Leftist Groups Tapping $1 Billion To Vastly Expand The Private Financing Of Public Elections

ZeroHedge, Mar 15, 2023 – Excerpt:

Authored by Steve Miller via RealClear Wire,

Democrats and their progressive allies are vastly expanding their unprecedented efforts, begun in 2020, to use private money to influence and run public elections.

Supported by groups with more than $1 billion at their disposal, according to public records, these partisan groups are working with state and local boards to influence functions that have long been the domain of government or political parties.

Registering and turning out voters – once handled primarily by political parties – and design of election office websites and mail-in ballots are being handed over to those same nonprofits, which are staffed by progressive activists that include former Democratic Party advocates, organized labor adherents and community organizers.

Republicans have opposed such efforts, passing legislation in 24 states since 2020 curbing the private financing of elections. But the GOP does not have a comparable, boots-on-the-ground effort to influence election boards and workers, and the private-funding bans haven’t proved absolute in some states.

“There is a cottage industry of 501c3s in public policy and in the political arena, trying to shape the future of immigration or education or any other topic,” said Kimberly Fiorello, a former Republican state representative in Connecticut. “Increasingly they are about elections, election administration, election technology, ballot design, and all with big funding. These groups seem innocuous, but they aren’t innocuous because they are funded by one political side.” \

Many of the progressive groups seeking to influence elections are connected to Arabella Advisors, a Washington-based, for-profit consulting company founded and led by Eric Kessler, a White House appointee during the Clinton administration.

_______________________________

Note again: “…the GOP does not have a comparable, boots-on-the-ground effort to influence election boards and workers, and the private-funding bans haven’t proved absolute in some states.”

If the GOP and Washington Republicans had any type of a populist economic plan with the power to restore financial security for American families, and get the United States of America back on track for long-term economic growth and U.S. Dollar stability….

They would have millions of these voters getting registered by leftists ‘beating the doors down’ to vote for them.

The GOP and Washington Republicans have the opportunity of a lifetime to present a dynamic new ‘roadmap to prosperity’ for America.

They so far, however, have nothing to offer.

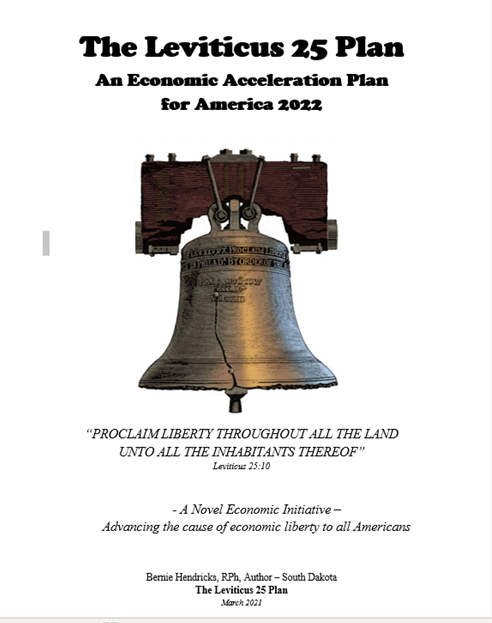

America’s Main Street Republicans do have a powerhouse economic plan for America.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2023 (5867 downloads)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}