height of the financial crisis.

In 2007 and 2008, Lehman Brothers Holdings Inc engaged in some old-fashioned, end-of-quarter, creative ‘book-cooking” to disguise their quietly snowballing insolvency issues….

Their financial sleight-of-hand involved book-keeping entries known as “Repo 105s” – where late-quarter temporary loans backed by ‘depressed’ assets were booked as ‘sales,’ with the revenues then ‘used’ to pay down debt. This provided “window dressing” for their quarterly reports to, naturally, make ‘management’ look good. Lehman would then ‘buy’ the asset back and add the old debt back in early in the new quarter.

Lehman ran up $50 billion worth of ‘Repo 105s’ in 2008. Auditor Ernst & Young ‘winked’ at the Lehman ‘shell game.’

The financial crisis quickly blew the game up in the fall of 2008.

“Lehman Brothers Holdings Inc. filed for bankruptcy on Sept. 15, 2008, after U.S. Treasury Secretary Henry Paulson refused to authorize a government bailout for the New York-based securities firm. By then, the Fed had supplied liquidity to Lehman’s main brokerage unit, Lehman Brothers Inc., for months, reaching $31.1 billion in June 2008.

On the day of the bankruptcy, Lehman’s Fed loans reached $44.8 billion. Barclays Plc took over some of the debt after buying Lehman’s North American securities business, according to court testimony. Lehman Brothers Inc. repaid $38.5 billion on Sept. 18, and Barclays’s Fed borrowings jumped by $49.1 billion to $63.8 billion that day, the data show.”

Peak amount of Debt on 9/15/2008: $46B

_____________________

In review – ‘book-cooker’ Lehman Brothers received massive liquidity infusions from the Fed… and Barclays received massive Fed-generated liquidity access to buy ‘book-cooker’ Lehman.

Meanwhile, U.S. citizens, who did not ‘cook books,’ paid dearly for the shocking credit meltdown precipitated by Lehman and others. Hardworking Americans suffered through billions of dollars of lost income, catastrophic job losses throughout the economy, and millions of home foreclosures sat and watched the as Fed transfused Lehman and Barclays with tens of billions of dollars of ‘magically created’ electronic money, while Main Street America got nothing.

It is time now to level the playing field and grant U.S. citizens, through a Citizens Credit Facility, the very same access to Fed liquidity that Lehman, Barclays, and dozens of other banking titans received.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

…When Henry Paulson steps back into the public conversation after years of relative silence, it’s not random timing. This is someone who sat at the center of the 2008 financial crisis and understands how quickly confidence can evaporate once stress begins to build in core markets….Paulson is explicitly warning that the scale of U.S. borrowing is now testing confidence in the Treasury market itself. With federal debt approaching $39 trillion, he points to the risk that the long-standing assumption of endless demand for U.S. government debt may no longer hold.

As he put it, “That’s a dangerous thing,” describing a scenario where foreign demand declines and Treasury prices fall. That is not a small shift in tone. The entire global financial system is built on the idea that Treasuries are the ultimate safe asset, and once that perception begins to weaken, the consequences cascade quickly.

What stands out even more is what he says next about how such a situation would resolve: “Should enough investors back out… the Federal Reserve would step in as a buyer of last resort.”

And as we all know, a “buyer of last resort” is simply another way of describing a return to large-scale intervention by the Federal Reserve. Whether policymakers call it stabilization, liquidity support, or something else (like the A.S.S.H.O.L.E.S. plan), the mechanism is the same: the central bank absorbs supply when the market no longer can. In other words, quantitative easing returns.

That leaves two realistic interpretations of why Paulson is speaking now.

Either he sees early signs of stress already forming beneath the surface of the Treasury market—declining foreign participation, weakening liquidity, or rising yields that are no longer being absorbed smoothly.

Or he is helping prepare the narrative for the policy response that will follow when those stresses become undeniable. Those two possibilities are not mutually exclusive. In fact, they often occur together.

His comments about needing an emergency response framework make that even clearer. He said, “We need an emergency break-the-glass plan… ready to go when we hit the wall,” and followed it with “It will be vicious.”

Notice he said when we hit the wall, not if.

That is not the language of a former official casually discussing long-term fiscal challenges. It is the language of someone who expects a disorderly adjustment and understands how quickly conditions can spiral once confidence breaks.

Markets already assume that after the next deleveraging cycle, central banks will return to QE. That part is widely understood. What is not fully appreciated is the implication if the stress originates inside the Treasury market itself. Treasuries are not just another asset class. They underpin global collateral systems, anchor borrowing costs across the economy, and support the U.S. dollar reserve currency status. If confidence in that market begins to erode, the feedback loop is far more severe than a typical recessionary downturn.

In that scenario, the Federal Reserve stepping in as the marginal buyer would not simply stabilize markets. It would fundamentally alter how capital allocates globally. Real yields could compress rapidly, confidence in fiat stability could weaken, and capital could rotate into hard assets at a pace that exceeds even aggressive expectations. The move would not just be cyclical, it would be structural.

The second-order risk is even more significant. If foreign demand for Treasuries fades and the U.S. increasingly relies on its own central bank to finance deficits, the signal to the rest of the world is unmistakable. That is how pressure begins to build on a reserve currency. An FX adjustment tied to the dollar is not the base case today, but neither was a systemic breakdown in mortgage markets prior to 2008. These transitions always look implausible until they are suddenly obvious.

The key point is that Paulson is not someone who reappears without purpose. He understands the plumbing of the system and the fragility that sits beneath it when leverage is high and confidence is stretched. His warning that “We have to prepare for that eventuality” should not be dismissed as generic caution. It suggests that the risks are no longer theoretical.

There is more in his comments than a simple observation about rising debt levels. Either he sees stress forming already, or he is preparing markets for the policy response that will follow when that stress becomes visible. In both cases, the implication is the same: something larger is developing beneath the surface of the Treasury market, and when it breaks into the open, the consequences will extend far beyond bonds.

_____________________________

The Leviticus 25 Plan is a preemptive “emergency break-the-glass plan,” ready to go now — before we “hit the wall.”

The Leviticus 25 Plan re-targets Fed liquidity flows in a way that will preemptively generate substantial ongoing federal budget surpluses, structurally downsize federal, state, and local government outlays, eliminate massive amounts of household debt, and revitalize ‘non-debt-driven’ economic growth.

The most powerful decentralizing economic acceleration plan in the world.

Wachovia had grown into a coveted spot of the fourth largest bank holding company in the U.S. when the Mortgage Backed Securities mania imploded and Wachovia melted down and was eventually acquired by Wells Fargo.

……………………………..

Wachovia Corp’s investment portfolio “began to go up in smoke” in the fall of 2008 with the collapse of the “housing boom.” Depositors got nervous and began “pulling their money out of the bank.” (Griftopia – Matt Taibbi)

Something had to be done. The bank was deemed “systemically important” by a frantic Fed and FDIC.

Wells Fargo was urged to assist, but was naturally reluctant to get involved. But then some old-fashioned “backroom” prompting by the Fed/Treasury sweetened the deal, and Wells Fargo stepped up to save the day.

Treasury Secretary Hank Paulson “promised” a deal that would work out to “an almost $25 billion tax break for Wells Fargo” going forward. And then Wells Fargo received their TARP apportionment of $25 billion in cash. Wells Fargo immediately decided it could “help the government out” and purchase Wachovia – for the fire-sale price of $12.7 billion.

Wachovia Corp., which almost collapsed in September 2008 because of a deposit run, floated itself with Federal Reserve funds the following month after becoming the object of a takeover battle between Citigroup Inc. and Wells Fargo & Co. Fed assistance for Charlotte, North Carolina-based Wachovia included a $29 billion loan on Oct. 6, 2008, from the discount window, the biggest of any U.S. bank during the crisis from the central bank’s 97-year-old lender-of-last-resort program. Wachovia also borrowed from the Term Auction Facility, bringing total Fed liquidity to $50 billion.

Peak amount of debt on 10/9/2008: $50B

……………………………………………….

U.S. taxpayers to the rescue…

Banks like Wachovia regained their ‘healthy glow’ … while main street America remains buried in debt, and now, increasingly roiled by inflation.

The Leviticus 25 Plan would level the playing field with equal access to liquidity, via a Citizens Credit Facility, for America’s hard-working, tax-paying families. It would restore economic liberty and provide dynamic, long-term benefits for all U.S. citizens.

“The biggest U.S. banks avoided the discount window, the Federal Reserve’s 97-year-old last-resort lending facility, partly out of concern that tapping it might brand them as weak. Dexia SA, a lender to local governments in Belgium, showed no such reservation.

The bank, based in Brussels and Paris, was the discount window’s biggest borrower during the crisis, tapping it for $37 billion in December 2008.

Dexia simultaneously borrowed $21.5 billion from temporary Fed programs that were primary sources of emergency funding for U.S.-based Citigroup Inc., Bank of America Corp. and JPMorgan Chase & Co. In all, Dexia owed about 120 billion euros ($168 billion) to central banks at the end of 2008. As of June 30, 2011, it still had 34 billion euros of central-bank funding.”

Peak amount of debt as of 12/31/2008: $58.5B

___________________________________________

Dexia SA suffered massive net losses during 2008 and 2009 from a stream of wild, reckless investments involving Icelandic Banks, Lehman Brothers, Washington Mutual, Greek government bonds, and of all things.. investments involving Bernard Madoff’s revolving Ponzi scheme.

Since Dexia had an office in New York, they qualified for massive liquidity infusions, courtesy of the U.S. Federal Reserve.

___________________________________

There is perfect justification in all of this for U.S. citizens to now be granted the same direct access to liquidity, to mitigate their own financial burdens, that was provided to major foreign banks including Dexia, Barclays, HSBC, UBS, Royal Bank of Scotland, DeutscheBank and others.

It is now time for U.S. to level the playing field.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The U.S. Federal Reserve generously infused major Wall Street global financial institutions, including foreign banks, with massive liquidity infusions during the height of the great financial crisis of 2007-2010.

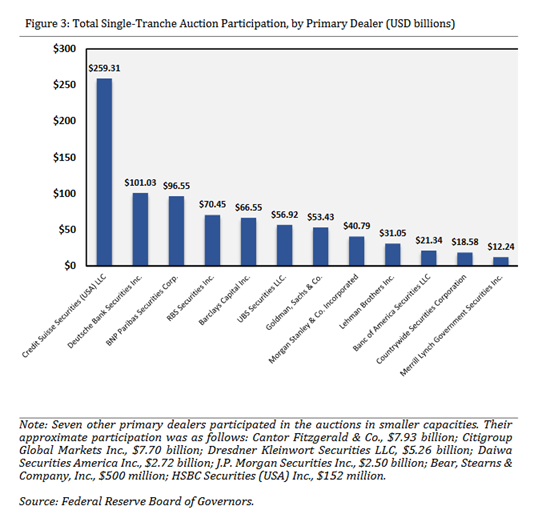

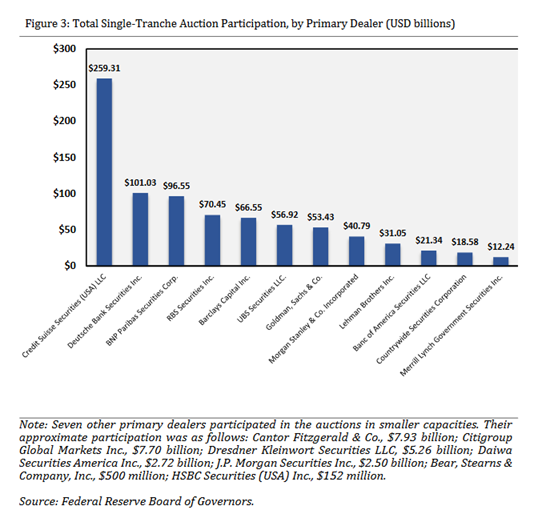

One of the biggest recipients of the Fed’s generosity: Switzerland-based Credit Suisse…

“Credit Suisse Group AG, Switzerland’s second-biggest bank by assets, was the biggest user of the Fed’s single-tranche open market operations, or ST OMO, borrowing $45 billion in August 2008. Under ST OMO, securities firms swapped eligible mortgage bonds for cash.

The Zurich-based bank’s U.S. brokerage also used the Term Securities Lending Facility, which allowed firms to swap certain debt securities for Treasuries that could be loaned out or sold for cash. Credit Suisse took no part in any central bank’s collateralized funding facilities in the crisis, said Steven Vames, a bank spokesman in New York. TSLF doesn’t count because it involved no cash transfers, he said, and the bank borrowed from ST OMO only as a so-called primary dealer. Primary dealers weren’t required to bid in ST OMO.”

Peak Amount of Debt on 8/27/2008: $60.8B

………………………

What are single-tranche open market operations?

The Fed’s ‘secret liquidity lifelines that ran from 2007 – 2010 generally involved various credit facilities, set up to ‘rescue’ the banking system, and make banks ‘healthy.’

ST OMO’s were another unique form of liquidity infusions that provided “term funding” to the (big bank) Primary Dealers, primarily benefiting major European (Primary Dealer) banks. – for the purpose of “mitigating heightened stress in funding markets.”

These ST OMO “secretive bailout operation” pumped out $855 billion between “March and December 2008.”

“These operations were conducted by the Federal Reserve Bank of New York with primary dealers as counterparties through an auction process under the standard legal authority for conducting temporary open market operations. In these transactions, primary dealers could deliver any of the types of securities–Treasuries, agency debt, or agency MBS–that are accepted in regular open market operations. By providing term funding to primary dealers, this program helped to address liquidity pressures evident across a number of financing markets and supported the flow of credit to U.S. households and business.”

“Well, not really. As the chart below shows the banks, pardon, primary dealers, that benefited the most from this secret iteration of Fed generosity were once again foreign banks, with the Top 5 borrowers being Credit Suisse, Deutsche Bank, BNP Paribas, RBS and Barclays. Together these five accounted for $593 billion of total borrowings, or 70% of the total.”

Below is a summary of who borrowed how much in total from the Fed’s ST-OMO program.

U.S. citizens deserve direct access to the liquidity extensions and credit guarantees that the Fed pumped out to rescue the banking system during the crisis period (2007 – 2010) when high-risk sub-prime debt took on ‘junk’ status, and fairly well ‘froze’ the system.

Certain Fed operations, like single-tranche open market operations, heavily favored major European banks – designed to mitigate “heightened stress.”

It is now time for the Fed to activate a U.S. Citizens Credit Facility to grant direct liquidity access to U.S. citizens – to eliminate debt and help relieve “heightened stress” at the family level in America.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

{kind=link}