The property tax relief plans named in the story below center around shifting tax burdens and squeezing already strained budgets, but do nothing to alleviate overall tax burdens for citizens and businesses.

They do nothing to reverse overall massive state and local budget deficits.

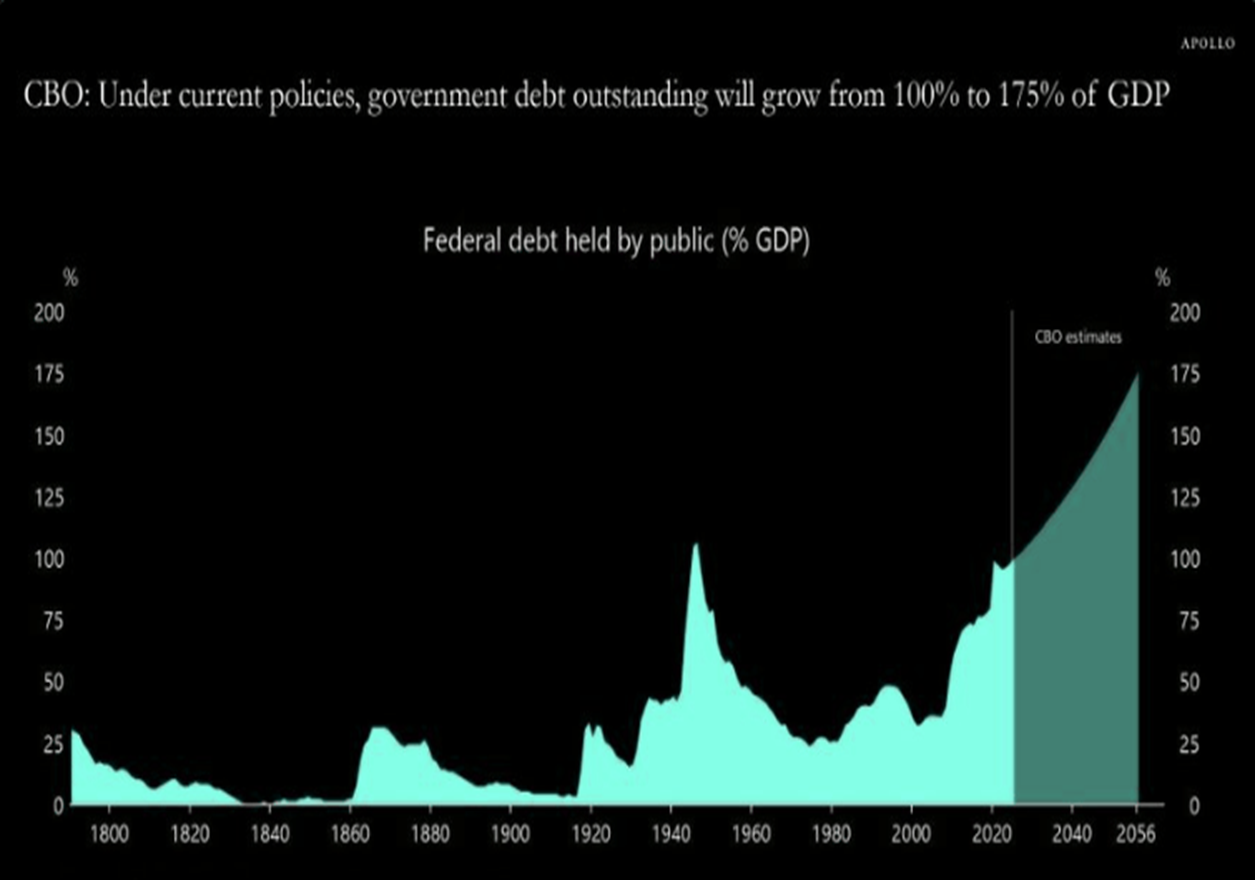

They do nothing to eliminate federal budget deficits – projected by the Congressional Budget Office (CB) to grow from $1.9 trillion in 2026 to $3.1 trillion by 2036 – and generate a powerful new flow of federal budget surpluses.

Finally, the strategies named below will do nothing to lift people up out of poverty, eliminate massive amounts of Household Debt, and restore financial security for millions of America’s hard-working, tax-paying U.S. citizens.

Meet the one plan in America that will resolve these critical issues: The Leviticus 25 Plan

………………………………………

A Property Tax Rebellion Is Emerging In America

ZeroHedge, May 04, 2026 – Authored by Aaron Gifford via The Epoch Times,

Excerpts:

…If 413,000 residents throughout the Buckeye State sign a petition before July 1, a public vote to eliminate local property taxes will appear on the November ballot.

If the signature count falls short, whatever is collected can be applied the following year, or however long it takes, said Blackmarr, media coordinator and a main volunteer for the 3,000-plus member Citizens for Property Tax Reform group.

“We are really hurting in Ohio,” she told The Epoch Times. “People never thought they’d be in this situation.”

Ohio isn’t alone. Forty-six states and the District of Columbia already have limits on annual local property tax levy increases, and leaders in Florida and Texas are pursuing additional legislation to limit government “flexibility” in how it raises revenues, according to a September report from McKinsey and Co., a global management consulting firm whose clients include state and local governments.

Schools, already strapped for cash, hang in the balance. School districts struggle with declining student enrollment, unfunded mandates, state and federal aid loss largely due to skyrocketing Medicaid costs, and spiking employee health insurance costs.

On the local level, mayors and town boards face similar challenges as they try to continue providing public safety, utilities, and infrastructure services.

Fed-up homeowners say it’s high time to try another way to pay their community’s civil servants, perhaps through higher sales tax or state income tax rates, along with slashing administrative bloat in schools and city halls.

“Let the state find a way where 100 percent of the population pays for education,” Ron Shumate, one of Blackmarr’s volunteers from suburban Cincinnati, told The Epoch Times. “They give profit-making businesses a break, but not us.”…

Across States and Communities

In Massachusetts, a citizens group in Great Barrington, near Springfield, wants to shift more of the costs for schools and local infrastructure to part-time residents who own vacation homes. If All Band Together gets its way, the current annual property tax on a full-time residence assessed at $200,000, for example, would decrease by $1,293, while the amount for a seasonal home with the same assessment would increase by $356, according to the group’s website.

In Minnesota and North Dakota, Republican lawmakers have proposed a cap on property tax increases based on the rate of inflation and population growth. If the rate of inflation is 3 percent and the population of a community grows by 1 percent, for example, then the increase cap for the taxing entity would be 3.5 percent. Overriding the cap would require voter approval.

John Phelan, an economist for Minnesota-based Center of the American Experiment, which wrote the model legislation for both states, said the proposal was prompted by property tax hikes last year of between 8 percent and 9.5 percent in some counties. School boards decide on annual district operating budgets and subsequent tax levies; voters only have a say on major expenditures beyond personnel and fixed costs, such as the creation of a multimillion-dollar technology fund.

“The burden shouldn’t be driven by asset values,” Phelan told The Epoch Times. “If [school districts] want to spend more money, they should get permission from the population.”

In Montana, Republican state lawmakers are pursuing a 2 percent cap on property tax hikes for local government funding, but not for schools, which consume about 55 percent of property tax revenues.

Kendall Cotton, president and CEO of the Frontier Institute research and policy center, called the legislation a good start, but said more relief is needed, as home appraisals in growing communities increased by 60 percent this year, resulting in double-digit property tax hikes….

“These big jumps put a lot of pressure on the system, but governments have not been responding in kind,” Cotton told The Epoch Times.

“Misplaced priorities,” he said. “People are really being taxed out of their homes. We are just renting from the government.”

Members of Nebraska’s Epic Option citizen group, like their peers in Ohio, are collecting signatures for a ballot initiative to eliminate property taxes. They paused their efforts to obtain the required 160,000 signatures this year and instead will focus on 2028, according to the group’s website….

Texas Gov. Greg Abbott suggested eliminating school property taxes, and Florida state lawmakers have proposed ending local government property taxes but not school taxes.

A bill in the Georgia state legislature calls for phasing out property taxes and increasing the sales tax. A similar bill was introduced in Pennsylvania. Various property tax reform measures have been proposed in Idaho, Illinois, Indiana, Iowa, Kansas, Oklahoma, South Dakota, and Wyoming, according to their respective state legislature websites.

School Budget Woes

More than one-third of U.S. public school funding comes from local property taxes, while the remainder is provided by state and federal aid, as well as municipal and state sales taxes, according to the National Center for Education Statistics. Some states also apply lottery and gambling revenues.

All told, K–12 spending across the country now exceeds $1 trillion, the Edunomics Lab at Georgetown University reported on April 23.

It also said public per-student spending ranges from about $11,000 in Idaho to more than $31,887 in the District of Columbia. Staffing and school tax rates continue to increase in most districts, while student enrollment decreases.

Typical state and federal aid formulas are based on enrollment, so districts must either cut costs or raise local taxes to offset the decreasing amount of per-student aid. The dependence on $189 billion in federal COVID-19 pandemic relief money, which prompted massive hiring sprees but is now exhausted, has exacerbated the financial crisis in many districts that serve low-income communities with large populations of special needs students…

Nationally, public K–12 enrollment decreased by about 900,500 students in the past decade, while staffing during the same time period increased by about 700,000, or 11.9 percent, according to the Edunomics Lab. The organization also reported planned school layoffs or staff reductions this year in Boston; Cleveland; Milwaukee; Las Vegas; Los Angeles; San Diego; San Francisco; Fresno, California; Richmond, Virginia; Tulsa, Oklahoma; Toledo, Ohio; Anchorage, Alaska; Cedar Rapids, Iowa; Fort Lauderdale, Florida; and “countless small and mid-sized districts.”

“This isn’t temporary,” the Edunomics Lab said in an email to The Epoch Times. “It’s a reset.”….

“The American dream is to own a home, work for at least 30 years, pay it off, retire 10 years later, and be comfortable,” … “If you’re relying on Social Security, that won’t happen.”

“People are tired of being taxed to death and seeing the money stolen,” …

Full article: https://www.zerohedge.com/personal-finance/property-tax-rebellion-emerging-america

____________________________________

The Leviticus 25 Plan will generate massive new tax revenue flows and reduce budget outlays on a broad scale – for federal, state, and local government agencies.

It does not ‘shift’ tax burdens. It eliminates tax burdens.

The Leviticus 25 Plan will give rise to the type of robust fiscal environment for state and local governments that will allow for property tax reductions beyond anything dreamed of in current, ongoing tax reduction discussions.

Teachers, faculty, administrators, support staff in America’s K-12 public and private schools and America’s higher education institutions who choose to participate will benefit enormously by the direct liquidity benefits of The Plan.

The Leviticus 25 Plan will generate $37.303 billion budget surpluses during each of its first five years of activation (2027-2031) – conservative economic scoring analysis – and pay for itself entirely over the succeeding 10-15 year period.

Finally, it will lift people up out of poverty, eliminate massive amounts of Household Debt, and restore financial security for millions of America’s hard-working, tax-paying U.S. citizens.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$95,000 per U.S. citizen – Leviticus 25 Plan 2027 (51641 downloads )

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}