“You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete. –R. Buckminster Fuller

……………………………..

How Expanded Obamacare Made Premiums Spiral, Americans Dependent

ZeroHedge, Jan 16, 2026 – Authored by Lawrence Wilson and Sylvia Xu via The Epoch Times,

Excerpts:

Congress responded to the COVID-19 pandemic by passing the American Rescue Plan Act in early 2021. This $1.9 trillion spending bill was intended to provide relief and spark an economic recovery.

Among other provisions, the law expanded the availability of government-subsidized health care through the Obamacare Marketplace to help low- to middle-income people maintain health coverage until the economy normalized.

The measure brought millions of middle-class Americans into Obamacare, but had the unintended consequence of making many of them dependent on government aid.

The law also introduced temporary, enhanced subsidies, which raised Obamacare premiums, some observers say.

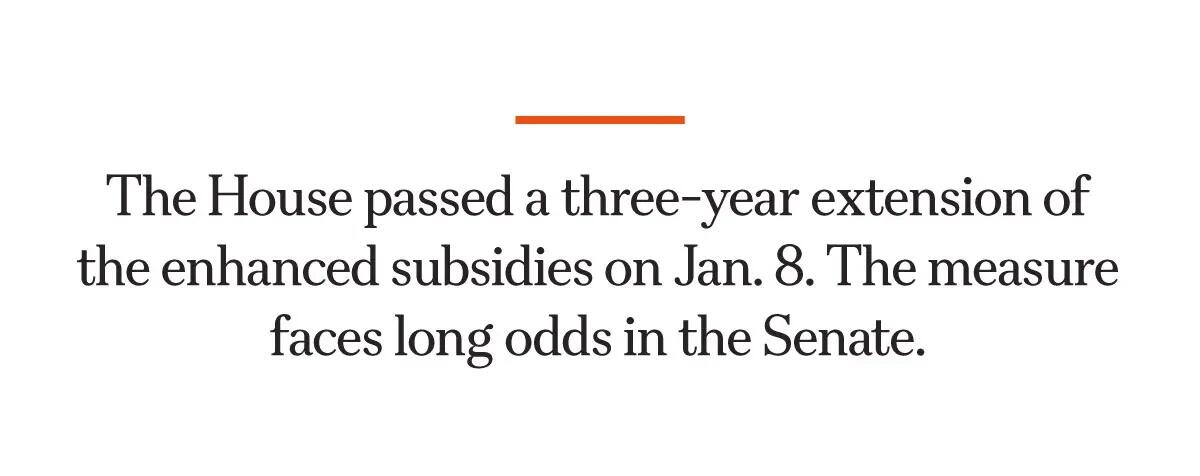

Though the enhanced subsidies expired on Dec. 31, 2025, Congress continues to debate their possible reinstatement.

…………………

During the pandemic, Congress created subsidies that had no income cap. These enhanced subsidies also lowered enrollees’ affordability cap—the maximum amount a customer would pay out of pocket for a monthly premium.

Under the enhanced subsidies, introduced in 2021, no enrollee would spend more than 8.5 percent of their monthly income on premiums. Some would pay no more than 6 percent, others 4 percent or 2 percent, and some would pay nothing.

Enrollment boomed, jumping from 11.4 million to 14.5 million in two years. By 2025, enrollment had doubled from its pre-pandemic level, topping 24 million, according to data from health research organization KFF.

The enhanced subsidies were set to expire in 2022, allowing just enough time to get people back to work.

But when the pandemic ended, the enhanced subsidies remained.

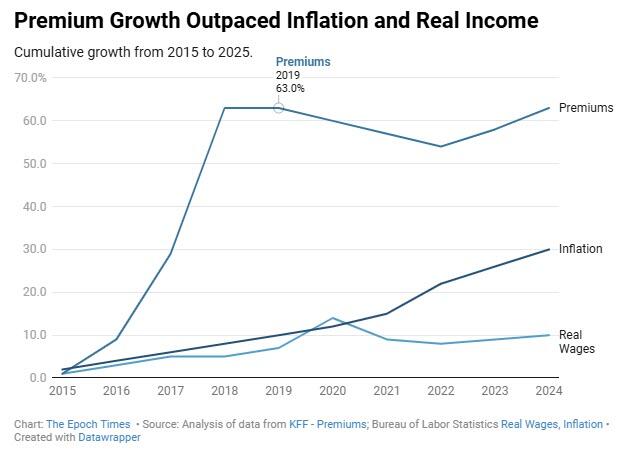

Premiums Increased, Wages Didn’t – Health insurance premiums increased dramatically during Obamacare’s first five years. The average individual premium for a 40-year-old went up at least 75 percent, according to data reported by KFF.

Prices soared in commercial markets, too, where the cost of individual premiums rose about 120 percent from 2013 to 2019, according to The Heritage Foundation.

Obamacare prices leveled out before the pandemic hit and from 2020 to 2022, which includes the first two years of enhanced subsidies, prices dropped 5 percent, according to data reported by KFF.

But in 2022, the year the subsidies were set to end, inflation was on the rise, peaking at more than 9 percent by midyear, according to the Bureau of Labor Statistics.

Economists broadly agree that this was an unintended consequence of American Rescue Plan spending. The rising prices were “the product of easy fiscal and monetary policies, excess savings accumulated during the pandemic, and the reopening of locked-down economies,” Ben Bernanke, former chairman of the Federal Reserve, wrote in a co-authored assessment for Brookings.

Congress responded by spending even more money. The Inflation Reduction Act, passed in August 2022, would pump another $1.2 trillion into the economy within a decade, the Cato Institute estimated. That included a three-year extension of the enhanced subsidies.

Obamacare premiums shot back up, according to data reported by KFF, rising more than 13 percent in three years.

…………………………..

“The [Affordable Care Act] subsidy structure is itself inflationary—driving up health care prices and total premiums,” said Mark Howell and Brian Blase of the think tank Paragon Health Institute. “As Congress considers the future of the COVID Credits . . . it must confront the reality that the [Affordable Care Act] made coverage far less affordable.”

That reality was largely hidden from many who received the enhanced subsidies because their out-of-pocket premium payments were capped based on income. Price hikes above that cap were paid by taxpayers, which meant the enhanced subsidies were now even more important for people with modest incomes.

………………………………..

There has been no dispute among lawmakers that the enhanced subsidies have been a boon to consumers.

The average Obamacare premium for 2025 was $619 per month, of which subsidies covered more than $500. More than 10 million enrollees, 46 percent of those receiving aid, paid $10 or less per month out of pocket for premiums.

About 8 million paid $0, according to Brookings.

That’s exactly the problem, according to some analysts, because the possibility of enrolling large numbers of people who would never receive a bill created a ripe opportunity for fraud.

Many people were enrolled in the program without their knowledge by unscrupulous insurance brokers, Blase alleges, prompting the federal government to send a commission check to them—and premium payments to an insurance company.

These phantom enrollees are detected in part by their lack of activity once enrolled, Blase said.

“In 2024, nearly 12 million enrollees did not use their plan a single time—up from fewer than 4 million in 2021,” Blase told the House Judiciary Committee on Dec. 10.

Overall, 35 percent of all exchange enrollees never used their plan, and 40 percent of fully subsidized enrollees did not have a single claim, which Blase said is double the rate in both the commercial market and pre-pandemic Obamacare.

America’s Health Insurance Providers, the trade association for health insurance companies, disputed that claim.

“A ‘no-claims’ year is evidence that a consumer stayed healthy or only had a few months of coverage—not that taxpayer money was misdirected or that their policy was illegitimate,” the group said in an Aug. 18 statement.

Yet in December 2025, the Government Accountability Office provided evidence of enrollment fraud in Obamacare that suggests fake accounts are being created.

Investigators were able to enroll 20 nonexistent identities in Obamacare in 2024 by using Social Security numbers that had never been issued to any person and other easily created counterfeit documents.

Of the 20 false enrollments, 18 were still active in September 2025, costing taxpayers more than $10,000 per month.

Investigators also found 26,000 accounts that received subsidies in 2023 based on Social Security numbers that matched records in the Social Security Administration’s death file.

More than 7,000 Social Security numbers belonged to people who were reported dead before enrolling in Obamacare, and 19,000 Social Security numbers matched death data by number but not name and address, indicating that false identities may have been created for enrollment.

Taxpayers paid more than $94 million in subsidies for one year based on those numbers.

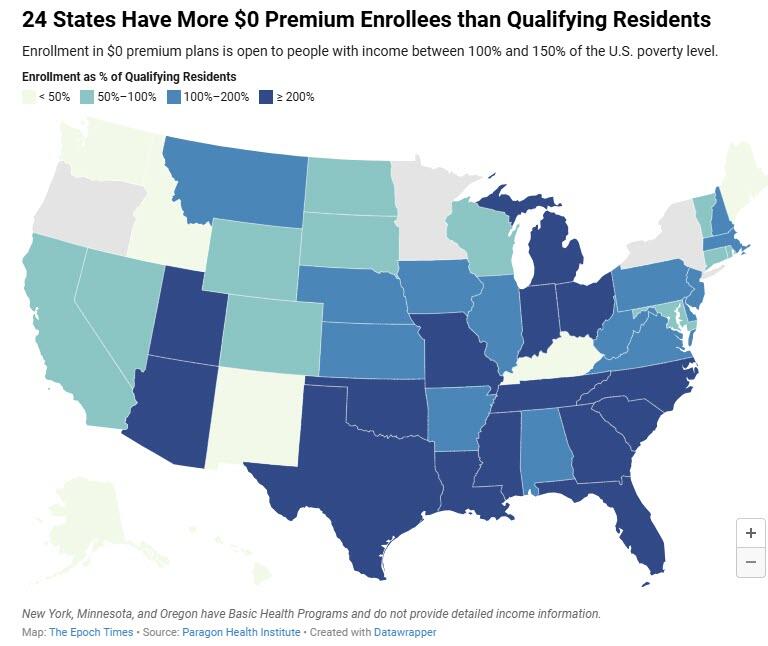

Another indication of fraud is the number of states where enrollment in Obamacare plans with a $0 premium is unreasonably high compared to the number with a qualifying income.

Twenty-four states have more Obamacare enrollees claiming incomes between 100 percent and 150 percent of the federal poverty level than there are people living in the state with that income, according to data from the U.S. Census Bureau.

The problem appears worse in states that have not adopted expanded Medicaid, which would have increased Medicaid eligibility to 138 percent of the federal poverty level.

Obamacare customers are automatically re-enrolled each year, so a fictitious account would continue to generate fraudulent commissions and wasteful insurance payments until detected.

Fraudulent enrollment costs up to $20 billion per year, according to Paragon Health Institute.

Making Health Care Affordable – The enhanced subsidies expired on Dec. 31, 2025. Congressional Republicans and Democrats continue to agree that the U.S. health care system has become unaffordable and want to address the problem. They differ in approach.

Democrats generally favor government intervention in the system, as in the case of Obamacare, where taxpayers pitch in to cover rising costs.

The Senate in December 2025 rejected a proposal to make the enhanced subsidies permanent. House Minority Leader Hakeem Jeffries (D-N.Y.) said at a press conference on Jan. 5 that his party continues to seek an extension of the subsidies “to protect the health care of tens of millions of … everyday Americans, middle-class Americans and working class Americans.”

Without the subsidies, Jeffries said, some consumers would face cost increases of up to $2,000 or more per month.

Republicans generally favor using the power of government to create marketplace competition. Senate Republicans recently presented a plan to provide dedicated funds directly to consumers, which they could use to shop for health care. That plan, too, was rejected by the Senate.

Sen. John Thune (R-S.D.), the Senate majority leader, addressed the differing philosophies in a Dec. 16, 2025, press conference.

“If [Democrats are] willing to accept changes that actually would put more power and control and resources in the hands of the American people, and less of that in the pockets of the insurance companies, I think there’s a path forward,” he said.

President Donald Trump has said he would veto any extension of Obamacare subsidies that came to his desk.

_____________________________________

To Sen. John Thune:

Main Street America Republicans have the plan that “would [indeed] put more power and control and resources in the hands of the American people, and less in the pockets of the insurance companies.”

It is a plan that will overwhelmingly win over the hearts and minds of U.S. citizen voters, and get America back on track as a world economic leader.

The Leviticus 25 Plan will reestablish a strong, market-based, citizen-centered health care system in America.

• Medicare Part D Prescription Drug Benefit – A Dynamic New Funding Model: The Leviticus 25 Plan.

• Pharmacy Closures – PBM Market Power Abuse. Problem Solved: The Leviticus 25 Plan

• World Class Health Care Solved: The Leviticus 25 Plan

• A Look Back: ObamaCare Administrative costs “shocking” – The Hill

………………………..

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$95,000 per U.S. citizen – Leviticus 25 Plan 2026 (44153 downloads )

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}