Global Central Banks are all ‘mushrooming’ their balance sheets up to unheard of levels to try to keep their respective economies from sinking deeper into the global ‘debt bog.’

And they are losing the battle. Global Debt is exploding, and economies are stagnating.

Here in the U.S., the Federal government is on a colossal spending spree, adding hundreds of billions of dollars to already-bursting entitlement programs (rent relief benefits, 25% food stamp enhancement, covering for student loans in default, expanding medicaid, broadening eligibility for Medicare benefits, billions of dollars for ‘free’ Covid immunizations), and things like….

The White House Budget (newly released details):

Aug 5, 2021: A few quotes about taxpayer money spent on useless climate studies from a fascinating site called Open The Book

Quote The Third—White House Pluted Bloatocrats

Today, on July 1st, the Biden administration released the annual Report to Congress on White House Office Personnel. President Biden hired czars, expensive “fellows,” “assistants,” and spent on a much larger First Lady (FLOTUS) staff.

The payroll report included the name, status, salary and position title of all 567 White House employees costing taxpayers $49.6 million. (Search Biden’s White House payroll and Trump’s four years posted at OpenTheBooks.com.)

Since January, the Biden administration has quickly staffed up. Here are some key findings from our auditors at OpenTheBooks.com:

• There are 190 more employees on White House staff under Biden than under Trump (377) and 80 more than under Obama (487) at this point in their respective presidencies.

• $9.6 million increase in payroll spending vs. the Trump FY2017 payroll. In 2017, the Trump White House spent $40 million for 377 employees, while the Biden payroll amounts to $49.6 million for 567 employees. All spending amounts are inflation adjusted.

• Hires include 320 female staffers ($28.9 million salaries) vs. 240 male staffers ($20.8 million salaries). In terms of top staffers — Special Assistants — there are 52 female ($6.3 million salaries) vs. 10 males ($1.2 million).

• Currently, there are 12 staffers dedicated – at least in part – to Dr. Jill Biden vs. five staffers who served Melania Trump in her first year (FY2017).

• Counts of the “Assistants to the President” – the most trusted advisors to the president – are the same (22) in for the Biden administration and the Trump and Obama administrations. This year, these advisors make $180,000.

……………………………………………………………………….

Meanwhile, over at the Fed…

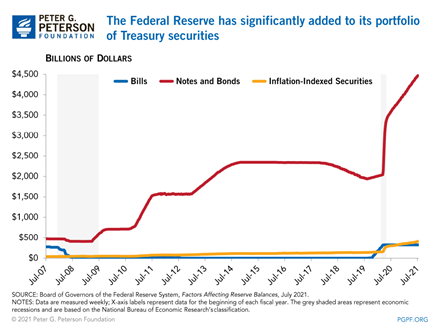

The Federal Reserve Holds More Treasury Notes and Bonds than Ever Before

Peter G. Peterson Foundation – July 28, 2021: https://www.pgpf.org/blog/2021/07/the-federal-reserve-holds-more-treasury-notes-and-bonds-than-ever-before

The U.S. Federal Reserve has significantly ramped up its holdings of Treasury securities as part of a broader effort to counteract the economic impact of the coronavirus (COVID-19) pandemic. Currently, the Federal Reserve holds more Treasury notes and bonds than ever before.

As of July 14, 2021, the Federal Reserve has a portfolio totaling $8.3 trillion in assets, an increase of about $3.6 trillion since March 18, 2020. Longer-term Treasury notes and bonds (excluding inflation-indexed securities) comprise nearly two-thirds of that expansion, with holdings of those two types of securities doubling from $2.2 trillion on March 18, 2020, to $4.5 trillion on July 14, 2021.

By comparison, the Federal Reserve only increased its holdings of Treasury notes and bonds by $116 billion, or roughly 25 percent, between December 5, 2007 and June 24, 2009 (a period known as the Great Recession). Over that same period, the Federal Reserve expanded its total portfolio from $920 billion in December 2007 to $2.1 trillion in June 2009, a total increase of $1.2 trillion. Much of that increase stemmed from the purchase of mortgage-backed securities and the implementation of new programs to address the economic slowdown.

________________________________

There is a dynamic economic acceleration plan, loaded up and ready to go, with the raw power to rescue America and restore economic liberty for U.S. citizens.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

$90,000 per U.S citizen – Leviticus 25 Plan 2022 (3823 downloads)

{kind=link}