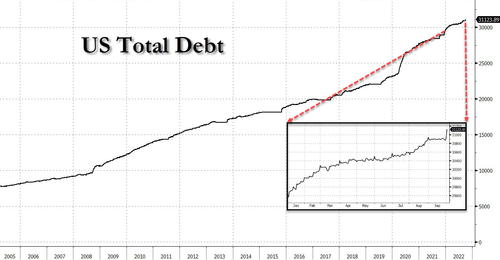

Household Debt in America has now surpassed the $16 trillion mark. Corporate Debt (non-financial) has climbed over $12.583 trillion. The National Debt has reached $31 trillion.

America has an inflation problem. But America’s debt crisis is far and away more serious.

Our Washington politicians, Democrats and Republicans, have no politically viable plan to deal with this crisis.

Main Street America’s Republicans do have a plan – the most powerful debt-busting economic acceleration plan on the face of the earth…

…………………………………………………

US National Debt Blows Past $31 Trillion

ZeroHedge, Wednesday, Oct 05, 2022 – Excerpts:

…”So many of the concerns we’ve had about our growing debt path are starting to show themselves as we both grow our debt and grow our rates of interest,” said Michael Peterson, CEO of the Peter G. Peterson Foundation, in a statement to the NY Times. “Too many people were complacent about our debt path in part because rates were so low.“

Higher rates could add an additional $1 trillion to what the federal government spends on interest payments this decade, according to Peterson Foundation estimates. That is on top of the record $8.1 trillion in debt costs that the Congressional Budget Office projected in May. Expenditures on interest could exceed what the United States spends on national defense by 2029, if interest rates on public debt rise to be just one percentage point higher than what the C.B.O. estimated over the next few years.

Michael Maharrey of SchiffGold notes;…

[T]here is no end to the borrowing and spending in sight. In August alone, the US government ran a massive $219.6 billion budget deficit.

While spending has slowed somewhat with the end of pandemic-era programs, the Biden administration continues to burn through roughly half-a-trillion dollars every single month. With one month left in the fiscal year, the government has spent just over $5.35 trillion.

And there is more spending coming down the pike.

The US government is still handing out COVID stimulus and it wants more. Congress recently pushed through another massive spending bill. Meanwhile, the US continues to shower money on Ukraine and other countries around the world. And we haven’t begun to see the impact of student loan forgiveness.

On top of increased spending, rising interest rates will balloon the debt even more.

Every increase in interest rate raises the federal government’s interest expense. So far in fiscal 2022, the US Treasury has forked out $471 billion just to fund the government’s interest payments.

To put that number into context, at this point in fiscal 2021 the Treasury’s interest expense stood at $356 billion. That represents a 30% year-on-year increase. Interest expense ranks as the sixth largest budget expense category, about $250 billion below Medicare. If interest rates remain elevated or continue rising, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.

According to the Congressional Budget Office, this is exactly what will happen. It projects interest payments will triple from nearly $400 billion in fiscal 2022 to $1.2 trillion in 2032. And it’s worse than that. The CBO made this estimate in May. Interest rates are already higher than those used in its analysis.

……..

The Problem of Debt

In the first place, a large national debt stunts economic growth.

According to the National Debt Clock, the debt to GDP ratio is 125.12%. Studies have shown that a debt-to-GDP ratio of over 90% retards economic growth by about 30%. This throws cold water on the conventional “spend now, worry about the debt later” mantra, along with the frequent claim that “we can grow ourselves out of the debt” now popular on both sides of the aisle in DC.

More immediately, the national debt is a big problem for the Federal Reserve as it drives up interest rates hoping to tame inflation.

The US government can’t keep borrowing and spending without the Fed monetizing the debt. It needs the central bank to buy Treasuries to prop up demand. Without the Fed’s intervention in the bond market, prices will tank, driving interest rates on US debt even higher.

A paper published by the Kansas City Federal Reserve Bank acknowledged that the central bank can’t slay inflation unless the US government gets its spending under control. In a nutshell, the authors argue that the Fed can’t control inflation alone. US government fiscal policy contributes to inflationary pressure and makes it impossible for the Fed to do its job.

______________________________________

Note again this key acknowledgement from the Kansas City Federal Reserve Bank: “…the central bank [Fed] can’t slay inflation unless the US government gets its spending under control.“

The Leviticus 25 Plan will allow for an enormous reduction in outlays, and it will generate massive new tax revenue gains for federal, state, and local government entities.

It will generate $583 billion surpluses at the federal level each of its first five years of activation (2023-2027), and it will completely pay for itself over the next 10-15 years.

It will revitalize economic growth, ramp up productivity, re-establish a citizen centered health care system in the U.S., and restore economic liberty.

The Leviticus 25 Plan is loaded up and ready to launch.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S. citizen – Leviticus 25 Plan 2023 (1146 downloads)