Federal bank regulatory agencies have finalized a rule to modify the Enhanced Supplementary Leverage Ratio (eSLR) standards, effective April 1, 2026 (with optional early adoption on January 1, 2026). The final rule lowers capital requirements for large U.S. banks (GSIBs), reducing the fixed 2% eSLR buffer to a variable amount equal to 50% of a bank’s Method 1 GSIB surcharge, which frees up balance sheet capacity and acts as a complement to strategies aimed at increasing bank participation in low-risk activities, such as Treasury market intermediation.

…………………….

AI Overview

Key Details of the Final Rule:

- Effective Date: April 1, 2026, with an option for early adoption on January 1, 2026.

- Targeted Entities: U.S. Global Systemically Important Bank holding companies (GSIBs) and their subsidiary depository institutions.

- Buffer Reduction: The eSLR buffer for covered depository institutions is capped at 1% above the minimum 3% leverage ratio, rather than the previous 2% buffer, according to Federal Register (.gov) and Office of the Comptroller of the Currency (OCC) (.gov).

- Purpose: To reduce the punitive capital charges on low-risk activities, such as U.S. Treasury market intermediation, and adjust capital standards based on systemic risk, according to Federal Reserve Board (.gov) and JD Supra.

- Impact: The changes are expected to lower funding costs and reduce Tier 1 capital requirements for holding companies by an estimated $13 billion, according to Federal Deposit Insurance Corporation (FDIC) (.gov) and JD Supra.

A Rule by the Comptroller of the Currency, the Federal Reserve System, and the Federal Deposit Insurance Corporation on 12/01/2025

_____________________________ …

The Leviticus 25 Plan would be a perfect complement to this new regulatory change in the Enhanced Supplemental Leverage Ratio (eSLR) for banks.

This regulatory change alone will be “bullish catalyst for treasuries” … allowing “banks to hold more Treasuries on their balance sheets without needing to hold additional capital against them, freeing up the capacity for banks to participate more actively in the Treasury market.” (The Bear Traps Report, Dec 20, 2024)

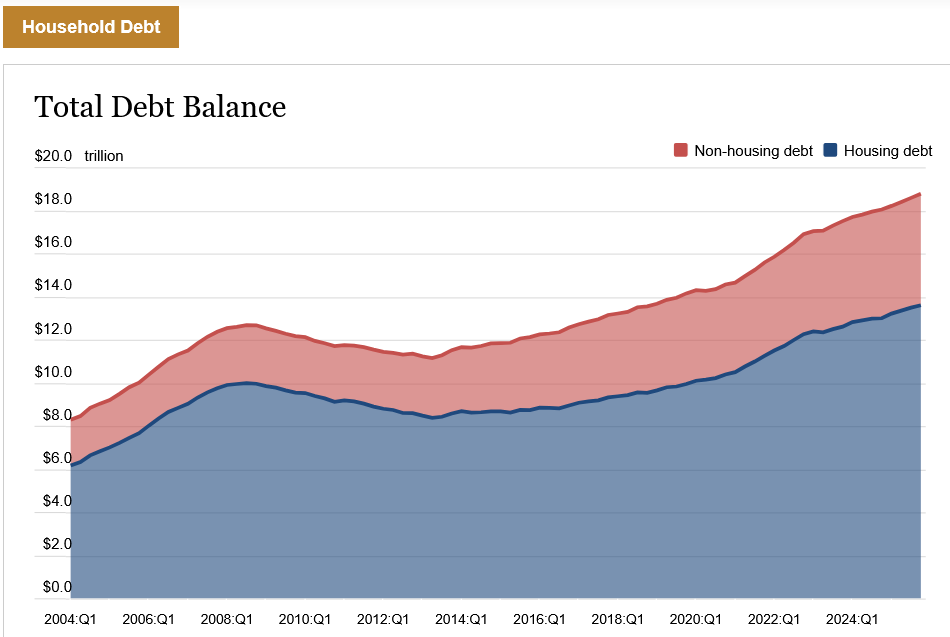

The Leviticus 25 Plan, through the satisfaction of private sector debt (mortgage debt, student loan debt, household debt, auto loans, credit card debt), would provide a powerful additional enhancement of the eSLR change, with trillions of new dollars flowing into the banking system. This synergism would allow GSIBs (global systemically important bank holding companies) even greater treasury auction purchasing power, with increased competitive bidding, lower interest rates, and long-term strength and stability for the U.S. Dollar.

The Leviticus 25 Plan would allow the Fed to adjust interest rates in response to price discovery and free market dynamics, rather than reacting to complex statistical evaluations and timing models, not to mention often intense political pressures.

Occasional adjustments over the course of time toward higher rates, to cool sporadic excesses and speculation within the economy, would decrease the likelihood of new ‘bubbles’ popping up in financial markets. It would be much better tolerated in this new low-debt environment, and it would allow savers to earn millions of dollars in additional interest on their savings.

The Leviticus 25 Plan’s massive public and private debt elimination dynamic will immediately:

1) Generate $37.303 billion federal budget surpluses annually during its first five years of activation (2027-2031), it will pay for itself entirely over the succeeding 10-15 year period, and contribute highly favorable budget gains for state and local government entities;

2) Lower short-term and long-term interest rates;

3) Reduce fraud and waste across many of government’s social insurance sectors;

4) Restore real financial security for millions of American families, rekindle the spirit of self-reliance, and scale back out-of-control government entitlement spending;

5) And generate a long-term economic growth cycle that would benefit all Americans, most notably the 33.2 million small businesses across the U.S..2) Lower short-term and long-term interest rates;

The Leviticus 25 Plan – the most powerful decentralizing economic acceleration plan in the world – is loaded up and ready to launch.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$95,000 per U.S. citizen – Leviticus 25 Plan 2027 (48914 downloads )

{kind=link}

{kind=link}