“It is true that the virtues which are less esteemed and practiced now – independence, self-reliance, and the willingness to bear risks, the readiness to back one’s own conviction against a majority, and the willingness to voluntary cooperation with one’s neighbors – are essentially those on which the of an individualist society rests. Collectivism has nothing to put in their place, and in so far as it already has destroyed then it has left a void filled by nothing but the demand for obedience and the compulsion of the individual to what is collectively decided to be good.” – Friedrich Hayek, The Road to Serfdom

……………………………………………………………..

The Leviticus 25 Plan re-establishes family and societal virtues which have been eroded through government encroachment and socialist-driven central planning – in America and elsewhere around the world.

The Leviticus 25 Plan – grants direct liquidity access to American families – the very same access to liquidity which was provided to the likes of Morgan Stanley, Citigroup, Bank of America Corp, Goldman Sachs, JP Morgan Chase, Merrill Lynch, Wells Fargo, Deutsch Bank, UBS AG, Royal Bank of Scotland, Plc, State Street, Barclays,and many, many others.

The primary goal of The Plan is debt elimination and the restoration of financial health and economic liberty for American families.

Imagine a family of four paying off their mortgage, car loans, credit card debt – and having additional on-hand liquidity for direct allocation for routine medical expenses.

The financial security benefits of all qualifying American families would be incalculable:

Financial stress relief – quality of life improvements – general living conditions, nutrition.

Working mothers desiring to spend more time with their children would be able scale back their outside employment hours or become full-time stay-at-home mothers.

Financial self-reliance at family level – reduced dependence on social welfare and charity programs.

Re-establishment of normal, positive incentives for work, enterprise, innovation, achievements.

Improved credit status for working Americans.

Improved access to primary health care.

Improved employment opportunities.

Significant potential for crime reduction.

……………………………………………………………………………….

There isno government-directed economic strategy that can provide even a fraction of these types of benefits, direct to America’s citizens.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The Leviticus 25 Plan – An Economic Acceleration Plan for America

There is precisely one plan with the raw power to clean this mess up and restore financial security to millions of American families. The Leviticus 25 Plan.

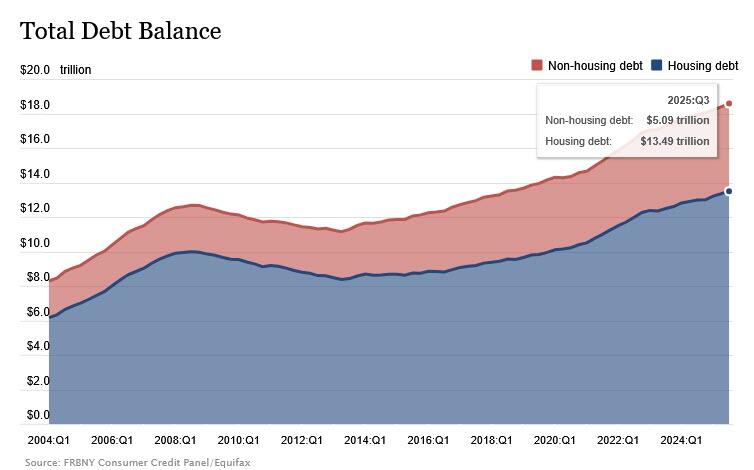

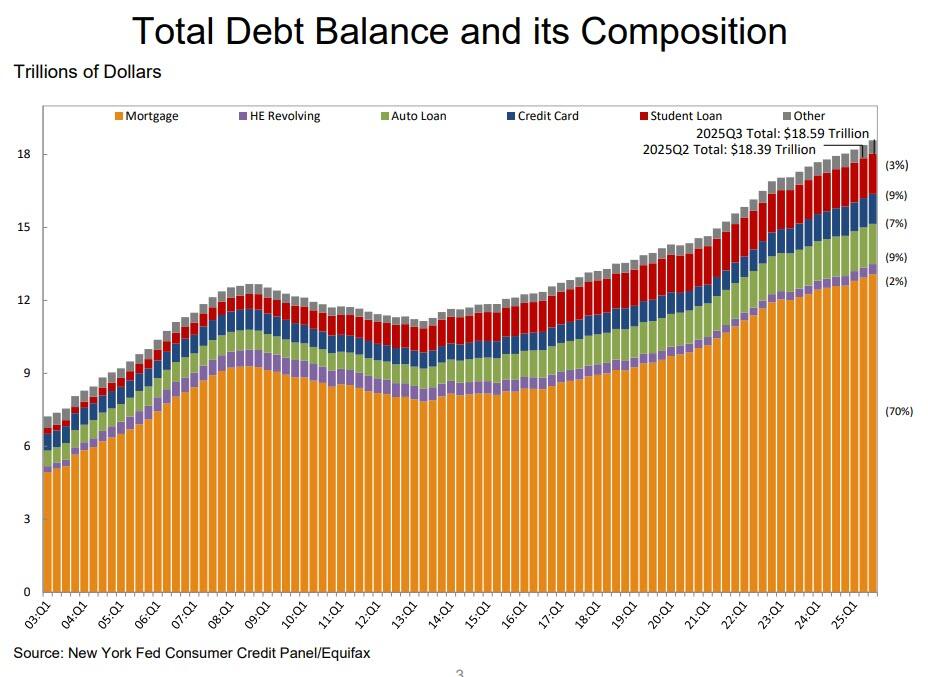

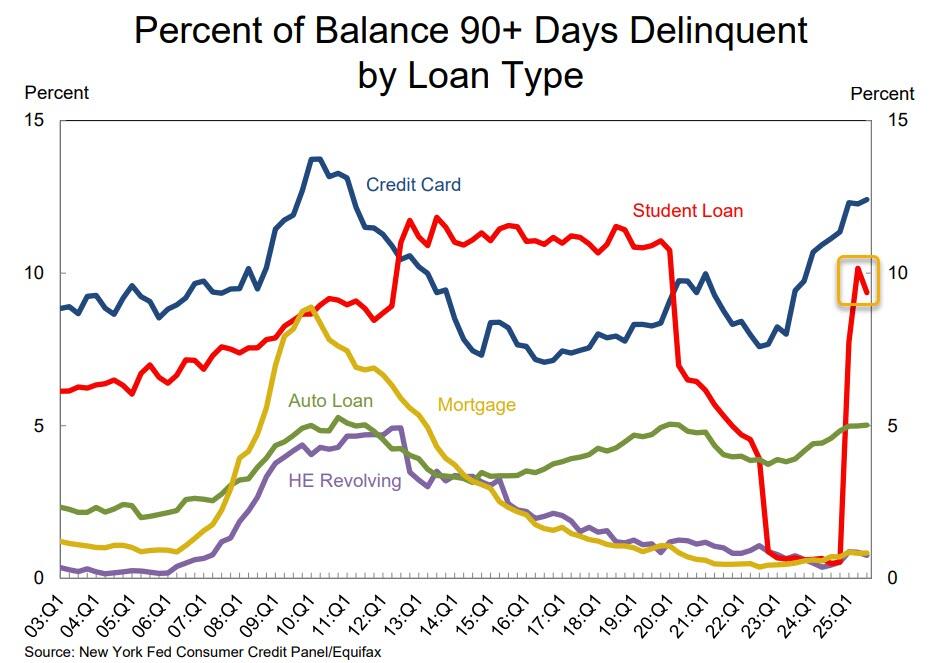

The NY Fed published its Quarterly Report on Household Debt and Credit.

Surprising exactly no-one, the report showed that total household debt increased by $197 billion (1%) in Q3 2025, to a new record high of $18.59 trillion. split between $13.5 trillion in housing debt and $5.1 trillion in non-housing debt.

“Household debt balances are growing at a moderate pace, with delinquency rates stabilizing,” said Donghoon Lee, Economic Research Advisor at the New York Fed. “The relatively low mortgage delinquency rates reflect the housing market’s resilience, driven by ample home equity and tight underwriting standards.”

Details:

Mortgage balances grew by $137 billion in the third quarter and totaled $13.07 trillion at the end of September 2025.

Mortgage delinquency rate rose to 0.83% from 0.82% prior quarter

Credit card balances rose by $24 billion from the previous quarter and stood at $1.23 trillion.

Delinquency rate at 12.41%, highest since 2011

Auto loan balances held steady at $1.66 trillion.

Home equity line of credit (HELOC) balances rose by $11 billion to $422 billion.

Student loan balances rose by $15 billion and stood at $1.65 trillion.

………

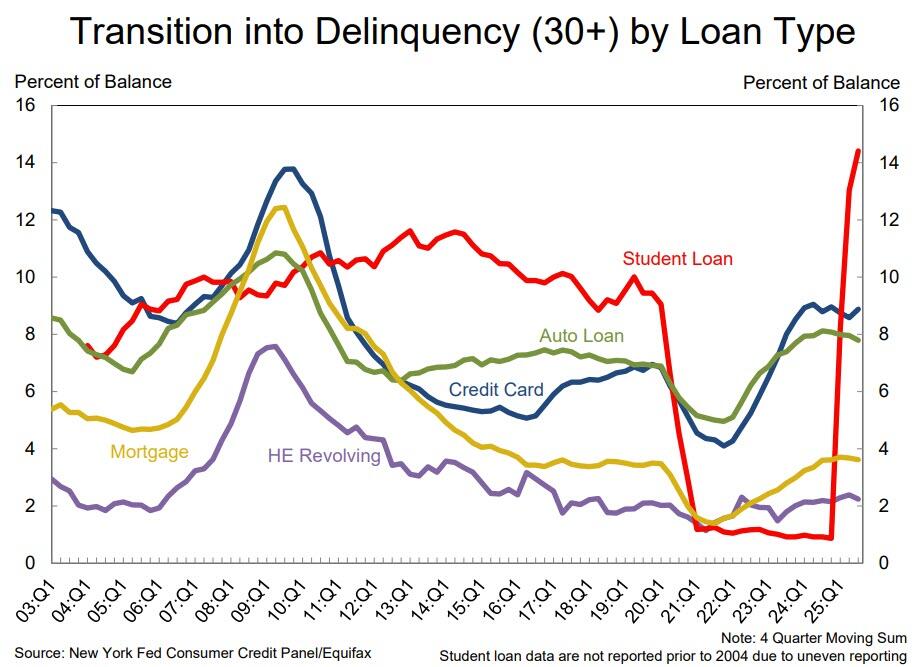

Of course, with rising debt, come rising delinquencies, and in the case of student debt, absolutely explosive ones.

As the NY Fed writes, aggregate delinquency rates remained elevated in Q3 2025, with 4.5% of outstanding debt in some stage of delinquency. Transitions into early delinquency were mixed with credit card debt and student loans increasing, while all other debt types saw decreases.

…. and serious delinquency (90+ days) increased across all debt types.

………………….

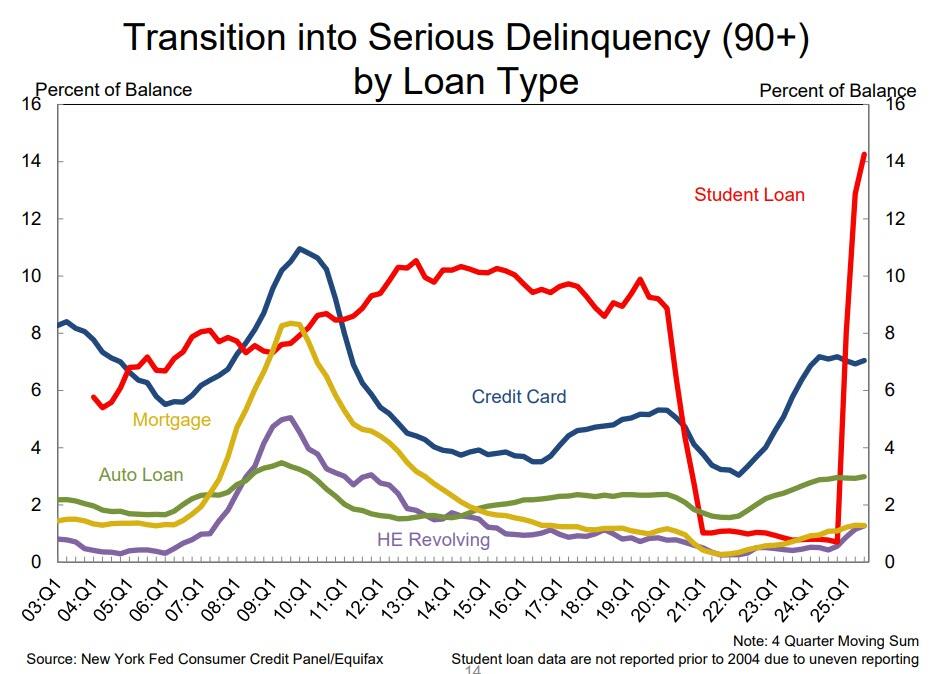

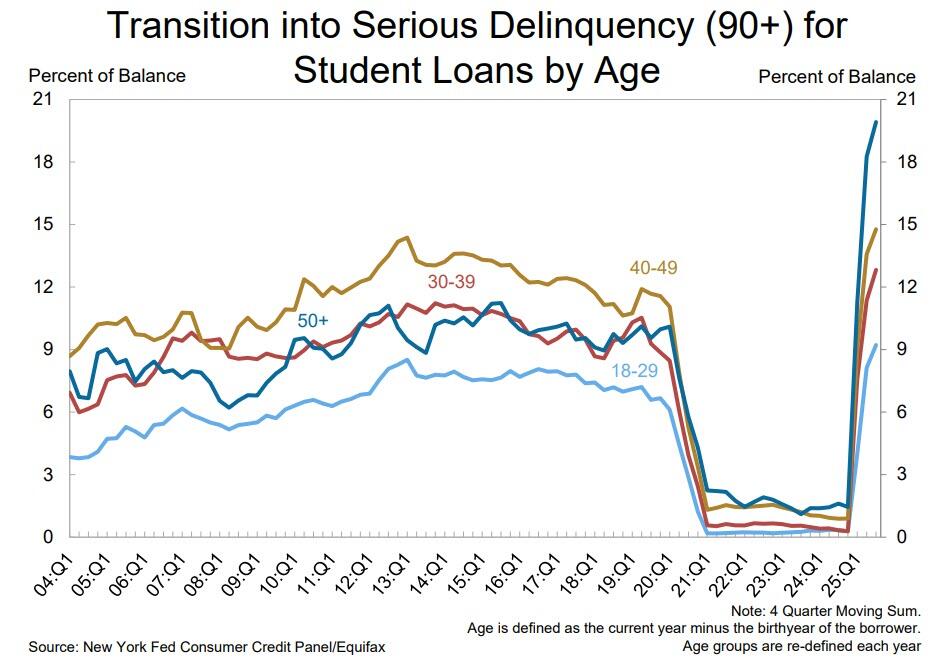

Taking a closer look at the ground zero of the current consumption crisis, namely student Loans, where outstanding debt stood at $1.65 trillion in Q3 2025.

And the punchline: missed federal student loan payments that were not previously reported to credit bureaus between Q2 2020 and Q4 2024 are now appearing in credit reports. Consequently, student loan delinquency rates have continued to surge after a sharp rise in the first half of 2025. In Q3 2025, 9.4% of aggregate student debt was reported as 90+ days delinquent or in default, as compared to 7.8% in Q1 2025 and 10.2% in Q2 2025. Also of note in the chart below, the credit card serious delinquency rate is actually creeping up even faster, and hit 12.41%, the highest since 2011.

And the most remarkable observation: over 20% of all student debt by those aged 50 and over (!) is effectively in default (technically it is still delinquent, but if millions haven’t made even a token effort to repay it in 90 days, one can safely classify it as in default).

That’s millions of potential consumers whose credit rating is about to get obliterated and who will not have access to credit cards or other debt forms for a long time.

The Leviticus 25 Plan retargets Fed liquidity flows to grant U.S. citizens the same direct access to liquidity extensions that the Fed and U.S. Treasury so generously provided to very same domestic and foreign financial institutions that precipitated the subprime mortgage debacle and subsequent Great Financial Crisis (2008-2010).

The GFC housing market collapse “wiped out $11 trillion in household wealth.” Over 9 million people lost their jobs, and “at least 10 million people lost their homes due to foreclosure, according to The Los Angeles Times.”

The Leviticus 25 Plan will eliminate trillions of dollars of Household Debt and generate $36.568 trillion federal budget surpluses during each of its first five years of activation (2026-2030).

The Leviticus 25 Plan, in one fell swoop, will effectively resolve the student loan debt crisis in America – while at the sametime providing equal financial security benefits to those who paid off their loans and those who chose to bypass college and enter directly into the work force.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

“The inherent vice of capitalism is the unequal sharing of blessings; the inherent virtue of socialism is the equal sharing of misery.” -Winston Churchill

“Socialism means slavery.” -Lord Acton

“Democracy and socialism have nothing in common, but one word, equality. But notice the difference: while democracy seeks equality in liberty, socialism seeks equality in restraint and servitude.” -Alexis de Tocqueville

Socialism leads to the politicization of society. Hardly anything can be worse for the production of wealth.

Socialism, at least its Marxist version, says its goal is complete equality. The Marxists observe that once you allow private property in the means of production, you allow differences. If I own resource A, then you do not own it and our relationship toward resource A becomes different and unequal. By abolishing private property in the means of production with one stroke, say the Marxists, everyone becomes co-owner of everything. This reflects everyone’s equal standing as a human being.

The reality is much different. Declaring everyone a co-owner of everything only nominally solves differences in ownership. It does not solve the real underlying problem: there remain differences in the power to control what is done with resources.

In capitalism, the person who owns a resource can also control what is done with it. In a socialized economy, this isn’t true because there is no longer any owner. Nonetheless the problem of control remains. Who is going to decide what is to be done with what? Under socialism, there is only one way: people settle their disagreements over the control of property by superimposing one will upon another. As long as there are differences, people will settle them through political means.

If people want to improve their income under socialism they have to move toward a more highly valued position in the hierarchy of caretakers. That takes political talent.

Under such a system, people will have to spend less time and effort developing their productive skills and more time and effort improving their political talents.

As people shift out of their roles as producers and users of resources, we find that their personalities change. They no longer cultivate the ability to anticipate situations of scarcity to take up productive opportunities, to be aware of technological possibilities, to anticipate changes in consumer demand, and to develop strategies of marketing. They no longer have to be able to initiate, to work, and to respond to the needs of others.

Instead, people develop the ability to assemble public support for their own position and opinion through means of persuasion, demagoguery, and intrigue, through promises, bribes, and threats. Different people rise to the top under socialism than under capitalism. The higher on the socialist hierarchy you look, the more you will find people who are too incompetent to do the job they are supposed to do. It is no hindrance in a caretaker politician’s career to be dumb, indolent, inefficient, and uncaring. He only needs superior political skills. This too contributes to the impoverishment of society.

The United States is not fully socialized, but already we see the disastrous effects of a politicized society as our own politicians continue to encroach on the rights of private property owners. All the impoverishing effects of socialism are with us in the U.S.: reduced levels of investment and saving, the misallocation of resources, the over-utilization and vandalization of factors of production, and the inferior quality of products and services. And these are only tastes of life under total socialism.

_____________________________________

The Leviticus 25 Plan

There is currently one, and only one, comprehensive economic acceleration plan in America that re-targets liquidity flows away from government agencies and corporate middlemen directly to U.S. citizens – to revitalize self-reliance in America and reverse the ‘impoverishing effects of socialism.’

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The Leviticus 25 Plan would lift millions of working-class, tax-paying American families up out of poverty – and eliminate the ever-growing dilemma of food lines and dependence upon government-based food handouts.

Food stamps are set to be paused on Nov. 1 because of the government shutdown.

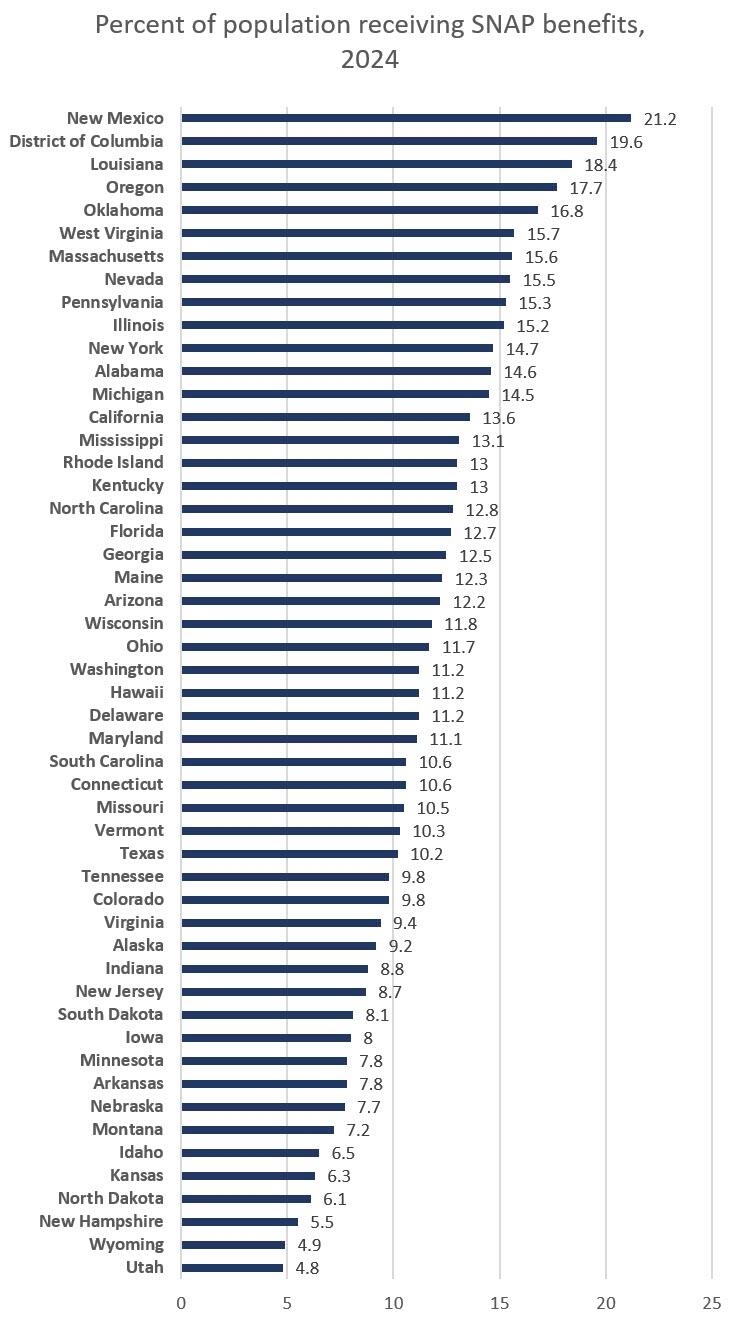

Some 42 million Americans will not receive benefits through the Supplemental Nutrition Assistance Program (SNAP) until Congress approves new funding, according to federal officials, although some states have taken steps to intervene.

Nationwide, the total percentage of the population receiving food stamps can vary significantly by state, and region. Measured state-by-state, we find that more than one in five residents of New Mexico receive food stamps. In Utah, on the other hand, fewer than one in twenty receive food stamps.

………………………………………………………………..…………………

Mercatus Center | GeorgeMason University | May 13, 2025

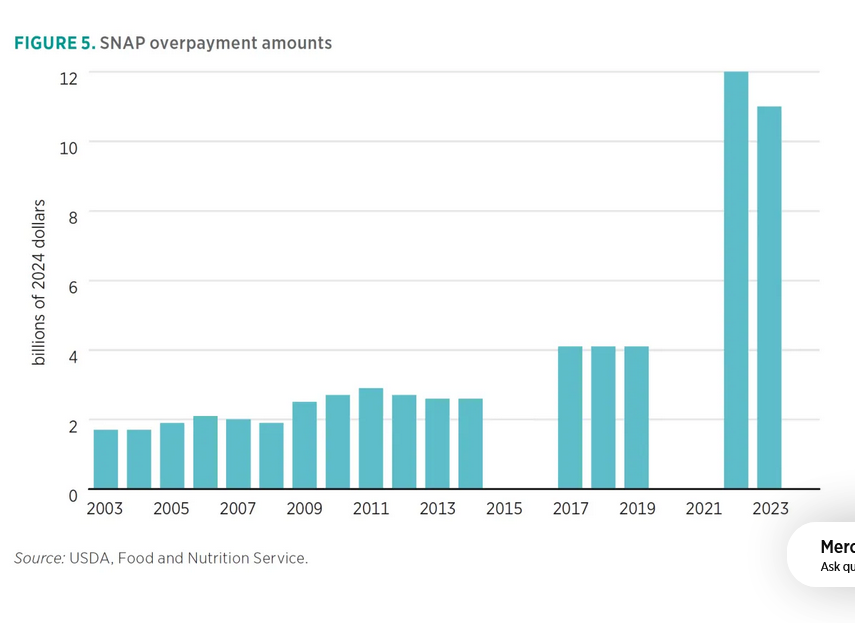

By 2023, the pandemic had pushed the national SNAP program error rate to nearly 12 percent, with overpayments amounting to about 10 percent of that figure. At the state level, overpayment rates were as high as 57 percent for Alaska. Even before the increase in the pandemic-era rates, the national overpayment rate had been rising rapidly: While it was just a little over 2 percent in 2012, the national overpayment rate hit 6 percent in 2019, before the pandemic. In dollar terms, as of December 2024, SNAP overpayments are up to $10 billion per year, and much of this amount is from benefit trafficking, which now costs $1.3 billion annually.

Nonbenefit costs to the federal government

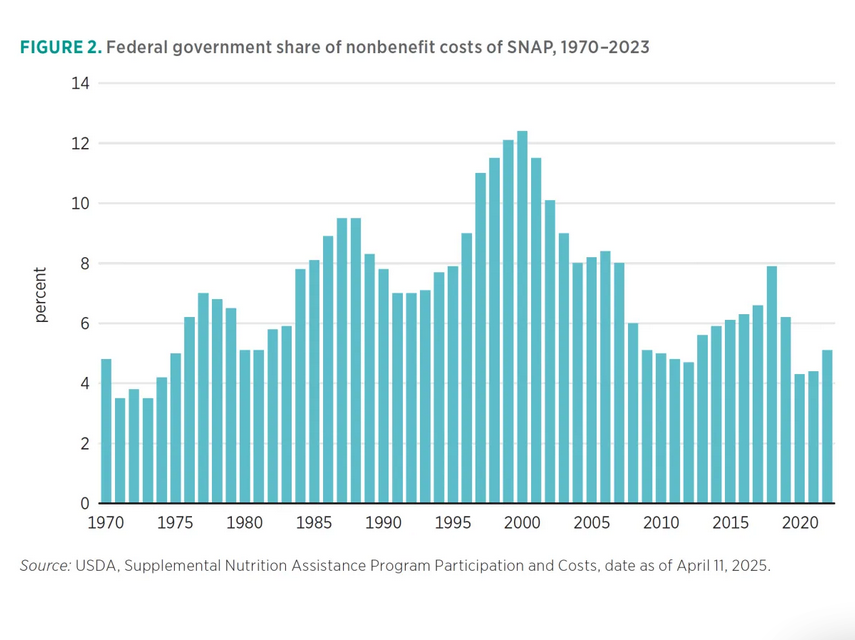

In addition to contributing to state administrative expenses, the federal government covers other, nonbenefit costs associated with SNAP. First, the FNS reviews the states’ administration of the program in accordance with federal requirements. The federal government also supports state expenses for nutrition education programs, employment and training programs, benefit and retailer redemption and monitoring, payment accuracy, electronic benefits transfer (EBT) systems, program evaluation and modernization, program access, and health and nutrition pilot projects.

The share of total federal spending on nonbenefit costs was about $6 billion in FY 2023, or 5 percent of the total costs (see figure 2).[3] SNAP administrative expenses vary quite widely by state.[4] For example, in FY 2016 average administrative expenses varied from $89 per case in Florida to $848 per case in Wyoming. However, there is little understanding of these differences, as this variation does not seem to be explained by economic conditions or caseload levels.

Overpayments have always dominated the program error rate. In 2023, for example, they outpaced underpayments six to one… in FY2023, SNAP overpayments totaled $10.7 billion, but recovery of overpayments was just $389 million, or less than 4 percent.[13]

Despite increased efforts to curtail waste, there has been no evidence of anything but increases in overpayments since FY 2013. Furthermore, there is no comprehensive measure of fraud in the program, but taxpayer dollars are lost whether overpayments are fraudulent or just errors. Because of the high cost of the program, these overpayment rates have certainly cost the government tens of billions of dollars (see figure 5).

SNAP Fraud Trafficking of SNAP benefits Problems specifically related to the use of EBT cards Retailer application fraud Errors and fraud by households Errors and fraud by state agencies

__________________________________________

The vast majority of federal and state entitlement programs, SNAP and TANF in particular, are rife with waste and fraud.

There is one comprehensive economic plan in America with the raw power to wipe out hundreds of billions of dollars in these annual losses – while at the same time lifting millions of U.S. citizens up out of the ranks of poverty.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

A century of central banking and commercial credit has normalized a simple but profound fact: most new money is created when banks make loans. As former U.S. Treasury Secretary Robert B. Anderson put it in 1959, when a bank issues a loan, it credits a deposit that did not exist the moment before; the new deposit is “new money.” In practice, this means the money supply expands primarily through private lending, not public issuance.

That mechanism is turbocharged by fractional-reserve banking and today by capital-based banking rules: banks do not lend out pre-existing savings one-for-one; they expand deposits by creating credit. Interest is attached to that credit, meaning the system requires continual new borrowing to service past borrowing. If credit creation slows materially, defaults rise, asset prices wobble, and political pressure mounts to “stimulate” again. In short, we live inside a treadmill that is far more credit-driven than most civics textbooks admit.

…………………………..

Modern banking’s political leverage grew alongside institutions like the Bank of England and, later, the U.S. Federal Reserve (established in 1913). Whatever the intention of their founders, central banks now sit at the junction of state and finance: they are publicly mandated yet operationally insulated (and privately owned), coordinating liquidity to stabilize the system while commercial banks originate most money-like claims.

This hybrid design has real consequences. It allows a small circle of decision-makers to set the price of money (interest rates), backstop private balance sheets in crises, and influence fiscal choices by making some policies financially easy and others expensive. Former Fed Chair Alan Greenspan once emphasized the institution’s independence; the flip side of that independence is low democratic visibility over choices that shape every mortgage, job market, and public budget.

Beyond national central banks lies the Bank for International Settlements (BIS) in Basel — often called the “central bank of central banks.” Through standards (Basel accords) and coordination, it helps align global banking rules. Critics argue this produces a technocratic layer of control over national economies with little public oversight. Whether one views that as prudent stewardship or as democratic deficit, it underscores a theme: the architecture of money governance is largely opaque to the public it governs.

……………………..

Critics like Roy Madron, John Jopling, and John Scales Avery have argued that this growth-dependency crowds out other goals: equitable distribution, environmental stewardship, and cultural stability. It also explains why mainstream debates often avoid the root structure and instead focus on the speed of the treadmill…

………………….

When money is predominantly debt, interest is not a side note; it is a structural tax on all who need money to transact. Banks, by creating credit, collect streams of interest that compound through the system. Meanwhile, inflation — the dilution of purchasing power — often becomes a necessary byproduct of keeping debt-loads serviceable. In practice, inflation acts as a stealth transfer from savers and wage earners to those closer to the spigot of new money (large financial institutions and asset owners).

This is not an argument to abolish credit; modern economies need flexible financing. It is an argument to name the trade-offs honestly. When we call monetary loosening a “stimulus,” we should also disclose who absorbs the loss in purchasing power and who gains from asset inflation. When we raise rates to “fight inflation,” we should admit the cost in jobs, bankruptcies, and public budgets. Stability is never free; it is reallocated volatility.

…………………..

Beyond national systems lies a web of global coordination — standards, swap lines, and lender-of-last-resort arrangements that knit economies together. Institutions such as the BIS, the IMF, and development banks shape the terms of liquidity and restructuring. Supporters say this is necessary to prevent contagion; critics counter that it allows a transnational financial class to set conditions on democratic societies in moments of maximum vulnerability.

Both views can be true. But whichever side you take, the outcome is similar: creditors hold leverage, and policy follows balance-sheet realities. The deeper the debt and the tighter the markets, the narrower the options for governments and citizens. This is not a conspiracy; it is a design choice we rarely discuss.

………………

Conclusion: Seeing the Machine

If you remember only one thing, let it be this: money is not neutral. How it is created, who controls its issuance, and what claims attach to it determine the shape of our economies and the boundaries of our politics. We can disagree about the best reforms, but we can no longer afford civic illiteracy about the monetary plumbing that governs our lives.

In a healthy society, the architecture of money would be a public conversation, not a specialist’s secret. Until then, the treadmill will keep turning — and those closest to the controls will keep deciding how fast the rest of us must run.

Mark Keenan is a former United Nations technical expert and the author of The Debt Machine: How Private Banks Engineered Global Control and Climate CO₂ Hoax: How Bankers Hijacked the Environment Movement. His work examines how global finance and policy networks shape the modern world behind the scenes.

______________________________________

The Leviticus 25 Plan corrects the imbalances in America’s debt-based money creation by granting millions of hard-working, tax-paying U.S. citizens the same direct liquidity extensions that were so generously provided to major U.S. and foreign banking concerns during the 2008-2010 great financial crisis, and again during the 2021-2023 Covid crisis.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

“Big government means low growth, high taxes, weak real wages, and a persistent productivity drag..”

Solution: There is one economic plan with the raw firepower to reignite economic growth, reduce taxes, generate ‘real wage gains,’ and spur productivity — The Leviticus 25 Plan

A few years ago, The Economist published an issue called “The Triumph of Big Government,” highlighting the rise of government intervention as the main driver of economic recovery and growth. The years of budget and deficit control were over. Mainstream economists hailed the decisive action of governments in developed nations, committed to spending to boost growth and abandoning the old “austerity” principles.

Only a few years later, The Economist publishes an issue titled “The Coming Debt Emergency,” mentioning the enormous deficit and debt problems in France, the United Kingdom, Japan, and the United States.

What happened? How can long-term bond yields rise when central banks are cutting rates? How did government debt lose its place as a reserve asset? Easy. Developed economies’ governments of all colours, from Biden and Sunak to Macron and Ishiba, bought the MMT fallacy that “deficits do not matter” and “sovereign nations can issue all the debt they need without risk.” Virtually all international bodies hailed statism as the global solution. However, in 2022, global central banks and investors started abandoning sovereign debt as a reserve asset and decided to add gold.

Developed nations have surpassed the three limits of indebtedness: the economic, fiscal and inflationary limitations. When more public debt creates lower economic and productivity growth, the economic limit has been surpassed. When interest expenses and deficits continue to rise despite rate cuts and higher taxes, the fiscal limit collapses. Additionally, when governments become addicted to issuing more debt in any part of the cycle, with diminishing investor demand, inflation becomes persistent.

No one really believes developed nations’ governments will control their public finances, and constant tax hikes and excessive regulation have choked the productive economy.

Employment is showing the negative effect of the “triumph of big government”. Bloating government spending may disguise GDP but does not create jobs.

Even as government spending continues to artificially elevate headline GDP figures, global labour markets are showing weakness. According to S&P Global’s October 2025 PMI Bulletin, the global economy continues to show headline growth, but employment growth has stalled, and productivity improvement has declined sharply.

S&P Global’s global composite PMI stood at 52.4 in September, its lowest level in three months. Companies are attempting to manage high taxation and regulatory burdens, resulting in stagnant employment levels and output growth. Employment was broadly flat across both manufacturing and services sectors, a sign of declining confidence and cost-saving across advanced economies.

The eurozone is a key example of how big government destroys employment growth, real wage improvements and investment. The modest improvement in activity comes with a decline of hiring and investment. The United Kingdom’s tax hikes and net zero policies have decimated the industry and obliterated employment growth….

Government spending and persistent inflation bloat nominal growth, while real economic productivity and private labour opportunities deteriorate. The erosion of value-added generated by the productive economy is alarming. Considering that major governments are borrowing heavily to fund what they call stimulus measures, and they refuse to reduce current spending, GDP figures are being inflated by debt-financed public sector demand.

This labour market stagnation highlighted by S&P Global coincides with a significant slowdown in real wage growth. Although headline CPI has eased in most advanced economies, real inflationary pressures are elevated and continue to erode disposable income even using official CPI figures. This situation leads to weak real consumption and worsening demographic trends.

Big government means low growth, high taxes, weak real wages, and a persistent productivity drag. Malinvestment and excessive government intervention are now the norm in major economies. SP Global explains that “the most interest rate–sensitive sectors, such as manufacturing and construction, account for a smaller share of economic activity in advanced economies than in the past.” However, the problem is not just interest rates but rising taxes and insurmountable regulations that dampen activity in high multiplier sectors.

The 2030 agenda, along with the so-called green regulations and net zero policies, has resulted in capital misallocation and distortions in policy. Thus, productivity gains are increasingly limited to digital and financial sectors.

Fiscal expansion now drives most of the headline economic activity in developed nations with negative side effects everywhere. The debt service burden is crowding out productive expenditure, high taxes limit investment and hiring, and regulation makes the economy stagnant. As sovereign yields climb, countries like France and the UK are already facing “vicious cycles” of slower growth and higher financing costs.

The reader may think that this is the result of incompetence and malinvestment, and if governments spent wisely and invested in productive activities, all would be fine. No. Central planning never works, even if there are some allegedly beneficial intentions. Keynesianism and social democracy always fail. Why are governments not worried? Because they can raise your taxes and present themselves as the solution.

The solution is simple. Less government means more growth.

___________________________________

Again: “Big government means low growth, high taxes, weak real wages, and a persistent productivity drag..”

“…constant tax hikes and excessive regulation have choked the productive economy.”

“The solution is simple. Less government means more growth.“

………………………………..

And that solution is here – loaded up and ready to launch…

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

“Individualism, in contrast to socialism and all other forms of totalitarianism, is based on the respect of Christianity for the individual man and the belief that it is desirable that men should be free to develop their own individual gifts and bents. This philosophy, first fully developed during the Renaissance, grew and spread into what we know as Western civilization. The general direction of social development was one of freeing the individual from the ties which bound him in feudal society.” -F.A. Hayek, Nobel Prize, Economic Sciences

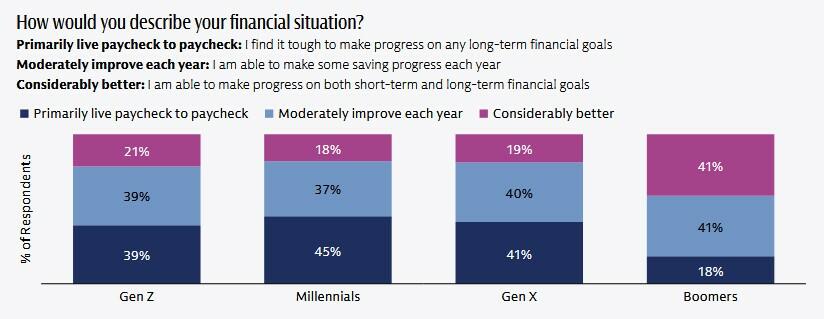

“According to a Goldman survey published earlier this month, around 40% of Americans under the age of boomer report living paycheck to paycheck as inflation continues to erode purchasing power.”

America needs a family-centered financial security reset for hard-working, tax-paying U.S. citizens. Main Street America Republicans have just such a plan.

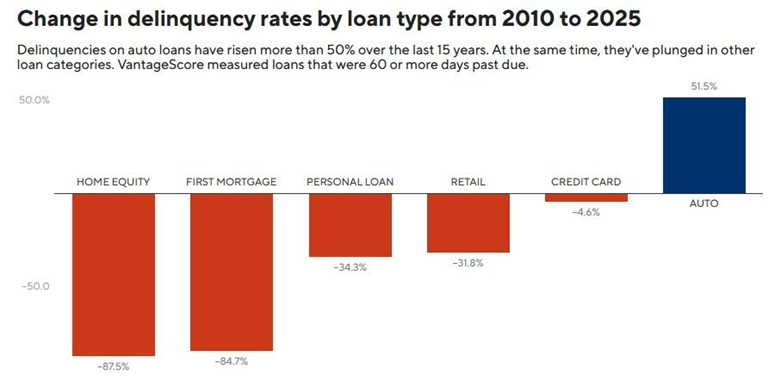

On Friday we noted thatauto loan delinquencies among low-tier consumers have surged 50% since 2010, as new vehicle prices have spiked over 25% since 2019 and 20% of borrowers forking over at least $1,000 per month for their depreciating asset (at 9% APR, no less).

And so it makes perfect sense that with over 100 million auto loans in America, the number of cars being repossessed is approaching records.

According to data from the Recovery Database Network (RDN), there have been over 7.5 million repossession assignments in the United States so far this year – meaning, authorizations given to an agency to recover a vehicle on behalf of a lender. This figure is on track to exceed 10.5 million by the end of the year. Of note, an assignment =/= a repossession, as repo men aren’t always successful.

Yet despite recovery ratios having fallen in recent years, over three million cars could be repossessed this year, a level not seen since 2009.

Paycheck to Paycheck

According to a Goldman survey published earlier this month, around 40% of Americans under the age of boomer report living paycheck to paycheck as inflation continues to erode purchasing power.

For those living primarily paycheck to paycheck, the top issue cited by 87% of those asked was “Too many monthly financial expenses” – like an auto loan. In second place is financial hardship (81%) such as home repairs, followed by credit card debt (77%).

Meanwhile, Fitch reports that 6.43 percent of subprime auto loans were at least 60 days past due in August, while Cox Automotive reported last week that the average transaction price for a new vehicle hit $50,000 last month – the highest level ever.

“Auto finance is at a breaking point, as Americans owe over $1.66 trillion in auto debt. Delinquencies, defaults, and repossessions have shot up in recent years and look alarmingly similar to trends that were apparent before the Great Recession,” wrote the Consumer Federation of America, a nonprofit advocacy group.

“Cars are more expensive than ever, due in part to economic factors, but also due to the fraught experience of buying and financing a car. Dealers and lenders have long engaged in deceptive and predatory practices that jack up prices for car buyers in order to line their pockets.”

_____________________________

Main Street America Republicans currently have the one and only blockbusting plan to reset the consumer debt cycle:

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Rising government spending and public debt create economic stagnation and declining living standards. Many citizens believe that the state will give them prosperity and equality. However, the state only makes paper promises by issuing debt, creating a constantly depreciated currency. Taxpayers are constantly expropriated, while the recipients of subsidies become a dependent subclass. Who wins? Bureaucrats.

Deficit spending is not a tool for growth. It erodes prosperity, creates persistent secular stagnation, real wage growth decline, and poor productivity growth.

High public spending and government debt falsely inflate GDP through government outlays while, in most cases, masking a private-sector recession underneath. GDP is easily manipulated by increasing government spending and changing the calculation of GDP deflators.

The state issues debt, a form of currency, and establishes a system that continuously suffocates the productive sector. In effect, GDP and CPI serve as measures of economic strength that obscure the imbalances created by the state; GDP overstates real growth by incorporating government spending financed by debt, while CPI, like the GDP deflator, underestimates the currency’s loss of purchasing power.

Major economies face a hidden real recession for households and small businesses using “robust” headline figures bloated by ever-rising government debt. Every new dollar of debt now generates less than sixty cents of nominal GDP in the U.S. However, when we look at countries like Japan, France, the UK or Germany, the multiplier effect of new government debt is either nonexistent or negative. The consequences are evident: true productive economic expansion is hurt by rising taxes, regulatory burdens, and inflation, which reduce incentives for private investment and innovation.

Statism creates enormous disincentives for productive investment and promotes malinvestment and the constant transfer of wealth from the productive sectors to the government. Governments finance their ever-expanding budgets in privileged conditions, creating a crowding out of the private sector that suffers the consequences of persistent inflation and raising taxes.

Remember that high taxes are not a tool to reduce debt but to justify it.….

…Persistent inflation is the systemic result of chronic government overspending and central bank easing to sustain sovereign debt bubbles…

Capitalism and social media do not cause inequality and discontent. Governments create inequality in its most severe form, which arises from political favouritism.

Artificial creation of currency is never neutral. It disproportionately benefits the first recipient of new money and governments and hurts the last recipients, wages, and deposit savings.

Workers and the middle class cannot protect themselves against the stealth expropriation of the economy…

By manipulating interest rates and maintaining elevated public outlays, governments create a stealthy nationalisation of the economy and a slow-motion crisis. This leads to a gradual decline in both purchasing power and living standards.

The solution is to diminish the power of the state, promote sound money, strengthen the private sector, favour entrepreneurship, and make systematic cuts to government spending.… Without decisive spending restraint, citizens remain trapped in a vicious cycle of dependency, currency devaluation, and impoverishment.

Rising government spending and public debt do not deliver productive growth. They create stagnation.

_________________________________

The Leviticus 25 Plan is America’s one and only decentralizing, debt-busting, government-shrinking economic revitalization plan – with the raw power to get America back on top as a legitimate economic superpower and true leader of the free world.

The Leviticus 25 Plan will ‘lift millions of working Americans up out of poverty’… ‘strengthen the private sector’…. ‘promote sound money’… deliver long-term economic growth… and restore economic liberty.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

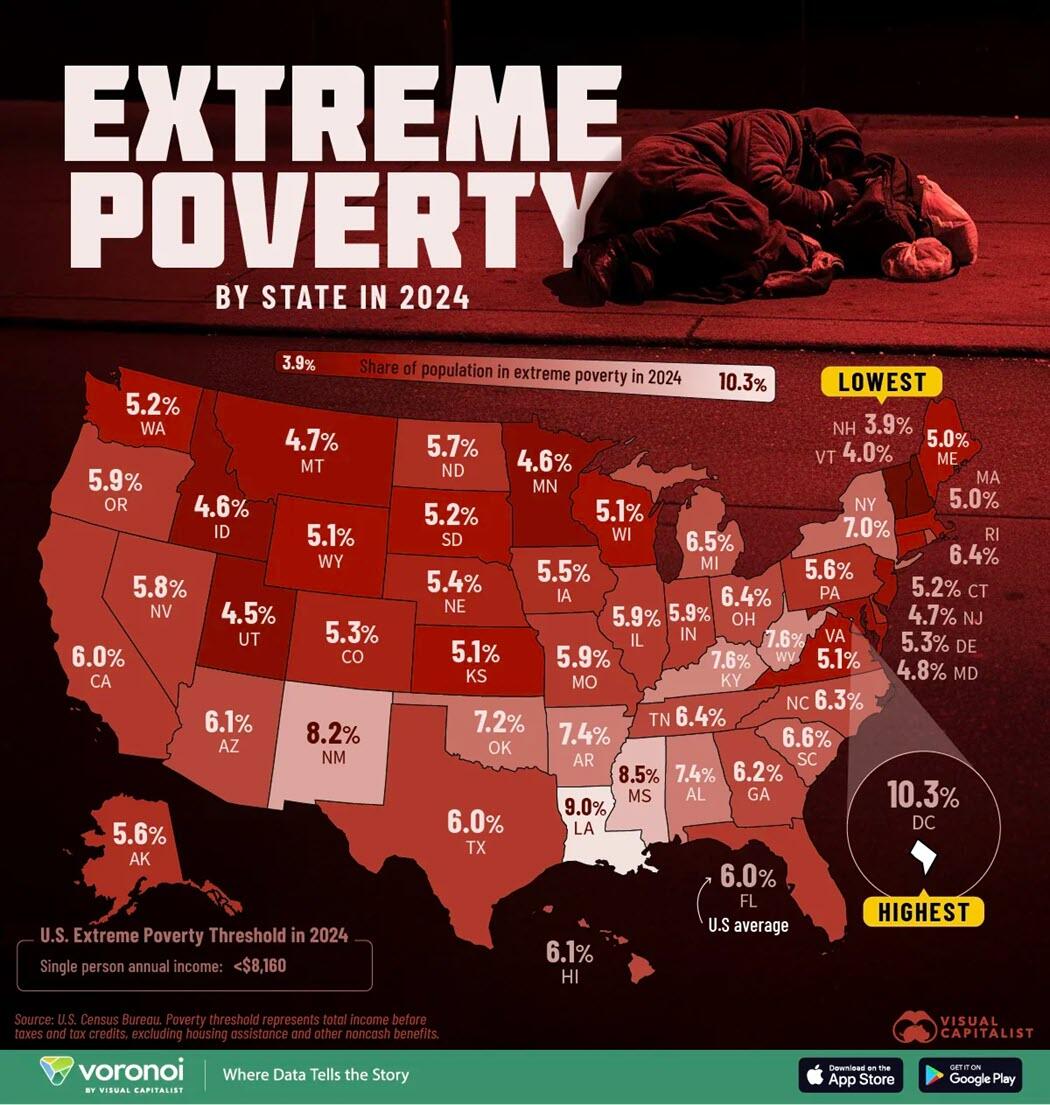

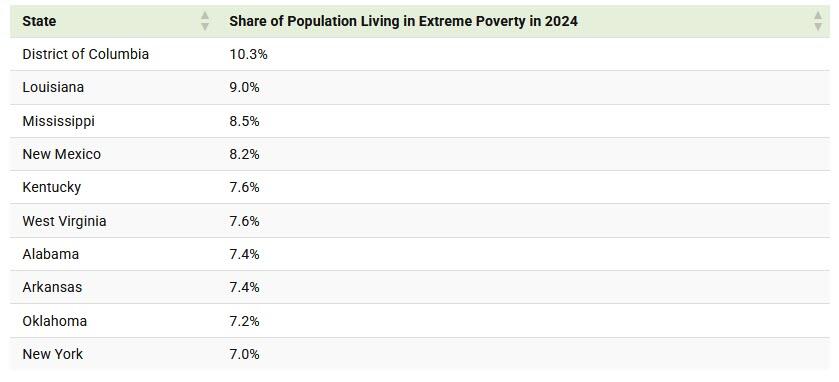

In 2024, 6% of the U.S. population lived in extreme poverty, equal to 20.4 million people.

While there are different definitions of extreme poverty, this is represented as those earning less than $8,160 in annual income, or half of the poverty line. As the federal budget makes cuts to food assistance and healthcare, levels of extreme poverty run the risk of worsening even further.

This graphic, viaVisual Capitalist’s Dorothy Neufeld, shows the share of each state living in extreme poverty in 2024, based on data from the U.S. Census Bureau.

Washington D.C. Has the Highest Level of Extreme Poverty

Last year, more than one in 10 residents of the nation’s capital lived in extreme poverty.

Going further, economic hardship disproportionately impacts people of color in Washington D.C., with one in three black children living in poverty between 2019 and 2023, on average.

As we can see, Southern states also rank among the most impoverished. In Louisiana, 9% of residents live in extreme poverty, and on average, 18.9% lived below the poverty line between 2021 and 2023.

Meanwhile, 7% of New York’s population are extremely impoverished, equal to an estimated 1.4 million people.

On the other end of the spectrum is New Hampshire with the lowest rate nationally, at 3.9%. The Granite State benefits from a stable job market, low unemployment, and a strong education system. Paired with relatively affordable healthcare, these factors contribute to higher living standards for its residents, reducing the risk of poverty.

___________________________________

The Leviticus 25 Plan is the one plan in America with the raw, irresistible power to lift millions of qualifying U.S. citizens up out of poverty and back on the road to living productive lives.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}