Did ObamaCare ‘Work’?

ZeroHedge, Dec 07, 2023 – Via Political Calculations blog, | Excerpts:

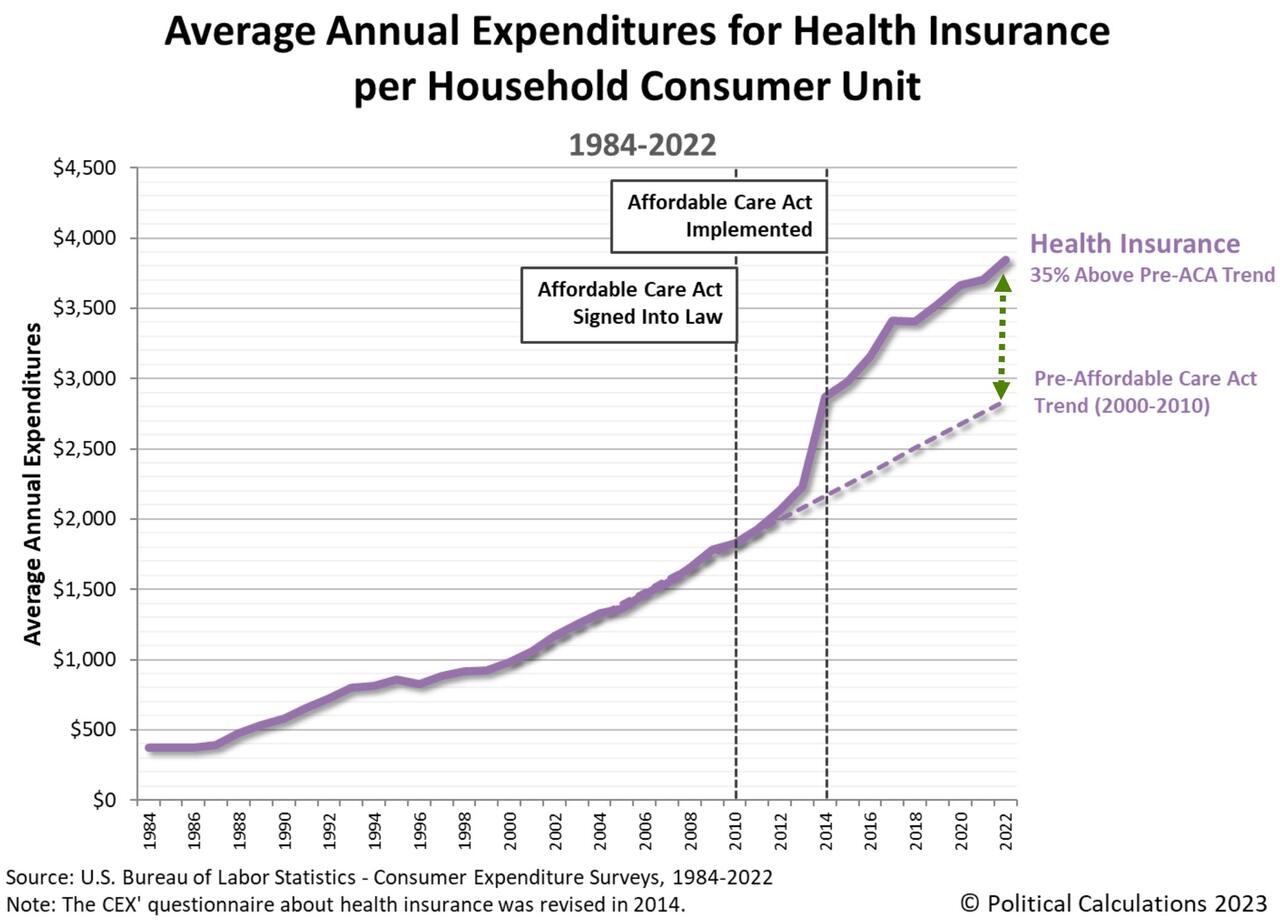

The Affordable Care Act was signed into law in 2010. It was slowly implemented, going into full effect in 2014. One of the main goals of the law was to make health insurance more affordable for Americans, but has it worked?

One way to answer that question is to see how much Americans are paying for health insurance since the ACA became law and to compare that how much American households would otherwise have paid if the preceding trend for health insurance costs remained in place.

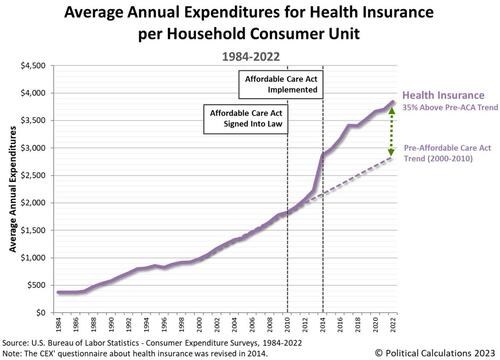

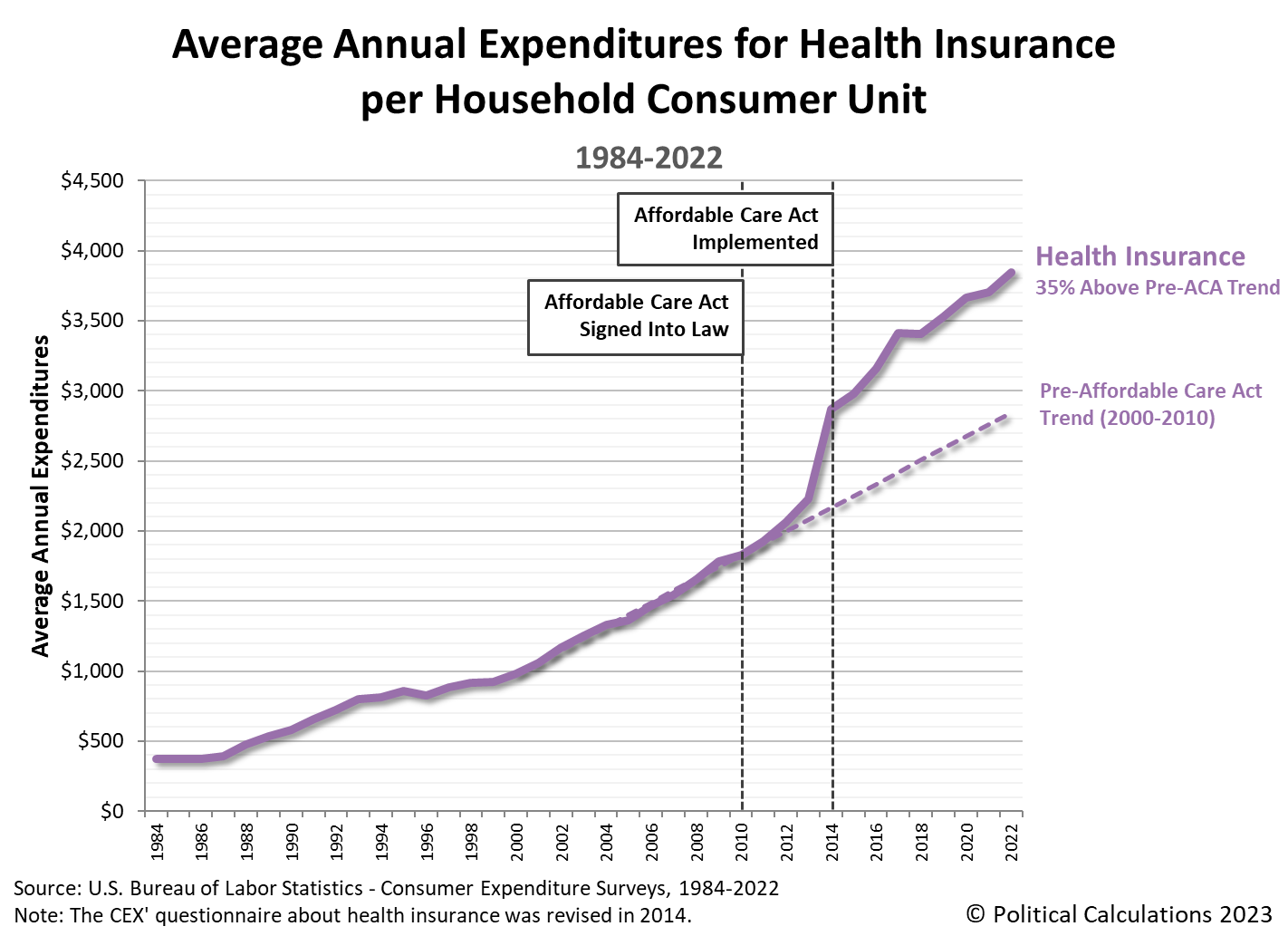

We can make comparison using data from the U.S. Census Bureau’s annual Consumer Expenditure (CEX) Survey. The CEX has reported how much an average “consumer unit”, which roughly corresponds to an American household, has paid for health insurance in each year from 1984 through 2022. It compares those data points with the trend based on the actual expenditures for health insurance from 2000 through 2010. Here’s the chart:

Compared to the pre-Affordable Care Act trend from 2000 through 2010, Americans household consumers paid 35% more on average for health insurance in 2022 than they would otherwise have paid based on the trend for these costs from 2000 through 2010.

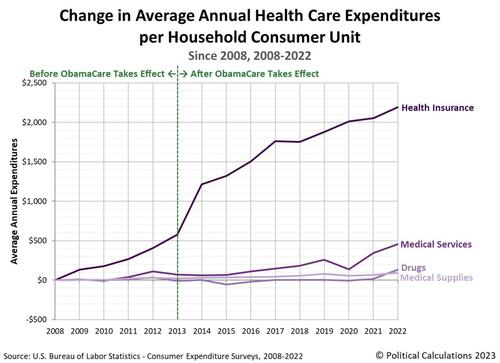

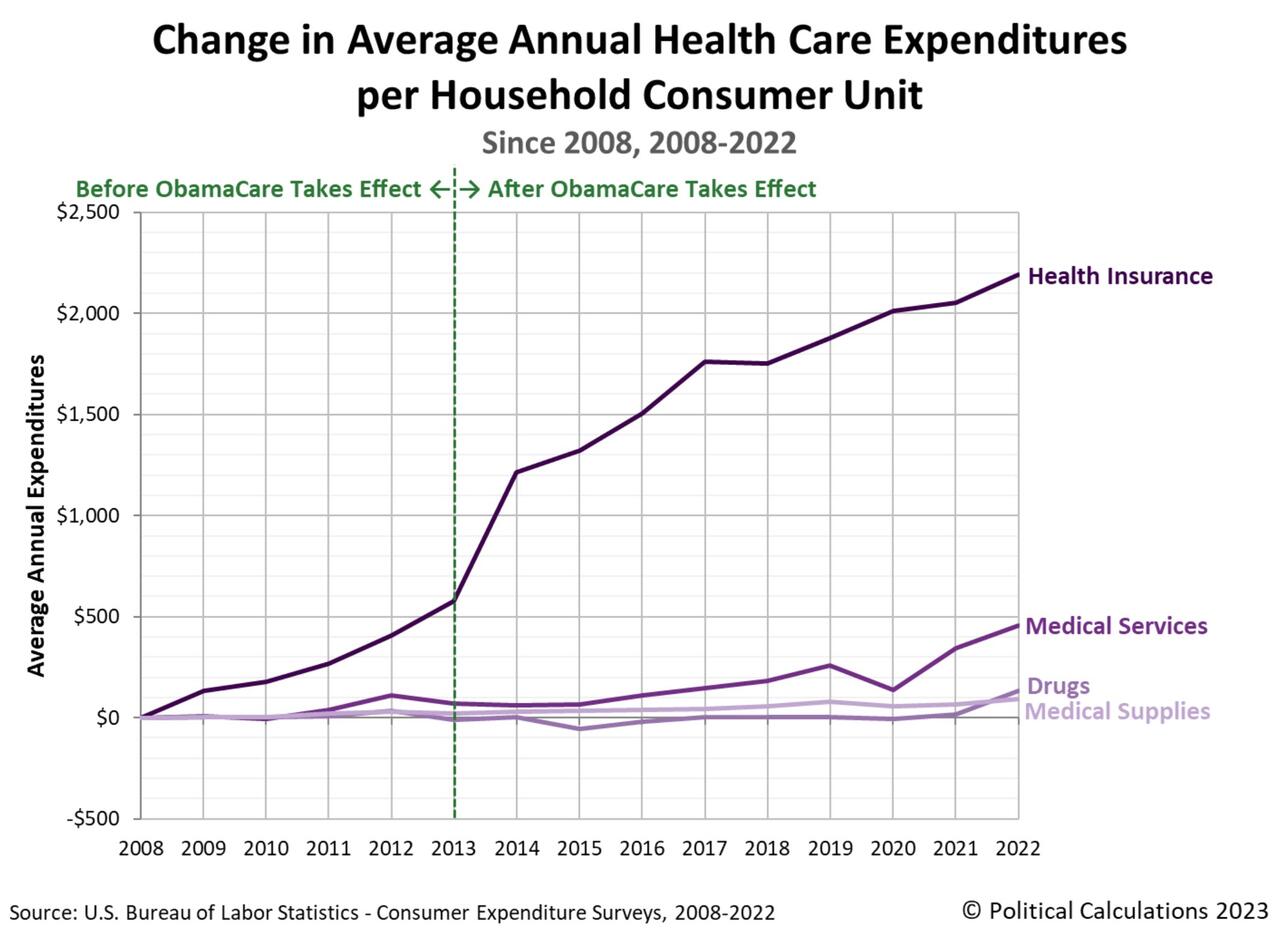

How does that compare with the household consumers’ other major health care expenditures? The chart is adapted from an older version and narrows in on the period from 2008 through 2022 to track the change in the average expenditures per American consumer unit for several health care expenditure categories. These categories include health insurance, medical services, drugs, and medical supplies.

Through 2022, what American household consumers pay for drugs and medical supplies has changed very little, with medical supplies within $95 and drugs within $133 of their cost in 2008.

Expenditures for medical services has seen more growth over time. In 2013, the year before the Affordable Care Act took full effect, Americans paid just $69 more for medical services than they did in 2008. By 2019, that increased to $257, which then dipped to $137 in the pandemic year of 2020. What American consumer households pay for medical services has risen rapidly since, as of 2022 they reached $457 more than they paid in 2008.

But what Americans pay for health insurance has relentlessly risen in all but one year (2017). In 2013, just before the Affordable Care Act became fully operational, Americans paid $576 more for health insurance than they did in 2008. That jumped immediately to $1,215 in 2014, and has since risen to be $2,190 more than what American consumer units paid for health insurance in 2008.

2022 is the most recent year for which we have figures available. The Census Bureau will collect the data for 2023 in March 2024 and will crunch the numbers for several months before reporting it all sometime in September 2024.

______________________

The U.S. Health Care Freedom Plan, an integral component of The Leviticus 25 Plan, will restore citizen-centered health care and summarily reduce ‘annual expenditure for health insurance’ by eliminating bureaucratic bloat, unfriendly and complicated medical access pathways, cumbersome, drawn-out claims processing, and rapidly shrinking reimbursements for physicians, pharmacists, and other health practitioners.

The U.S. Health Care Freedom Plan offers a powerful new access strategy for patients receiving medical and pharmaceutical services, home medical equipment, and home care services.

The Plan grants citizens the freedom to pay directly, in person, for their week-to-week health care purchases. It cuts out layers of bureaucracy and middlemen … simplifies access to health care and restores genuine ‘patient-provider’ relationships.

The U.S. Health Care Freedom Plan is the only comprehensive, citizen-centered health care plan in America. It ‘resets’ the health care industry to present a clean, efficient and responsible system. Most importantly, this plan restores individual citizen-centered health care for all participating Americans.

The U.S. Health Care Freedom Plan is available to each and every U.S. citizen – with no coverage mandates. Each U.S. citizen who wishes to participate will be granted a full and complete exemption from the ACA.

Each participating U.S. citizen shall receive a credit extension, through a special Federal Reserve / U.S. Treasury Citizens Credit Facility of $30,000, electronically deposited into a Medical Savings Account (MSA) – for direct allocation toward family health care needs.

Private insurance – Families shall be allowed to enroll in high-deductible major medical plans, that include basic, ‘no frills’ medical plans which best suit their individual needs and desires. These streamlined plans would lower premium costs for employees and employers, encouraging employers to cost-share savings with employees through incentive-based employer MSA contributions.

Those with extraordinary medical issues may be included in a high-risk category, with such plans being eligible for a government subsidy (similar to current Medicare Advantage).

Federal / state programs – Individuals enrolled in Medicare / Medicaid / VA / TRICARE / FEHB programs would maintain their covered status, with an annual deductible of $6,000 per year per enrolled family member, for a period of five years for those benefits. The dedicated MSA funds would fully fund the offset for the higher ($6,000) deductible feature for that five-year period. MSA funds could also be used to pay Medicare supplement premiums and other potential co-pay obligations.

Where health care services paid by patients directly with MSA funds, providers would not be bound by federal / state rules pertaining to Electronic Medical Records (EMRs), and other unnecessary administrative burdens.

………………………………….

The Leviticus 25 Plan activation period is slated for the 5-year period beginning in 2026 and ending in 2030.

The Leviticus 25 Plan – Each participating U.S. citizen will receive a $60,000 deposit into a Family Account (FA) and a $35,000 deposit into a Medical Savings Account (MSA).

Qualification: All U.S. citizens residing in the United States are eligible to participate, contingent upon meeting qualification standards and agreement to specified recapture provisions. Participants (other than ‘custody account’ applicants) must prove stable credit history, stable job history, no recent drug/felony convictions.

These general recapture provisions include:

- Waiving all federal income tax refunds for a period of 5 years.

- Waiving benefits from income security programs, select benefits from means-tested welfare programs, SSI, and SSDI for a period of 5 years.

- Enrollees in the Medicare, Medicaid, VA Healthcare system, Federal Employees Health Benefits (FEHB), and TRICARE will be subject to a $7,000 deductible for primary care and outpatient services annually for a period of 5 years. (See full plan for more details)

The Leviticus 25 Plan generates $37.303 billion federal budget surpluses annually during each of its first five years of activation (2027-2031), and pays for itself entirely over a 10-15 year period.

………………………………….

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$95,000 per U.S. citizen – Leviticus 25 Plan 2026 (34114 downloads )

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}