Fredrich A. von Hayek: “We must make the building of a free society once more an intellectual adventure, a deed of courage…. Unless we can make the philosophic foundations of a free society once more a living intellectual issue, and its implementation a task which challenges the ingenuity and imagination of our liveliest minds, the prospects of freedom are indeed dark. But if we can regain that belief in the power of ideas which was the mark of liberalism at its best, the battle is not lost.”

_________________________

To help make America’s rebuild a reality…

The Leviticus 25 Plan – An Economic Acceleration Plan for America

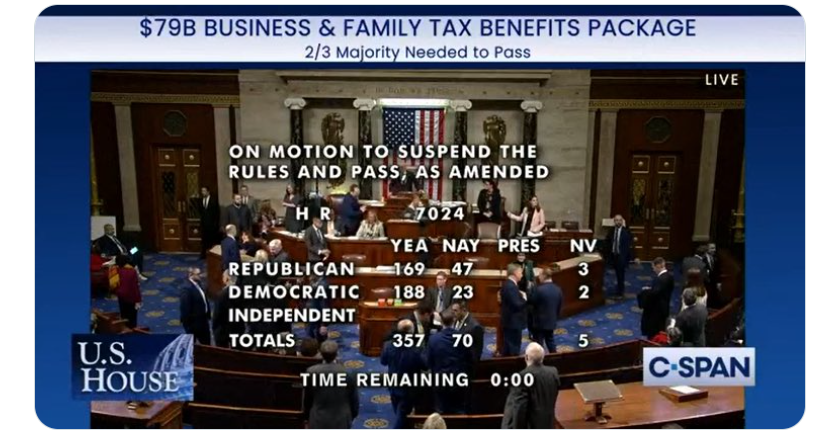

169 Republicans joined 188 Democrats to expand welfare. There were only 47 no votes from Republicans.

More Welfare

.@RepThomasMassie on the welfare tax bill: “There’s something in this bill called ‘tax credits,’ but they’re also called ‘refundable.’ So what is a refundable tax credit?

It’s welfare by a different name. We are going to give cash payments, checks to people who don’t even pay… pic.twitter.com/lZGZYImGus | — Rep. Matt Gaetz (@RepMattGaetz) January 31, 2024

“There’s something in this bill called ‘tax credits,’ but they’re also called ‘refundable.’ So what is a refundable tax credit? It’s welfare by a different name. We are going to give cash payments, checks to people who don’t even pay taxes. The hard-working constituents that I represent in Kentucky are tired of getting up at 6am, driving an hour or two to work, working their hind ends off to watch their neighbors collect these checks, of which there will be more of after this bill. It’s just wrong.”…

Where Socialism Works

“SOCIALISM ONLY WORKS TWO PLACES — HEAVEN WHERE THEY DON’T NEED IT — AND HELL WHERE THEY ALREADY HAVE IT” ~RONALD REAGAN

Mind Boggling Support – Social Security and Medicare spending climbed 12% to 13% in the first three months of this fiscal year compared to last. Sweetened subsidies are boosting ObamaCare enrollment. Growing entitlement spending is one reason that government, healthcare and social assistance accounted for more than half of the net new jobs in December, according to the Bureau of Labor Statistics.

The deficit would be even larger if not for the Internal Revenue Service holding back a wave of more stimulus. The agency in September paused processing new claims for the Covid-era Employee Retention Credit owing to concerns over abuse and fraud. By one estimate, the IRS has a $244 billion backlog of claims, which will flood the economy when the IRS processes them.

All of this spending contributes to GDP, at least in the short term. But much of this isn’t productive growth that will improve living standards in the long term, and the bills for all this spending will probably be paid in higher taxes.

That’s why it’s mind-boggling that House Republicans want to help Democrats throw another deficit party … tax credit and extend some business tax breaks through 2025.

Democrats have signed on because they view the child-credit provisions as a down payment on a guaranteed annual income and want to boost flagging business investment this year. The political mystery is why Republicans want to add their signature. The tax bill negotiated by Democrat Ron Wyden and GOP Rep. Jason Smith is another in-kind contribution to the Democratic re-election campaign.

The legislation now heads to the Senate. If the Senate Republicans hoist another surrender flag, Biden would sign the bill.

But it takes 60 votes in the Senate. That’s not a given.

Senators are haggling over spending and immigration legislation. They are scheduled to be on recess for two weeks starting Feb. 12, and aides don’t expect lawmakers to consider the tax bill before then.

“I’m certainly not just willing to let the House pass something and then say, ‘Oh well, we’ll just take that,’” said Sen. John Cornyn (R., Texas), who said he doesn’t feel any urgency to advance the bill. “The price we’re having to pay is pretty outrageous.”

The price is not pretty outrageous, it’s very outrageous.

Question of the Day – Of what possible use are Republicans when the majority vote like Democrats?…

In case you haven’t figured this out, it’s highly inflationary.

…………………………………………………….

Note: According to the Wall Street Journal, Jan 17, 2024, “The overall deal would cover the 2023, 2024 and 2025 tax years and cost roughly $78 billion.”

_______________________________

Main Street America Republicans have a powerful alternative plan.

This Plan will lift working Americans up out of poverty and reduce dependence on government. It will revive a macro economic environment in America where federal, state and local governments will be able to cut taxes for families and small businesses, rather than continually dipping into the budget-busting tax credits ‘cookie jar.’

This Plan will reduce entitlement spending, restore financial security for America’s hard-working, tax-paying U.S. citizens, and, most importantly, generate $112.6 billion federal budget surpluses annually (2025-2029).

The Leviticus 25 Plan – An Economic Acceleration Plan for America

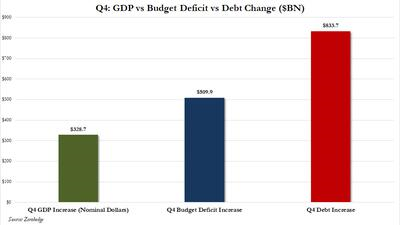

Peter St Onge writes it up and it is a doozy: “Fresh GDP numbers came in and it was a blowout. The kind of blowout that only a $2.7 trillion government deficit can buy while the private economy crumbles around it. Another couple blowout GDP reports like this and Americans will be living under an overpass.”

The essential ruse comes down to unfathomable amounts of government spending that is being recorded as productivity and output, and interpreted by media as growth. “In the past 12 months the federal deficit increased by $1.3 trillion. Yet we only got half that in GDP—about $600 billion. In other words, everything else shrank. It’s even worse for that brave and stunning Q4—there we got just $300 billion in extra GDP for—wait for it—$834 billion of new federal debt.”

To put a fine point on it: “Essentially, [GDP is measuring] the pace at which we’re going Soviet, replacing private wealth with government waste.” In his interpretation of the data, we are destroying wealth at the fastest rate since 2008.

“While Q4 GDP rose by $329 billion to $27.939 trillion, a respectable if made up number, what is much more disturbing is that over the same time period, the US budget deficit rose by more than 50 percent, or $510 billion. And the cherry on top: the increase in public US debt in the same three month period was a stunning $834 billion, or 154 percent more than the increase in GDP. In other words, it now takes $1.55 in budget deficit to generate $1 of growth… and it takes over $2.50 in new debt to generate $1 of GDP growth!”

To further the analysis, and doing the math: “[E]very dollar in GDP growth cost $1.69 in new debt, and also means that every new job cost future generations of Americans $957,100.48.”

To say this is unsustainable is more than obvious. It is a disaster and this is dragging American prosperity into the pits, if by prosperity you mean quality of life. No matter how many gizmos to which you have access, the resources for living a good life are depleting very fast. The idea of a one-income family is nearly extinct, whereas it was the norm three-quarters of a century ago…

The United States has been the world center of technological innovation during these years, and the historical home for free enterprise and entrepreneurship. We should have had the greatest boom times in our history! Instead, government stole all that energy for itself. It’s a tragedy…

On the good side, we are seeing the evaporation of trust in media, medicine, academia, and government. Large media organizations are laying off workers in droves just to survive, and the woke agenda generally seems on the ropes.

________________________________________

Again: “To say this is unsustainable is more than obvious. It is a disaster and this is dragging American prosperity into the pits, if by prosperity you mean quality of life. No matter how many gizmos to which you have access, the resources for living a good life are depleting very fast. The idea of a one-income family is nearly extinct, whereas it was the norm three-quarters of a century ago.”

Washington Democrats are feeding America’s debt-binged economic decline.

Washington Republicans have no credible counter-plan to get America’s mushrooming debt cycle back under control and get the U.S. economy back on track. This is one of the most shameful episodes in the history of the GOP.

Main Street America Republicans do have a plan…

The Leviticus 25 Plan will generate average annual budget surpluses of $112.6 billion in each of its first five years of activation (2025-2029) vs current CBO-projected average annual deficits of $1.795 trillion for the same period.

This represents an astounding $1.9 trillion positive budget gain annually (2025-2029) for the U.S. federal budget.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

The Leviticus 25 Plan – annual economic scoring update. For each of the first five years of activation (2025-2029), The Leviticus 25 Plan will generate average annual budget surpluses of $112.6 billion vs current CBO-projected average annual deficits of $1.795 trillion for the same period.

Overview, Primary Assumptions, Economic Scoring

The Leviticus 25 Plan activation period is slated for the 5-year period beginning in 2025 and ending in 2029.

1. The Leviticus 25 Plan– Each participating U.S. citizen will receive a $60,000 deposit into a qualified Family Account (FA) and a $30,000 deposit into a qualified Medical Savings Account (MSA).

All U.S. citizens residing in the United States are eligible to participate, contingent upon meeting qualification standards and agreement to specified recapture provisions.

Participants (other than ‘custody account’ applicants) must prove stable credit history, stable job history, no recent drug/felony convictions.

These general recapture provisions include:

– Waiving all federal income tax refunds for a period of 5 years.

– Waiving benefits from economic security programs, select benefits from means-tested welfare programs, SSI, and SSDI for a period of 5 years.

– Enrollees in the Medicare, VA Healthcare system, Federal Employees Health Benefits (FEHB), and TRICARE will be subject to a $6,000 deductible for primary care and outpatient services annually for a period of 5 years. (See full plan for more details)

Primary scoring assumptions:

The Plan assumes an 80% participation rate by U.S. citizens. Wealthier Americans would choose not to participate, due to the comparative benefit of income tax refund amounts. Many individuals of lower socio-economic sector would also choose not to participate, due to the comparatively high benefits profiles that they would not wish to give up.

The Plan assumes that participating families would use significant funds to pay down / eliminate debt, and that these longer-term, lower debt service obligations would enhance the financial security of participating families for several decades beyond the opening activation period. Federal, state, and local government entities would benefit from longer-term tax revenue growth and reduced citizen dependence on government-based entitlement program benefits.

The Plan assumes that dynamic new efficiencies would emerge in the healthcare system – with more families managing/directing healthcare expenditures through their MSAs.

The Plan assumes that apart from the recapture provisions, there would also be significant tax revenue growth for federal, state and local government entities from free-market economic revitalization, more people working and paying taxes, and from the elimination of various income tax deductions (e.g. mortgage / HELOC interest expense).

The Plan assumes that there would not be a massive full-scale move back into the means-tested welfare programs, income security programs, SSI, and SSDI at the end of the initial 5-year activation period.

The benefits of a free-market economy and newfound economic liberty for American families would provide positive economic inertia throughout years 5-10, and for several decades beyond.

Recapture provisions would provide a substantial federal budget surpluses for each year of the initial 5-year period. Economic growth over the following 10-15 years would generate sufficient recapture funding and tax revenue growth to offset the entire initial Federal Reserve balance sheet expansion.

Significant inertia from The Plan would also provide on-going, market-based growth benefits over succeeding years that far exceed any prospect for healthy economic growth that may be expected under America’s current big-government, central-planning approach.

Dynamic economic benefits would flow from:

– Family level massive debt elimination, financial security gains.

– Timely, sweeping reversal of big government “central planning” control.

– Productivity gains from reversal of work disincentives currently embedded in social programs.

– Stabilization of bank capitalization, housing market.

– Strengthen / stabilize long-term value of U.S. Dollar.

– Minimizing the role of government in managing, directing, controlling the affairs of citizens.

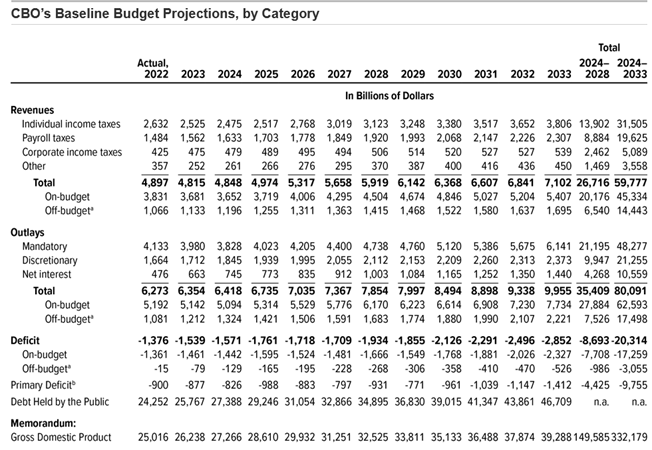

2. Federal Budget Deficit Projections – Congressional Budget Office

The Budget and Economic Outlook: 2023-2033 projects budget deficits ranging from $1,571 trillion in 2024, up to $1.855 trillion in 2029, and on up to $2.852 trillion by 2033. Actual deficits for the out years are likely to be higher than CBO projections, based upon history (“actual” versus “projected”).

The Leviticus 25 Plan – the most powerful economic acceleration plan in the world: economic scoring summary.

3. Federal Income Tax Recapture

The scoring model assumes that 80% of U.S. citizens will participate in The Leviticus 25 Plan.

Participants must give up their tax refunds through the Plan’s recapture provisions for the 5-year target period (2025-2029).

According to 2023 IRS Filing season statistics, through Dec 29, 2023:

105,734,000 total refunds were paid out for a total of $334.861 billion.

Refund totals have increased by ~$31.2 billion over the past six years, from $303.761 billion (2018) to a current (estimated) $334.861 billion (2023), representing an average increase of $5.2 billion per year.

A conservative estimated average of $5 billion per year (2025-2029) will be used for this recapture calculation.

2023: $334.9 billion

2024: $339.9 billion

2025: $344.9 billion

2026: $349.9 billion

2027: $354.9 billion

2028: $359.9 billion

2029: $364.9 billion

Total: $1.775 trillion

Total recapture X 80%: $1.775 trillion X .8 = $1.420 trillion

Total recapture per annum (2025-2029): $1.42 / 5 = $284.0 billion

Participants in the Plan will forego Economic Security Program benefits and select means-tested welfare benefits for the period 2025-2029.

Economic security programs: About 8 percent (or $522 billion) of the federal budget in 2023 supported programs that provide aid (other than health insurance or Social Security benefits) to individuals and families facing hardship. Economic security programs include: the refundable portions of the Earned Income Tax Credit and Child Tax Credit, which assist low- and moderate-income working families; programs that provide cash payments to eligible individuals or households, including unemployment insurance and Supplemental Security Income for low-income people who are elderly or disabled; various forms of in-kind assistance for low-income people, including the Supplemental Nutrition Assistance Program (formerly known as food stamps), school meals, low-income housing assistance, child care assistance, and help meeting home energy bills; and other programs such as those that aid abused or neglected children.1

The Leviticus 25 Plan – the most powerful economic acceleration plan in the world: economic scoring summary.

5. Medicaid/CHIP Recapture

Each U.S. citizen participating in The Plan will receive a $30,000 deposit, funded through a Federal Reserve-based Citizens Credit Facility, into a personal Medical Savings Account (MSA).

The Leviticus 25 Plan assumes 80% participation by Medicaid / CHIP enrollees.

Within this comprehensive economic plan, The U.S. Health Care Freedom Plan provides

Medical Savings Account (MSA) funding of $30,000 to cover the $6,000 deductible for Medicaid and CHIP eligible primary care events and select out-patient care services – primarily related to routine medical appointments, Medicaid prescription events, disease state monitoring clinics, and other desired primary care services.

September 2023 Medicaid & CHIP Enrollment – 88,414,773 individuals were enrolled in Medicaid and CHIP in the 50 states and the District of Columbia that reported enrollment data for September 2023. 81,408,432 individuals were enrolled in Medicaid. 7,006,341 individuals were enrolled in CHIP.

The 88,414,773 enrollment level represents a decrease of 2,518,996 (2.77%) from the Sep 2022 ‘Covid-period’ enrollment of 90,933,769. It represents an increase of 4,799,996 (5.74%) from the July 2021 ‘pre-Covid’ enrollment of 83,614,777 individuals.

Using a conservative estimate of 90.0 million for 2024, with a projected 2% annual growth rate:

2024: 90.0 million

2025: 91.8 million

2026: 93.6 million

2027: 95.5 million

2028: 97.4 million

2029: 99.3 million

Total: 477.6 million receiving benefits 2025-2029

Average annual enrollment (2025-2029): 95.52 million

95.52 million X .8 = 76.42 million X $6,000/year X 5 years = $2.293 trillion

Total Medicaid/CHIP recapture during the 5-year target period (2025-2029): $2.293 trillion

Note 1: The potential savings of $2.296 trillion do not take into account the additional savings to state government outlays, which range from 15% to 35% of total Medicaid-CHIP spending.

Note 2: The potential savings of $2.296 trillion does not take into account the likelihood of additional savings from individuals no longer being eligible for Medicaid-CHIP, due to their improving financial status.

______________________

6. Medicare Recapture

Each U.S. citizen participating in The Plan will receive a $30,000 deposit, funded through a Federal Reserve-based Citizens Credit Facility, into a personal Medical Savings Account (MSA).

The Leviticus 25 Plan assumes 80% participation by Medicare enrollees.

Within this comprehensive economic plan, The U.S. Health Care Freedom Plan provides

Medical Savings Account (MSA) funding of $30,000 to cover the $6,000 deductible for Medicare-eligible primary care events and select out-patient services – primarily related to routine medical appointments, Medicare Part D prescription events, disease state monitoring clinics, and other desired primary care services.

There were 65,954,976 people are enrolled in Medicare as of May 2023.

Projection: Medicare spending growth is projected to average 7.2% over 2021-2030, the fastest rate among the major payers. Projected spending growth of 11.3% in 2021 is expected to be mainly influenced by an assumed acceleration in utilization growth, while growth in 2022 of 7.5% is expected to reflect more moderate growth in use, as well as lower fee-for-service payment rate updates and the phasing in of sequestration cuts. Spending is projected to exceed $1 trillion for the first time in 2023. By 2030, Medicare spending growth is expected to slow to 4.3% as the Baby Boomers are no longer enrolling and as further increases in sequestration cuts occur.

Medicare – As of May 2023, 65,954,976 people are enrolled in Medicare. This is an increase of 118,238 since the last report.

*33,945,540 are enrolled in Original Medicare.

*32,009,436 are enrolled in Medicare Advantage or other health plans. This includes enrollment in Medicare Advantage plans with and without prescription drug coverage.

*51,742,496 are enrolled in Medicare Part D. This includes enrollment in stand-alone prescription drug plans as well as Medicare Advantage plans that offer prescription drug coverage.

The Leviticus 25 Plan assumes 80% participation by Veterans Administration healthcare enrollees. Within this comprehensive structure, The U.S. Health Care Freedom Plan provides Medical Savings Account (MSA) funding of $30,000, through a Federal Reserve-based Citizens Credit Facility, to cover annual $6,000 deductibles over the course of the 5-year target period (2025-2029).

FY 2022 – 9.07 million enrollees in the VA health care system.

The plan assumes a conservative 1% growth rate in VA Health Care enrollment (2025-2029).

The Leviticus 25 Plan assumes 80% participation by TRICARE enrollees.

Through The U.S. Health Care Freedom Plan, participating members will receive a Medical Savings Account (MSA) funding injection of $30,000, through a Federal Reserve-based Citizens Credit Facility, to cover annual $6,000 deductibles for desired primary care and out-patient services over the course of the 5-year target period (2025-2029).

There are currently ~9.5 million U.S. citizen beneficiaries in various locations around the world.

Recapture – total (2025-2029): 9.5 million X 0.8 X $6,000 X 5 years: $228.0 billion

The Leviticus 25 Plan assumes 80% participation by FEHB enrollees.

Participating members will receive a Medical Savings Account (MSA) funding injection of $30,000, through a Federal Reserve-based Citizens Credit Facility, to cover annual $6,000 deductibles for desired primary care and out-patient services over the course of the 5-year target period (2024-2028).

There are currently 9.0 million U.S. citizen FEHB beneficiaries. Note – the Federal government also pays approximately 72% of premium costs per enrollee.

Recapture – total (2025-2029): 9.0 million X 0.8 X $6,000 X 5 = $216.0 billion

The FEHB Program is the largest employer-sponsored group health insurance program in the world, covering over 9 million people including employees, annuitants …

________________________

9. Social Security Disability Income (SSDI)

The Leviticus 25 Plan specifies that participants will not be eligible for SSDI benefits.

The Plan assumes 80% participation.

Number, average, and total monthly benefits, December 2023: 8,414,000 recipients

Total annual SSDI payments, December 2023: ~$142.572 billion.

SSDI received an 8.7% Cost of Living Adjustment (COLA) for 2023.

This projection assumes a conservative 2% growth per year for 2025-2029.

2023: $142.572 billion

2024: $145.423 billion

2025: $148.331 billion

2026: $151.298 billion

2027: $154.324 billion

2028: $157.410 billion

2029:$160.558 billion

Total: $771.921 billion / Average per year: $154.384 billion

Total for 5-year target period 2025-2029:

Plan assumes 80% participation – recapture: $771.921 billion X 0.8 = $617.537 billion

Source(s): Social Security Benefits Dec 2023 – Disability Insurance https://www.ssa.gov/policy/docs/quickfacts/stat_snapshot/

Recipients: 8,414,000 | Total monthly benefits $11.881 billion;

The Leviticus 25 Plan – the most powerful economic acceleration plan in the world: economic scoring summary.

Interest expense recapture on projected deficits 2025-2029

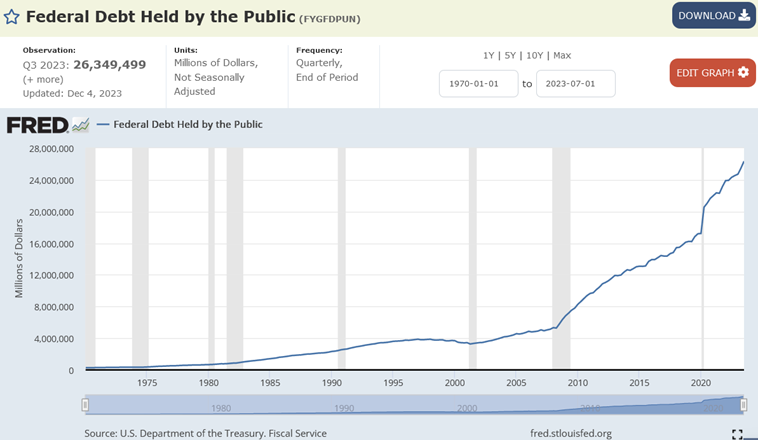

Federal debt has increased from $22.1 trillion in 2020 to $34.0 trillion as of December, 2023. Federal debt held by the public is reported to be $27.783 trillion, with the remainder, $6.216 trillion of intra-governmental debt outstanding, which arises when one part of the government borrows from another. This intra-governmental debt interest expense will be omitted from this calculation, since those dollars are not expensed directly.

U.S. monthly interest rate on interest-bearing debt 2018-2023

As of December 2023, the United States government has a monthly interest rate of 3.11 percent on its debt, continuing an upward trend in interest rates that began at the beginning of 2022. In March of 2023, U.S. debt reached 31.46 trillion U.S. dollars.

Interest expense on the public debt during FY 2024 is currently being expensed at a monthly interest rate of 3.11%. Projections estimate monthly rate will decline to an approximate average of 2.3% – 2.4% over the next 5-6 years.

This projection will assume an average monthly interest rate of 3.10% for 2024, and an average monthly interest rate of 2.75% in calculating the interest expense to be eliminated during the budget surplus years of 2025-2029.

This projection also assumes that annual federal budget deficits will be funded through Treasury Issuance at an average of 79.0% rate fir Debt Held by the Public.

Year Annual Deficit/2 X %Debt Held by Public X Interest Rate

2024: $1.571 trillion/2 X .79 X .0310 = $19.237 billion

2025: $1.761 trillion/2 X .79 X .0280 = $19.477 billion

2026: $1.718 trillion/2 X .79 X .0270 = $18.322 billion

2027: $1.709 trillion/2 X .79 X .0260 = $17.551 billion

2028: $1.934 trillion/2 X .79 X .0250 = $19.098 billion

2029: $1.855 trillion/2 X .79 X .0240 = $17.585 billion

Recapture: Total interest expense eliminated by projected operating surpluses: $92.033 billion

Average annual budget surplus (projected) 2025-2029: $563.033 billion / 5 years; $112.6 billion per year

___________________________________

Note 1: Projected budget surpluses for 2025-2029 do not factor in the additional government tax revenue gains that would accrue from the massive shift in capital away from debt service and into productive economic activity.

Note 2: Projected budget surpluses for 2025-2029 do not factor in the additional government tax revenue gains that would accrue from significantly lower levels of debt deduction on individual income tax filings.

Note 3: Projected budget surpluses from the Medicaid / CHIP recapture do not take into account the likelihood of fewer citizens actually qualifying for Medicaid / CHIP benefits.

Note 4: The Plan’s funding of individual Medical Savings Accounts (MSAs) with the $6,000 deductible provision per year would result in an enormous drop in the number of claims each year for Medicare reimbursement. Medicare payroll taxes would generate a growing revenue stream, due to stronger economic growth, while outlays would drop significantly from the reduced claims numbers – thereby providing the Fed with a powerful tool to recapitalize the Medicare Trust Fund, via the Citizen’s Credit Facility.

The Leviticus 25 Plan – Projection limitations

There can be no question that The Leviticus 25 Plan would generate healthy, broad-based economic growth from broad-based debt reduction and improved financial stability at the family level, the restoration of free market dynamics in commerce, and scaling back social program work disincentives.

The Leviticus 25 Plan does not attempt to project how much additional tax revenue and reduced cost of government will be realized, above and beyond the Recapture Provisions, over the course of the initial five years of the plan. In that sense, The Plan understates the effect of additional dynamic economic benefits.

Robust funding of Medical Savings Accounts and the elimination of millions of insurance claims and claims resolutions for basic primary care and everyday healthcare purchases swill save millions of man-hours of health care cost on an annual basis. Scaling back government involvement in basic primary care and everyday healthcare purchases for millions of Americans will also generate massive cost savings.

The Plan makes no attempt to project the positive effects of the streamlined, consumer-driven efficiencies that will emerge, and the cost reduction and improvement in services.

The Plan therefore understates the benefits.

The Plan projects an 80 percent participation rate by U.S. citizens. It is assumed that a large number of wealthy Americans will not participate, because their tax refunds are larger than the annual Plan benefits. And it is assumed that a large number of Americans receiving significant government benefits for extraordinary health or economic issues will also not participate.

Cost savings from the reductions in massive social welfare spending and other programs, like unemployment insurance, workman’s compensation, SSI and SSDI can be difficult to quantity, since state and federal funding mechanisms may both be involved in various ways. In that regard, The Plan may understate, or it may overstate, the benefits.

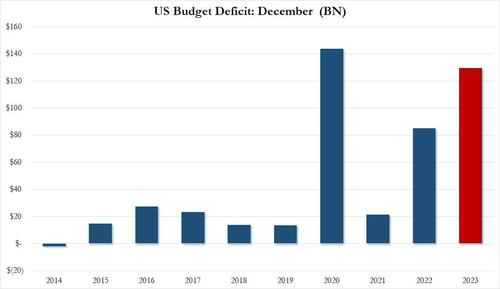

As for the final, and most shocking, data point, the December budget deficit of $129.4 billion was more than $40BN higher than the $87.5BN median estimate, and was more than 50% higher compared to the $85BN December deficit in fiscal 2022.

By Diccon Hyatt | Investopedia | Published January 08, 2024

Key Takeaways

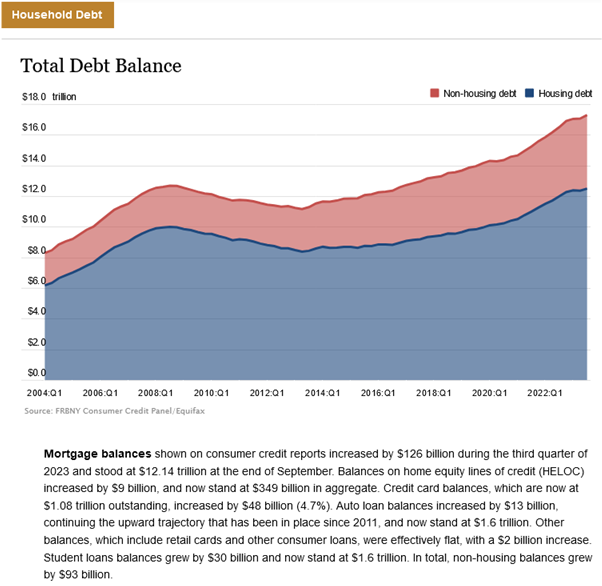

Consumer debt surged $23.8 billion in November, most of that due to a $19.1 billion increase in revolving debt, mainly credit cards.

The debt is increasingly burdensome for households, with interest rates on credit card debt averaging more than 21%, the highest in decades.

Some households are under increasing financial pressure and falling behind on their bills, with delinquencies for credit cards and car loans having recently surpassed pre-pandemic levels

____________________________

Washington Democrats’ Plan: Expand federal and state government-based social programs, expand federal bureaucracy. No plans of record to constrain spending, bring budget deficits back under control.

Washington Republicans’ Plan: No credible, politically feasible economic strategy to constrain spending enough to have any material effect on budget deficits. No plan to protect the purchasing power of the U.S. Dollar and maintain its status as the world’s reserve currency. No plan to address America’s long-term public and private debt leverage issues.

Washington Republicans have the opportunity of a lifetime to present a master plan to dig America out of its cavernous debt hole and restore the American dream – and they have nothing.

Main Street America Republicans do have a plan – an economic acceleration masterpiece that will: 1) Generate massive new tax revenue flows, cost savings, and multi-billion dollar budget surpluses each of the first five years of activation; 2) Set the U.S. Dollar back on track for long-term strength and stability; 3) Eliminate trillions of dollars in Household Debt and restore financial security for millions of American families; 4) Revitalize economic growth, strengthen the U.S. banking system; and 4) Restore economic liberty and free market economics in the United States.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

America needs a new plan – one that offers a helping hand ‘up out of poverty,’ rather than the perpetuating the current system that “severely punish work effort,” promote continual dependence on government, and stifle the human spirit.

Phil Gramm and John Early’s “Another Wrong Way to Measure Poverty” (op-ed, Dec. 6) is notable for revealing how poverty rates are artificially inflated by the Census Bureau by excluding most social-welfare benefits. When all the benefits are counted, the authors contend, “the percentage of Americans living in poverty falls to only 2.5%.”

…. While Americans may be more comfortable than census numbers suggest, the authors miss the poverty of opportunity that occurs once people become ensnared in the social-welfare system.

Consider a 2022 study by economist Ed Dolan. He gives the case of a hypothetical Boston family with one adult, two young children and an income of $22,000, which is at that group’s official poverty level. The family qualifies for around $66,000 in social-welfare benefits, which certainly brings it out of poverty.

But here’s the rub: Even if the family’s income doubles to $44,000, the social-welfare benefits collectively roll back $1.03 for every marginal dollar earned over this range, leaving the family worse off in total wages and benefits. Our research calls this phenomenon a “disincentive desert,” (as opposed to the much-studied “benefits cliff”), since this is equivalent to an extremely high and persistent tax on work effort, ranging from 90% to 110%, across long spans of income.

As a result, many low-income Americans are left comfortably numb in a social-welfare state that severely punishes work effort and stifles the imagination for what life might be. I contend that rather than focusing on living standards at a point in time, we should see that life without hope of economic progress is the ultimate definition of poverty. Policies that address this issue are the key to reviving downward trends in labor-force participation. –Prof. Craig J. Richardson, Winston-Salem State University

____________________________

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

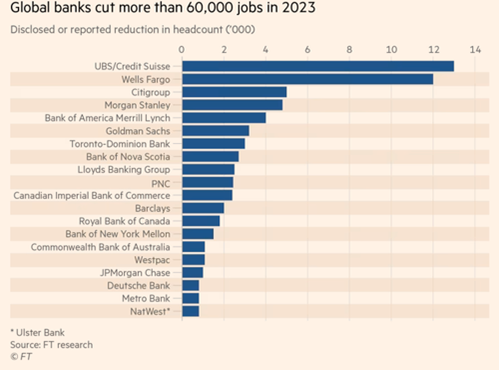

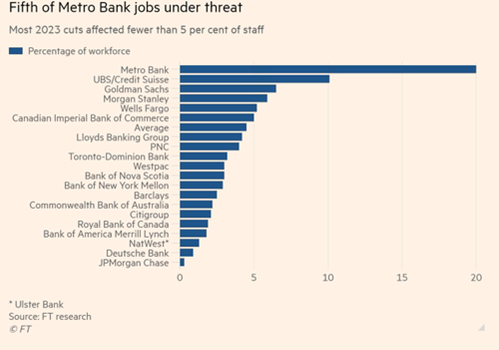

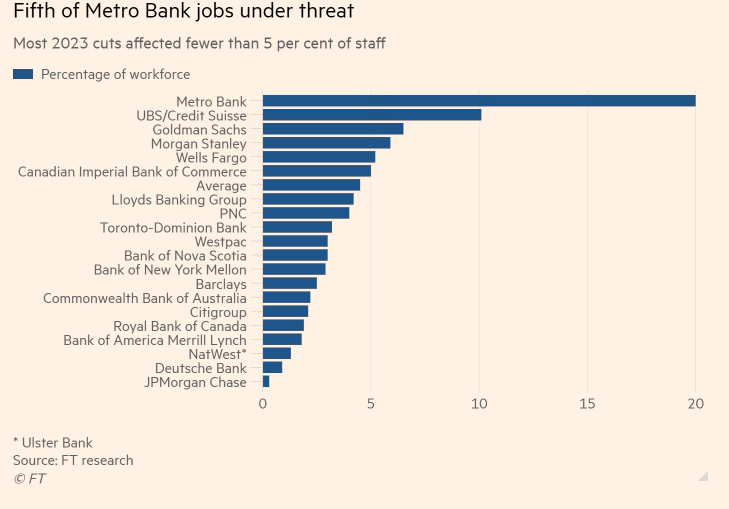

The collapse of three US regional banks – First Republic Bank, Silicon Valley Bank, and Signature Bank – marked some of the largest failures in the banking system since 2008. Central banks contained the “mini-crisis” earlier this year with forced interventions and the mega-merger of Credit Suisse and UBS. Despite the interventions, global banks still axed the most jobs since the global financial crisis.

A new report from the Financial Times shows twenty of the world’s largest banks slashed 61,905 jobs in 2023, a move to protect profit margins in a period of high interest rates amid a slump in dealmaking and equity and debt sales. This compared with the 140,000 lost during the GFC of 2007-08.

“There is no stability, no investment, no growth in most banks — and there are likely to be more job cuts,” said Lee Thacker, owner of financial services headhunting firm Silvermine Partners.

FT noted that corporate disclosure data and its independent reporting did not include smaller regional bank cuts, indicating total job loss could be much higher.

At least half of the job cuts came from Wall Street lenders struggling with Western central banks’ most aggressive interest rate hikes in a generation.

The most significant cut of any single bank was at Switzerland’s UBS.

Morgan Stanley reduced jobs by 4,800, Bank of America by 4,000, Goldman Sachs by 3,200, and JPMorgan Chase by 1,000. As a whole, Wall Street cut 30,000 workers this year.

“The revenues aren’t there, so this is partly a response to overexpansion. But there is also a simpler explanation: political cost-cutting,” said Thacker.

Gaurav Arora, global head of competitor analytics at Coalition, warned: “We expect full-year 2024 to be a continuation of the story of 2023.”

Wilmington Trust, Mar 16, 2023 – The macro picture for distress

Many loan market analysts have taken a dim view of the distressed space in the next two years. Fitch, for example, sees a band of 2023 institutional leveraged loan default rates between 2.5%–3.0%. They project $47 billion of defaults in 2023 at the midpoint of their forecast.1

Deutsche Bank is more pessimistic, expecting a 5.6% default rate in the United States and a 3.7% rate in the euro market in 2023. Per their estimates, default rates on U.S. leveraged loans will hit a near-record high of 11.3% in 2024, while defaults on euro-leveraged loans will hit 7.1%.2

Undoubtedly, the economic climate is harsh for borrowers. A complex economic cycle continues to spin. Wilmington Trust’s 2023 Capital Markets Forecast highlights an inflationary vortex driven by labor, China, and energy, which creates structural stress.3 This vortex and the resulting monetary policy are exerting its pull across companies’ capital structures.

Mortgage delinquencies – “About five million U.S. households were estimated to be behind on their last month’s mortgage repayment in June 2023. Homeowners between 40 and 54 years made up over 1.8 million households late on their payment. Second in rank were roughly 1.5 million homeowners between 25 and 39 years” -Statista, Jul 23, 2023

According to Kipplinger, “the delinquency rate for conventional loans increased 21 basis points to 2.5%, while the rate for FHA loans increased 55 basis points to 9.5%. The delinquency rate for VA loans increased 6 basis points to 3.76%.”

__________________________________

The Leviticus 25 Plan provides direct liquidity extensions to qualifying U.S. citizens, through a Fed-based Citizens Credit Facility, for the express purpose of massive ‘ground-level’ debt elimination.

This process will provide the banking system with massive new inflows of liquidity to strengthen cash reserves, solve a majority of banks’ distressed debt and delinquent mortgage issues, allow banks to rectify a significant proportion of their ‘maturity mismatch’ issues with fresh purchase of Treasuries and other high-grade credit instruments yielding significantly higher yields.

The Leviticus 25 Plan will generate federal budget surpluses of $619.5 billion each of the first five years following activation, and pay for itself over a 10-15 year period.

It will generate long-term economic growth – not dependent upon debt issuance.

It will restore financial security for millions of American families – and reduce dependence on government programs.

The Leviticus 25 Plan is a dynamic economic initiative providing direct liquidity benefits for American families, while at the same time scaling back the role of government in managing and controlling the affairs of citizens. It is a comprehensive plan with long-term economic and social benefits for citizens and government.

The inspiration for this plan is based upon Biblical principles set forth in the Book of Leviticus, principles tendering direct economic liberties to the people.

The Leviticus 25 Plan – An Economic Acceleration Plan for America

{kind=link}

{kind=link}