America does not need Fed interest rate cuts. It does not need more government ‘stimulation programs,’ or meager tax cuts, or trivial spending reduction measures.

America needs massive public and private debt reduction, massive reductions in government social program spending, citizen-centered health care, economic liberty, and the restoration of free market dynamics.

……………………………………………………

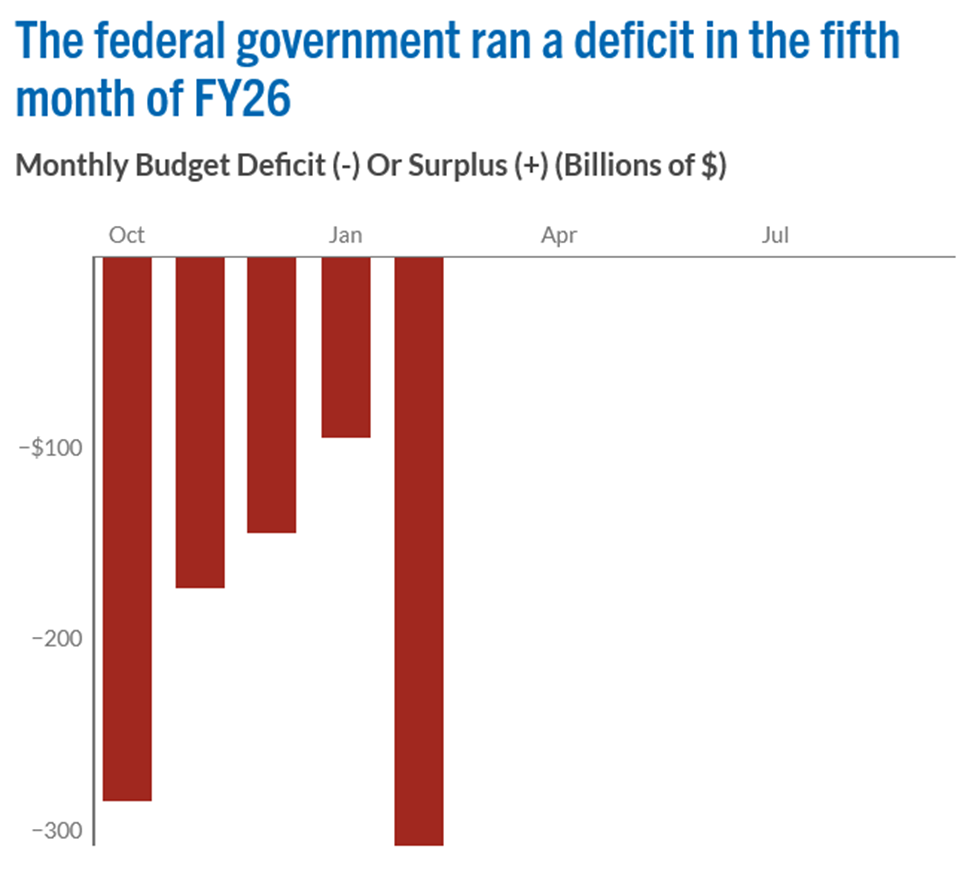

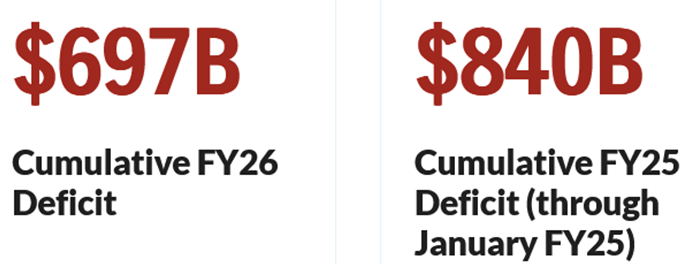

Source: Department of the Treasury

The federal government reported a deficit of $95 billion in the month of January FY26, a decrease of $34 billion from the $129 billion deficit recorded in January FY25. However, February 1 fell on a weekend in both FY25 and FY26, causing certain payments, mostly Medicare-related, to be shifted into January of both years. Those timing shifts inflated outlays for the past two Januarys. Adjusting for those timing shifts, the January FY26 deficit would have been $41 billion less than the same month in the previous year.

Four months through FY26, the deficit was $143 billion below last year’s level. However, the cumulative deficits of FY25 and FY26 have been affected by the aforementioned January 1 timing shifts. Without those effects, the cumulative deficit for FY26 would have been $152 billion less than last year’s adjusted total.

For FY26, total outlays were $2.5 trillion, $46 billion lower than the same period in the previous year. Adjusting for those timing shifts, spending was $37 billion below the same period last year. That increase was driven mainly by three categories: Social Security spending was up by $38 billion, stemming from cost-of-living adjustments and some retroactive payments; Medicare outlays increased by $28 billion (adjusted for timing shifts); and net interest rose by $24 billion

The US government sold $701 billion of Treasury securities this week, spread over nine auctions, including 10-year Treasury notes and 30-year Treasury bonds.

[U.S. Department of Treasury] Sold $54B of 10-Year Treasury notes at 4.18% to replace $25B of maturing 1.73% 10-year notes, pushing up amount outstanding by $29B.

…………………………………….

$11T Funding Crisis: Fed Trapped as Treasury Ponzi Fails (Your Money at Risk)

ITM Trading, Feb 10, 2026 – Excerpts:

Eight weeks. $90 billion in [Fed] Treasury bill purchases. And that’s just the appetizer. There’s $9 trillion in rollovers coming due at today’s rates, plus another $2 trillion in new issuance. That’s $11 trillion the US needs to find buyers for while China dumps Treasuries and Japanese capital flows home.

Taylor Kenney connects the dots: the Fed isn’t providing “technical support.” It’s gearing up for the largest monetization cycle in history, starting from a balance sheet that’s already 7x its pre-2008 level…

……………………………………..

Doug Casey, Feb 17, 2026 – Excerpt:

During the Covid hysteria, the Fed was creating $120 billion out of thin air each month—far larger than the $40 billion per month during QE3, which itself was larger than the monthly pace during QE1 and QE2.

That’s why I expect the coming QE—or whatever they decide to call it—will be significantly bigger than the $120 billion per month they injected into the economy during the Covid scam.

And if gold is already hitting record highs, imagine what happens when the Fed unleashes even more currency debasement than the last rounds of “stimulus.”

Here’s the reality: the monetary system is breaking down—and the people who run it know exactly how to use that breakdown to tighten their grip.

Their endgame is a digital system that can track, limit, and ultimately control every transaction. And anyone who isn’t prepared risks losing far more than purchasing power.

____________________________________

The Leviticus 25 Plan – The most powerful economic acceleration plan in the world:: * $37.303 billion federal budget surpluses annually 2027-2031; * Massive elimination of household debt (mortgage, consumer, student loan, credit card, auto loan debt); * Citizen-centered health care, driven by direct consumer spending for primary health care services – widespread of reductions in bureaucratic costs, middleman expenditures, claims processing; * Powerful, dynamic economic growth; * Long-term financial security for millions of American families;

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The most recent projections from the Congressional Budget Office (CBO) confirm once again that America’s fiscal outlook is on an unsustainable path — increasingly driven by higher interest costs. Growing debt, in addition to the rise in interest rates over the past couple of years, has significantly increased the cost of federal borrowing. In 2025, interest costs on the national debt totaled $970 billion — surpassing most other components of the federal budget.

CBO projects that interest costs in 2026 will reach a new milestone and total $1.0 trillion — a 7 percent increase from the year before, but following increases of 10 and 34 percent in each of the two years before that. This year’s high interest bill is part of a trend that stretches out into the future, as debt continues to climb and relatively high interest rates push up the cost of federal borrowing. Over the next decade, the U.S. government’s interest payments on the national debt are now projected to total $16.2 trillion — the highest dollar amount for interest in any historical 10-year period and nearly double the total spent over the past two decades after adjusting for inflation…

Mounting interest costs put tremendous pressure on the federal budget, making it more difficult and costly to address pressing challenges and invest for the future. In fact, under CBO’s current Budget and Economic Outlook, net interest costs will exceed Medicare spending through the upcoming decade. Rising interest costs also contribute to a vicious cycle of higher debt and additional interest costs.

Another way to contextualize the growth in interest costs: this year, the Treasury will pay $2.8 billion per day, on average, for interest. And unless we change course, that will rise to $5.9 billion per day in 2036.

Any number in the trillions can be hard to grasp. Here are some ways to consider what $16.2 trillion in interest means for America.

$16.2 trillion is:

Approximately $47,000 per person.

Approximately three times what the government spent on net interest between 2006 and 2025.

Approximately three times Social Security’s cumulative cash deficits in the next 10 years.

Approximately five times the cost of the 403 U.S. weather and climate disasters where overall damages each reached or exceeded $1 billion since 1980 (adjusted for inflation).

By any measure, interest costs as part of the federal budget are at an all-time high, and trending even higher in the years ahead. Securing the nation’s fiscal and economic future will mean getting those interest costs under control, which will help relieve pressure within the budget, allow investments in priorities for the country’s future, respond to emergencies, and help ensure a vibrant and inclusive economy for the nation.

_________________________________

The Leviticus 25 Plan economic benefits: • Massive reduction in state, federal government outlays; • Federal budget surpluses of $37.303 billion annually 2027-2031; • Massive reduction in federal interest expense budget item; • Pay for itself entirely over the succeeding 10-15 years; • Vastly improved credit market liquidity, U.S. Dollar strength/stability; • Free market dynamics, powerful, long-term economic growth: 3-4%; • Restored financial health and reduced taxes for millions of American families.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Younger Americans were more likely to say the economy was the country’s most pressing concern last year, according to a new survey.

In the Gallup poll, 32 percent of Americans aged 15 to 34 said that economic issues were “the most important problem” the U.S. “is facing currently,” while 21 percent of Americans aged 35 to 54 said that economic issues were the most important problem. Thirteen percent of Americans aged 55 and older said the same about economic issues.

“Concern about economic issues is present across all generations, but younger adults express the most concern,” Gallup said in an article featuring the survey.

Affordability has come into focus as a key electoral issue with the 2026 midterm elections approaching. President Trump has faced criticism over the issue from Democrats in recent months, who are looking to take back the House and possibly the Senate.

U.S. private-sector employment went up by 22,000 jobs last month, according to a report from the payroll management company ADP.

ADP said in its National Employment Report that January was “a lackluster month for hiring,” but the company also noted that the health care sector “was a standout.”

Another survey from last month found that close to 60 percent of Americans had a negative view of the economy under Trump. In that Wall Street Journal poll, 57 percent said the strength of the economy was “not so good” or “poor.”

The Gallup survey took place from June 14 to June 16, 2025. It polled 1,000 people and has a margin of error of 4.4 percentage points.

___________________________________

Solution: The most powerful economic acceleration plan in the world.

The Leviticus 25 Plan will grant individual U.S. citizens the same direct Federal Reserve liquidity extensions that were provided to major U.S. and foreign banks during the 2007-2010 great financial crisis and again during the 2021-2022 Covid crisis.

Each qualifying U.S. citizen wishing to participate will receive a $60,000 deposit into a designated Family Account (FA) and $35,000 into a designated Medical Savings Account (MSA) via a Fed/U.S. Treasury Citizens Credit Facility.

Benefits – The Leviticus 25 Plan will: * Provide direct liquidity extensions to U.S. citizen families residing in the United States. * Optimize the allocation of primary health-care services funding, including Medicare and Medicaid. * Improve the economic climate for U.S. small businesses; vastly expand employment opportunities; eliminate massive amounts of public and private debt; restore financial health across the nation for all American families. * Generate dynamic, long-term, tax revenue growth cycles for government (federal, state, local). * Reduce the cost of government, strengthen U.S. housing market, and stabilize the banking system. * Reduce the scope of social programs, reduce government control over the daily affairs of U.S. citizens. * Generate $37.303 billion budget surpluses each of its first five years of activation, pay for itself entirely over a 10-15 year period, and set the U.S. Dollar on course for long-term strength and stability.

The Leviticus 25 Plan will revitalize economic growth and re-establish free market principles with positive economic and social incentives for millions of American families.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The Leviticus 25 Plan 2027 – the most powerful economic acceleration plan in the world. Updated economic scoring summary: Every qualifying U.S. citizen who wishes to participate will receive $60,000 (Family Account) and $35,000 (Medical Savings Account). $95,000 per U.S. citizen. Massive public and private debt elimination. Economic liberty

Average annual budget surplus (projected) 2027-2031: $186.517 billion / 5 years: $37.303 billion per year

Note 1: Projected budget surpluses for 2027-2031 do not factor in the additional government tax revenue gains that would accrue from the massive shift in capital away from debt service and into productive economic activity.

Note 2: Projected budget surpluses for 2027-2031 do not factor in the additional government tax revenue gains that would accrue from significantly lower levels of debt deductibility on individual income tax filings.

Note 3: Projected budget surpluses from the Medicaid / CHIP recapture do not take into account the likelihood of fewer citizens actually qualifying for Medicaid / CHIP benefits.

Note 4: Projected budget surpluses from Interest Expense Reductions during each of the first five years of activation (2027-2031) is likely understated due to the fact that ‘debt held by the public’ is projected to increase by 8.5% per year, from $28.278 trillion in 2026 to $40.198 trillion in 2030.

Note 5: The Plan’s funding of individual Medical Savings Accounts (MSAs) with the $7,000 deductible provision per year would result in an enormous drop in the number of claims each year for Medicare reimbursement. Medicare payroll taxes would generate a growing revenue stream, due to stronger economic growth, while outlays would drop significantly from the reduced claims numbers – thereby providing the Fed / Treasury Department with a powerful recapitalization of the Medicare Trust Fund, via the Citizen’s Credit Facility.

The Leviticus 25 Plan – Projection limitations There can be no question that The Leviticus 25 Plan would generate healthy, broad-based economic growth from broad-based debt reduction and improved financial stability at the family level, the restoration of free market dynamics in commerce, and scaling back social program work disincentives.

The Leviticus 25 Plan does not attempt to project how much additional tax revenue and reduced cost of government will be realized, above and beyond the Recapture Provisions, over the course of the initial five years of the plan. In that sense, The Plan understates the effect of additional dynamic economic benefits.

Robust funding of Medical Savings Accounts and the elimination of millions of insurance claims and claims resolutions for basic primary care and everyday healthcare purchases swill save millions of man-hours of health care cost on an annual basis. Scaling back government involvement in basic primary care and everyday healthcare purchases for millions of Americans will also generate massive cost savings.

The Plan makes no attempt to project the positive effects of the streamlined, consumer-driven efficiencies that will emerge, and the cost reduction and improvement in services. The Plan therefore understates the benefits. The Plan projects an 80 percent participation rate by U.S. citizens. It is assumed that a large number of wealthy Americans will not participate, because their tax refunds are larger than the annual Plan benefits. And it is assumed that a large number of Americans receiving significant government benefits for extraordinary health or economic issues will also not participate.

Cost savings from the reductions in massive social welfare spending and other programs, like unemployment insurance, workman’s compensation, SSI and SSDI can be difficult to quantity, since state and federal funding mechanisms may both be involved in various ways. In that regard, The Plan may understate, or it may overstate, the benefits.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Monetary expansion doesn’t spread evenly. New money concentrates where it enters—in financial assets, real estate, and the balance sheets of those with credit access. This creates two economies: one for asset-holders, enriched by expansion; another for wage-earners, crushed by the cost increases that follow.

To hit 2 percent consumer inflation, central banks must restrict money supply enough to destroy demand among ordinary households—the people furthest from the monetary spigot. But they’ve already inflated assets to the point where millions of families, pension funds, and governments depend on continued expansion to stay solvent. Tightening enough to hit 2 percent CPI means liquidating the phantom wealth propping up the entire system. We glimpsed this in 2022-2023: modest rate increases triggered bank failures and sovereign debt crises.

The trap is complete: monetary expansion enriches the few while punishing the many, but contraction would bankrupt both.

The Measurement Mirage

The CPI doesn’t measure what people experience. Housing costs appear through “owner’s equivalent rent”—a fiction understating reality by a significant amount. Healthcare, education, childcare—costs that have doubled or tripled—receive minimal weight. Meanwhile, falling electronics and import prices pull the average down.

A family whose rent has doubled, childcare tripled, and healthcare quadrupled is told inflation is “only” three percent. Central banks fight to hit a target disconnected from lived reality, using tools that damage those already most hurt by mismeasured inflation.

The Sovereign Debt Vise

The United States now carries $38.12 trillion in debt, with deficits locked in structural overdrive. For fiscal year 2025 (ending September 30, 2025), the federal budget deficit totaled approximately $1.8 trillion—marking one of the largest annual deficits in US history in nominal terms. In calendar year 2025 alone (through November), the debt has already climbed by over $1 trillion, representing one of the fastest accumulations outside of pandemic-era spikes.

The Fed cannot pursue “price stability” without triggering sovereign default. It cannot monetize the debt without abandoning its inflation target. Monetary and fiscal policy have fused into a single system where every path leads to ruin.

…..

The QT Surrender: Why the Fed Can’t Stop Printing

The Federal Reserve announced in October 2025 that quantitative tightening will end in December after reducing its balance sheet from $9 trillion to $6.6 trillion. This isn’t a policy choice—it’s mathematical surrender.

The Fed’s balance sheet remains bloated with low-yielding assets from QE rounds dating to 2008, earning two-three percent while the Fed pays 4.5 percent on reserves it created to buy them. The Fed operated at a loss for three consecutive years.

But the Fed cannot shrink its balance sheet to pre-crisis levels without triggering a liquidity crisis. The modern financial system operates under an “ample reserves framework”—a euphemism for permanent monetary expansion. Banks, pension funds, and Treasury markets have become structurally dependent on massive reserve creation. When the Fed attempted modest QT reductions, repo markets showed stress. They’re stopping, not because inflation is conquered, but because the financial system cannot handle genuine monetary normalization.

The QT cessation sets the stage for QE’s inevitable return. The Fed is now in what Austrian economists call the “crack-up boom” phase—the point where monetary authorities choose between deflation (and cascading debt defaults) or continued inflation (and currency destruction). The QT cessation signals their choice.

…..

Policy Checkmate—The Impossible Choice

High inflation destroys savings, distorts price signals, and creates social instability. But we must be honest: the 2 percent target cannot be achieved without either.

The options seem to be: 1) a deflationary depression that liquidates the debt overhang—and likely the social order with it; 2) a financial repression that slowly confiscates wealth through negative real rates; or, 3) a restructuring of how we conceptualize monetary stability in a hyper-financialized economy.

The first option is politically impossible and humanly catastrophic. The second is what we’re already doing, just with more dishonesty. The third requires admitting central banking as currently practiced has failed.

…..

The Endgame

This is the endgame of monetary central planning: not with hyperinflationary bang or deflationary whimper, but with the confused stumbling of policymakers who cannot admit their tools have welded them into a cage. The two percent target, tariff dividends, ample reserves frameworks, and technocratic jargon cannot obscure the simple truth: we have built an economic system requiring perpetual monetary expansion to avoid collapse, and we’ve run out of ways to pretend this is sustainable policy rather than slow-motion currency debasement with extra steps.

___________________________________________

The Leviticus 25 Plan is the one and only economic acceleration plan in the world with the power to ‘rebalance the scales’ which had tipped notoriously in favor of America’s “asset-holders, enriched by expansion” … to now tip back strongly in favor of America’s “wage-earners, crushed by the cost increases that follow.”

The Leviticus 25 Plan will furthermore eliminate America’s annual federal budget deficits, projected to average over $2 trillion over each of the coming five years, and thereby strengthen the U.S. Dollar and temper the ever-growing pressures of currency debasement.

The Leviticus 25 Plan will (conservatively) generate federal budget surpluses averaging $37.303 billion in each of its first five years of activation (2027-2031) and effectively pay for itself entirely over the following 10-15 year period.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

Average annual budget surplus (projected) 2027-2031: $186.517 billion / 5 years: $37.303 billion per year

Note 1: Projected budget surpluses for 2027-2031 do not factor in the additional government tax revenue gains that would accrue from the massive shift in capital away from debt service and into productive economic activity.

Note 2: Projected budget surpluses for 2027-2031 do not factor in the additional government tax revenue gains that would accrue from significantly lower levels of debt deductibility on individual income tax filings.

Note 3: Projected budget surpluses from the Medicaid / CHIP recapture do not take into account the likelihood of fewer citizens actually qualifying for Medicaid / CHIP benefits.

Note 4: Projected budget surpluses from Interest Expense Reductions during each of the first five years of activation (2027-2031) is likely understated due to the fact that ‘debt held by the public’ is projected to increase by 8.5% per year, from $28.278 trillion in 2026 to $40.198 trillion in 2030.

Note 5: The Plan’s funding of individual Medical Savings Accounts (MSAs) with the $7,000 deductible provision per year would result in an enormous drop in the number of claims each year for Medicare reimbursement. Medicare payroll taxes would generate a growing revenue stream, due to stronger economic growth, while outlays would drop significantly from the reduced claims numbers – thereby providing the Fed / Treasury Department with a powerful recapitalization of the Medicare Trust Fund, via the Citizen’s Credit Facility.

The Leviticus 25 Plan – Projection limitations There can be no question that The Leviticus 25 Plan would generate healthy, broad-based economic growth from broad-based debt reduction and improved financial stability at the family level, the restoration of free market dynamics in commerce, and scaling back social program work disincentives.

The Leviticus 25 Plan does not attempt to project how much additional tax revenue and reduced cost of government will be realized, above and beyond the Recapture Provisions, over the course of the initial five years of the plan. In that sense, The Plan understates the effect of additional dynamic economic benefits.

Robust funding of Medical Savings Accounts and the elimination of millions of insurance claims and claims resolutions for basic primary care and everyday healthcare purchases swill save millions of man-hours of health care cost on an annual basis. Scaling back government involvement in basic primary care and everyday healthcare purchases for millions of Americans will also generate massive cost savings.

The Plan makes no attempt to project the positive effects of the streamlined, consumer-driven efficiencies that will emerge, and the cost reduction and improvement in services. The Plan therefore understates the benefits. The Plan projects an 80 percent participation rate by U.S. citizens. It is assumed that a large number of wealthy Americans will not participate, because their tax refunds are larger than the annual Plan benefits. And it is assumed that a large number of Americans receiving significant government benefits for extraordinary health or economic issues will also not participate.

Cost savings from the reductions in massive social welfare spending and other programs, like unemployment insurance, workman’s compensation, SSI and SSDI can be difficult to quantity, since state and federal funding mechanisms may both be involved in various ways. In that regard, The Plan may understate, or it may overstate, the benefits.

The Leviticus 25 Plan 2027 – the world’s most powerful economic acceleration plan: Updated economic scoring summary.

Interest expense on projected deficits 2027-2031

Federal debt has increased from $22.1 trillion in 2020 to $37.64 trillion as of July 1, 2025. Federal debt held by the public was reported to be $30.298 trillion, with remainder, $7.342 trillion, comprised of intra-governmental debt outstanding, which arises when one part of the government borrows from another. This intra-governmental debt interest expense item will be omitted from this calculation, since those dollars are not expensed directly.

St. Louis Fed Q3 2025: Debt held by the public, $30.3 trillion, makes up 80.0% of the $37.64 trillion National Debt. U.S. Department of the Treasury (fiscal data): Interest Expense and Average Interest Rates on the National Debt FYTD 2026: 3.324%

The Bear Traps Report, Dec 30, 2024–Excerpts: “CBO data, Bloomberg. The average weighted coupon on the U.S. debt load is about 2.7% vs. over 4.5% for 10-year U.S. Treasuries. As bonds mature, they get refinanced at much higher yields.”

“Incoming Stress Points – In 2025 the U.S. Treasury faces $9.6Tr of maturities in their so-called publicly held debt. In Q1 alone — the government faces $5.58Tr of maturities (bonds coming due, redemption), but 86% of those are short-term bills that the Treasury department rolls over into new 4-week, 8-week, 3,4, or 6-month bills, among others.”

“As a result, almost daily bill auctions are coming to a theater near you, as the Treasury Department mindlessly keeps pushing new paper into the market to pay back the colossal amount of maturing debt.”

This projection will assume an average monthly interest rate of 3.324% for 2026, and a conservative average monthly interest rate of 3.25% in calculating the interest expense to be eliminated during the budget surplus years of 2027-2031. This projection also assumes that annual federal budget deficits will be funded through Treasury Issuance at an average of 80.0% rate for Debt Held by the Public.

Year / Annual Deficit/2 2025: $1.865 trillion/2 X .79 X .03 = $22.965 billion 2026: $1.713 trillion/2 X .79 X .03 = $21.934 billion 2027: $1.687 trillion/2 X .80 X .0325 = $21.931 billion 2028: $1.911 trillion/2 X .80 X .0325 = $24.843 billion 2029: $1.938 trillion/2 X .80 X .0325 = $25.194 billion 2030: $2.140 trillion/2 X .80 X .0325 = $27.820 billion 2031: $2.233 trillion/2 X .80 X .0325 = $29.029 billion

Recapture: Total interest expense eliminated by projected operating surpluses: $128.817 billion

The Leviticus 25 Plan 2027 – the most powerful economic acceleration plan in the world: Updated economic scoring summary.

Medicaid/CHIP Recapture Each U.S. citizen participating in The Plan will receive a $35,000 deposit, funded through a Federal Reserve / U.S. Treasury Department-based Citizens Credit Facility, into a personal Medical Savings Account (MSA).

The Leviticus 25 Plan assumes 80% participation by Medicaid / CHIP enrollees. Within this comprehensive economic plan, The U.S. Health Care Freedom Plan provides Medical Savings Account (MSA) funding of $35,000 to cover the $7,000 deductible for Medicaid and CHIP eligible primary care events and select out-patient care services – primarily related to routine medical appointments, Medicaid prescription events, disease state monitoring clinics, and other desired primary care services.

September 2025 Medicaid & CHIP Enrollment – 77.05 million individuals were enrolled in Medicaid and CHIP in the 50 states and the District of Columbia that reported enrollment data for September 2025. 69,797,328 people were enrolled in Medicaid; 7,252,967 enrolled in CHIP.

Using a conservative estimate of 77.0 million for 2025, with a projected annual growth rate of 2%: 2025: 77.00 million 2026: 78.54 million 2027: 80.11 million 2028: 81.71 million 2029: 83.34 million 2030: 85.10 million 2031: 86.80 million

Total: 417.06 million receiving benefits 2027-2031

Average annual enrollment (2027-2031): 83.41 million 83.41 million X .8 = 66.728 million X $7,000/year X 5 years = $2.335 trillion

Total Medicaid/CHIP recapture during the 5-year target period (2027-2031): $2.335 trillion

Medicare Recapture Each U.S. citizen participating in The Plan will receive a $35,000 deposit, funded through a Federal Reserve / U.S Treasury Department-based Citizens Credit Facility, into a personal Medical Savings Account (MSA).

The Leviticus 25 Plan assumes 80% participation by Medicare enrollees. Within this comprehensive economic plan, The U.S. Health Care Freedom Plan provides Medical Savings Account (MSA) funding of $35,000 to cover a $7,000 annual deductible for Medicare-eligible primary care events and select out-patient services – primarily related to routine medical appointments, Medicare Part D prescription events, disease state monitoring clinics, and other desired primary care services.

There were 69.6 million people were enrolled in Medicare as of October 2025.

Projection: “Medicare spending grew 7.8% to $1,118.0 billion in 2024, or 21 percent of total National Health Expenditures.”

“Over 2024-33 average NHE growth (5.8 percent) is projected to outpace that of average Gross Domestic Product (GDP) growth (4.3 percent), resulting in an increase in the health spending share of GDP from 17.6 percent in 2023 to 20.3 percent in 2033.”

“Medicare enrollment is projected to grow steadily, with total beneficiaries rising to an estimated 78-79 million by 2030-2031.”

Applying a conservative projected enrollment growth rate of 2.5% annually through 2031, with an 80% participation rate, and a $7,000 annual deductible for the 5-year target period (2027-2031): 2025: 69.60 million X .8 X $6,000 = $334,080,000 2026: 71.34 million X .8 X $6,000 = $342,432,000 2027: 73.12 million X .8 X $7,000 = $409,472,000 2028: 74.95 million X .8 X $7,000 = $419,720,000 2029: 76.82 million X .8 X $7,000 = $430,192,000 2030: 78.74 million X .8 X $7.000 = $440,994,000 2031: 80.70 million X .8 X $7,000 = $451,920,000

Total Medicare recapture during the 5-year target period (2027-2031): $2.152 trillion

VA Healthcare The Leviticus 25 Plan assumes 80% participation by Veterans Administration healthcare enrollees. Within this comprehensive structure, The U.S. Health Care Freedom Plan provides Medical Savings Account (MSA) funding of $35,000, through a Federal Reserve / U.S. Treasury-based Citizens Credit Facility, to cover annual $7,000 deductibles for VA primary healthcare services over the course of the 5-year target period (2027-2031).

FY 2025 – 9.2 million enrollees in the VA health care system. The plan assumes a stable 9.2 million enrollment in the VA Health Care System.

2027: 9.2 X 0.8 X $7,000 = $51,520,000,000 2028: 9.2 X 0.8 X $7,000 = $51,520,000,000 2029: 9.2 X 0.8 X $7,000 = $51,520,000,000 2030: 9.2 X 0.8 X $7,000 = $51,520,000,000 2031: 9.2 X 0.8 X $7,000 = $51,520,000,000

Total recapture: $257,600,000,000

Average annual recapture (2027-2031): $51.52 billion

TRICARE The Leviticus 25 Plan assumes 80% participation by qualified TRICARE enrollees.

Through The U.S. Health Care Freedom Plan component, participating members will receive a Medical Savings Account (MSA) funding injection of $35,000, through a Federal Reserve / U.S. Treasury Department-based Citizens Credit Facility, to cover annual $7,000 deductibles for desired primary care and out-patient services over the course of the 5-year target period (2027-2031).

There are currently ~9.4 million U.S. citizen beneficiaries in various locations around the world. Recapture – total (2027-2031): 9.4 million X 0.8 X $7,000 X 5 years: $263.2 billion

Federal Employee Health Benefits (FEHB) The Leviticus 25 Plan assumes 80% participation by FEHB enrollees. Participating members will receive a Medical Savings Account (MSA) funding injection of $35,000, through a Federal Reserve / U.S. Treasury Department-based Citizens Credit Facility, to cover annual $7,000 deductibles for desired primary care and out-patient services over the course of the 5-year target period (2027-2031).

FEHB Program carriers cover most active, full-time civilian employees and retirees of the U.S. government and their families. The Program now provides benefits to over 8.2 million federal enrollees and dependents and offers over 180 health plan choices to federal members.

Note – the Federal government also pays approximately 72% of premium costs per enrollee. Recapture – total (2027-2031): 8.3 million X 0.8 X $7,000 X 5 = $229.6 billion

Social Security Disability Income (SSDI) The Leviticus 25 Plan specifies that qualifying participants will not be eligible for SSDI benefits. The Plan assumes 80% participation by SSDI recipients.

December 2025 – total beneficiaries: 8.163 million recipients; Total monthly SSDI benefit payments: $12.182 billion; Total annual SSDI benefit payments: $146.184 billion.

This projection assumes a conservative 3% growth per year for 2027-2031, covering both enrollment growth and COLA: 2025: $146.184 billion 2026: $150.570 billion 2027: $155.087 billion 2028: $159.740 billion 2029: $164.532 billion 2030: $169.468 billion 2031: $174.552 billion

Total: $823.379 billion / Average per year: $164.676 billion

Total for 5-year target period 2027-2031: Plan assumes 80% participation – recapture: $823.379 billion X 0.8 = $658.70 billion

“SSDI benefits are financed primarily by part of the Social Security payroll tax..”

“Social Security’s trustees project that the share of people in the United States receiving SSDI will rise somewhat over the next 20 years and then remain stable.”

Note: The 3% growth projection, covering both the enrollment increase and annual COLA, is likely a conservative estimation for the period 2027-2031.

The Leviticus 25 Plan – the most powerful economic acceleration plan in the world: Updated economic scoring summary.

Federal Income Tax Recapture This scoring model assumes that 80% of qualified U.S. citizens will voluntarily participate in The Leviticus 25 Plan. Participants must give up their tax refunds through the Plan’s recapture provisions for the 5-year target period (2027-2031).

According to 2025 IRS Filing season statistics, through Dec 28, 2025: 103,846,000 total refunds were paid out, totaling $328.878 billion.

Refund totals have increased by approximately $25.117 billion over the past eight years, from $303.761 billion (2018) to a current (estimated) $328.878 billion (2025), representing an average increase of $3.14 billion per year.

A conservative estimated average of $3.1 billion per year (2027-2031) will be used for this recapture calculation. 2024: $329.1 billion (actual) 2025: $328.9 billion (actual) 2026: $332.0 billion 2027: $335.1 billion 2028: $338.2 billion 2029: $341.3 billion 2030: $344.4 billion 2031: $347.5 billion

Total: $1.707 trillion

Total recapture X 80%: $1.707 trillion X .8 = $1.366 trillion

Total recapture per annum (2027-2031): $1.366 trillion / 5 = $273.2 billion

Participants in the Plan will forego Economic Security Program benefits and select means-tested welfare benefits for the period 2027-2031.

Economic security programs: Outlays were about 10 percent (or $701.6 billion) of the federal budget in 2025, in funding [safety net] programs that provide aid (other than health insurance or Social Security benefits) to individuals and families facing hardship. Economic security programs include: the refundable portions of the Earned Income Tax Credit and Child Tax Credit, which assist low- and moderate-income working families; programs that provide cash payments to eligible individuals or households, including unemployment insurance and Supplemental Security Income for low-income people who are elderly or disabled; various forms of in-kind assistance for low-income people, including the Supplemental Nutrition Assistance Program (formerly known as food stamps), school meals, low-income housing assistance, child care assistance, and help meeting home energy bills; and other programs such as those that aid abused or neglected children.1

The Leviticus 25 Plan will generate annual budget surpluses of $37.303 billion during each of the first five years of activation (2027-2031), versus the CBO-projected $1.982 trillion average annual deficits, representing a positive budget gain of $2.019 trillion annually for the period.

Budget surpluses would be negotiable for partial transfer back to the Federal Reserve to effect ongoing reductions of the Citizens Credit Facility balance sheet. More importantly, $37.303 billion annual budget surpluses would provide a dynamic counterbalance to the inevitable demands on the Fed to purchase T-Bills and T-Bonds in support of Treasury Auctions throughout 2027-2031.

Overview, Primary Assumptions, Economic Scoring

The Leviticus 25 Plan activation period is slated for the 5-year period beginning in 2027 and ending in 2031.

The Leviticus 25 Plan – Each participating U.S. citizen will receive a $60,000 deposit into a Family Account (FA) and a $35,000 deposit into a Medical Savings Account (MSA).

All U.S. citizens residing in the United States are eligible to participate, contingent upon meeting qualification standards and agreement to specified recapture provisions. Participants (other than ‘custody account’ applicants) must prove stable credit history, stable job history, no recent drug/felony convictions.

These general recapture provisions include:

Waiving all federal income tax refunds for a period of 5 years.

Waiving benefits from economic security programs, select benefits from means-tested welfare programs, SSI, and SSDI for a period of 5 years.

Enrollees in the Medicare, VA Healthcare system, Federal Employees Health Benefits (FEHB), and TRICARE will be subject to a $7,000 deductible for primary care and outpatient services annually for a period of 5 years. (See full plan for more details)

Primary scoring assumptions:

The Plan assumes an 80% participation rate by U.S. citizens. Wealthier Americans would choose not to participate, due to the comparative benefit of income tax refund amounts. Many individuals of lower socio-economic sector would also choose not to participate, due to the comparatively high benefits profiles that they would not wish to give up.

The Plan assumes that participating families would use significant funds to pay down / eliminate debt, and that these longer-term, lower debt service obligations would enhance the financial security of participating families for several decades beyond the opening activation period. Federal, state, and local government entities would benefit from longer-term tax revenue growth and reduced citizen dependence on government-based entitlement program benefits.

The Plan assumes that dynamic new efficiencies would emerge in the healthcare system – with more families managing/directing healthcare expenditures through their MSAs.

The Plan assumes that apart from the recapture provisions, there would also be significant tax revenue growth for federal, state and local government entities from free-market economic revitalization, more people working and paying taxes, and from the elimination of various income tax deductions (e.g. mortgage / HELOC interest expense).

The Plan assumes that there would not be a massive full-scale move back into the means-tested welfare programs, income security programs, SSI, and SSDI at the end of the initial 5-year activation period.

The benefits of a free-market economy and newfound economic liberty for American families would provide positive economic inertia throughout years 5-10, and for several decades beyond.

Recapture provisions would provide substantial federal budget surpluses for each year of the initial 5-year period. Economic growth over the following 10-15 years would generate sufficient recapture funding and tax revenue growth to offset the entire initial Federal Reserve balance sheet expansion.

Significant inertia from The Plan would also provide on-going, market-based growth benefits over succeeding years that far exceed any prospect for healthy economic growth that may be expected under America’s current big-government, central-planning approach.

Dynamic economic benefits would flow from:

Family level massive debt elimination, financial security gains.

Timely, sweeping reversal of big government “central planning” control.

Productivity gains from reversal of work disincentives currently embedded in social programs.

Stabilization of bank capitalization, housing market.

Strengthen / stabilize long-term value of U.S. Dollar.

Minimizing the role of government in managing, directing, controlling the affairs of citizens.

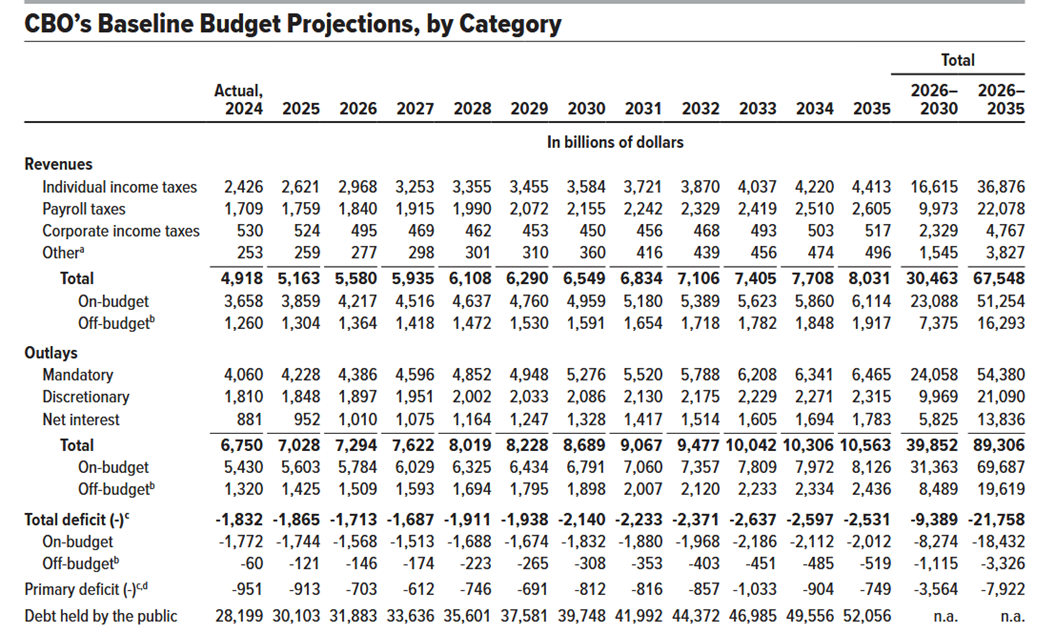

Federal Budget Deficit Projections – Congressional Budget Office The Budget and Economic Outlook: 2025-2035 projects budget deficits ranging from $1.713 trillion 2026 to $2.140 trillion in 2030, and on up to $2.531 trillion by 2035. Actual deficits for the out years are likely to be higher than CBO projections, based upon history (“actual” versus “projected”).